Investment Summary

Universal Medical (UM) announced that pre-tax earnings increased by more than 20% in the third quarter. We expect both revenue and net profit in 18E to increase by around 25%. With continuous progresses of hospital investment management business and steady growing financial leasing business, UM is expected to build a comprehensive healthcare group. We use SOTP method, given the financing lease business 7x PE, hospital investment management business 15x PE, to derive target price of HK$8.62, BUY rating. (Closing price at 2 Nov 2018)

Business Overview

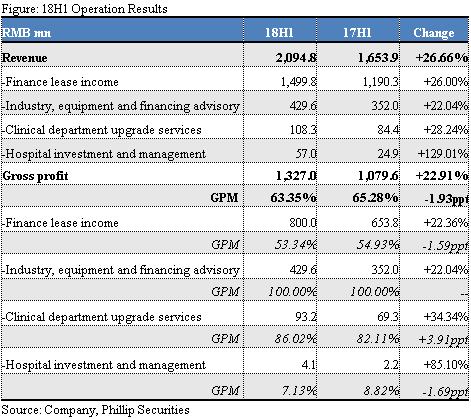

Strong growth in first three quarters, and expected ~25% topline growth in 18E. Its latest announcement shows that pre-tax profit growth was above 20% during previous three quarters. In 18H1, UM realized revenue of RMB2.09bn, up by 26.7% yoy, gross profit increased 22.9% to RMB13.27mn, and net profit increased 26.7% to RM73mn.. ROE increased nearly 2 ppts to 19.17%. Topline and net profit are expected to maintain over 25% growth in 18E. New hospital business is expected to report around RMB100mn income in 18E.

Financial leasing business: interest earning assets yield slightly lowers and debt cost remains stable. In 18H1, the revenue of financial leasing business was RMB1499.78mn, up by 26% yoy, and gross profit increased by 22.4% to RMB800mn. More stringent risk control measures are implemented to track customer repayment ability and monitor credit changes. We know from our checks that market demand for medical financial leasing remains strong, but UM chooses to do business with customers with higher credit, who have stronger bargaining power at the same time. So we predict the yield to keep relatively low in 18H2. We emphasize that these stricter risk-control measures, though putting pressure on short-term profitability, facilitate high quality of interest-bearing assets and the recovery of accounts receivable, which ensure long-run development. Also UM actively adapts to interest rate changes. Its debt costs will remain relatively stable throughout 2018.

National policies accelerate hospital investment business. The Chinese government called for (in Guo Zi Fa Gai Ge [2017] No.134) that the transfer and reform of SOE medical institutions should be completed before the end of 2018. In 18H2, we see relevant official departments accelerating the process of divestiture of SOEs` hospitals from original SOEs. More SOEs` hospitals are expected to reach cooperation agreements with buyers or partners by the end of the year. UM's shareholder General Technology Group is a central SOE with healthcare industry as its core business. Leveraging on support from main shareholder, UM is proactively pitching SOE's hospitals for potential cooperation. More hospital projects are expected by the end of 2018 and 2019.

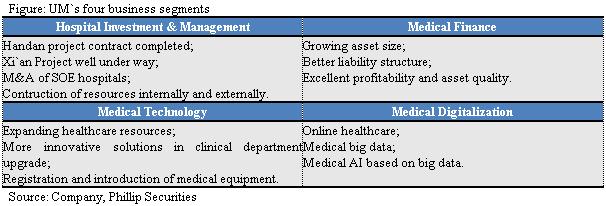

To building a first-class healthcare group. UM is trying to build a first class healthcare group with four core segments providing medical financial services, medical technology services, hospital investment management services and hospital digitalization services. Conforming to the rising domestic residents` medical demand, UM seizes the strip-off opportunity of SOEs` hospitals to attain hospital assets, and further expands hospital business scope by the on-going reconstruction and expansion of hospitals. Besides, UM's financial and technological advantages will help hospitals to upgrade scale, enhance technical strength, improve efficiency and profitability.

Strong growth in first three quarters, and expected ~25% topline growth for whole year. Its latest announcement shows that pre-tax profit growth was above 20% during previous three quarters. In 18H1, UM realized revenue of RMB2.09bn, up by 26.7% yoy, gross profit increased 22.9% to RMB13.27mn, and net profit increased 26.7% to RM73mn.. ROE increased nearly 2 ppts to 19.17%. Topline and net profit are expected to maintain over 25% growth in 18E. New hospital business is expected to report around RMB100mn income in 18E.

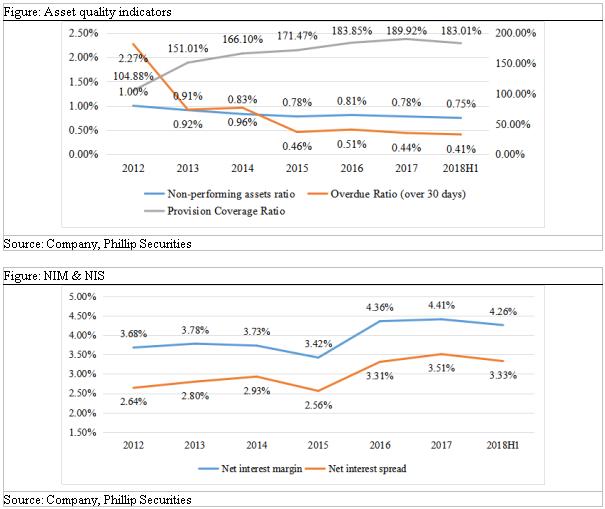

Financial leasing business: interest earning assets yield slightly lowers and debt cost remains stable. Total asset steadily grew by 13.8% yoy to RMB42,948.7mn. Finance lease segment report revenue of RMB1,499.78mn up by 26% in 18H1, and gross profit increased by 22.4% to RMB800mn. Finance lease receivables recorded RMB407.3mn, 75% of which was from medical industry. Non-performing assets ratio dropped from 0.78% to 0.75% and overdue ratio (over 30 days) declined from 0.44% to 0.41%. More stringent risk control measures are implemented to track customer repayment ability and monitor credit changes. We know from our check that market demand for medical financial leasing remains strong, but UM chooses to do business with customers with better credit, who have stronger bargaining power at the same time. Thus we see net interest spread narrowing to 7.96% (vs. 8.28% in 17H1, -0.32ppts). So we predict the yield to keep relatively low in 18H2. We emphasize that these stricter risk-control measures, though putting pressure on short-term profitability, facilitate high quality of interest-bearing assets and the recovery of accounts receivable, which ensure long-run development. Also UM actively adapts to changing interest conditions through adjusting financing strategy and optimizing debt structure. We expect its debt costs to remain relatively stable throughout 2018.

Contribution from hospital investment management business will increase significantly from 2019E. In FY17 and 18H1, the income of hospital investment management business was RMB77.47mn/56.98mn respectively. Gross profit was RMB9.7mn and RMB4.06mn, with GPM of 7.77%/7.13%. We estimate that the revenue of hospital investment management business will be about RMB100mn in FY18E, mainly from the supply chain business of the First Affiliated Hospital of Xi`an Jiaotong University. We expect that from 2019, the supply chain business of the Xi`an FAH and the Handan First Hospital will be further reflected in the operating income of UM.

In 18H2, the government accelerated the divestiture of SOEs` hospitals. In Aug 2017, the Chinese government delivered a document (Guo Zi Fa Gai Ge [2017] No.134), calling for the reform to be completed by the end of 2018 and supporting SOEs focusing on medical indstry to take over and integrate these SOE hospitals. In 18H2, relevant official departments make efforts to accelerate the process of divestiture of SOEs` hospitals from original SOEs. More SOEs` hospitals are expected to reach cooperation agreements with buyers or partners by the end of the year. UM's shareholder General Technology Group is a central SOE with healthcare industry as its core business. Leverage on support from main shareholder, UM is proactively pitching SOE's hospitals for potential cooperation. More hospital projects are expected by the end of 2018 and 2019.

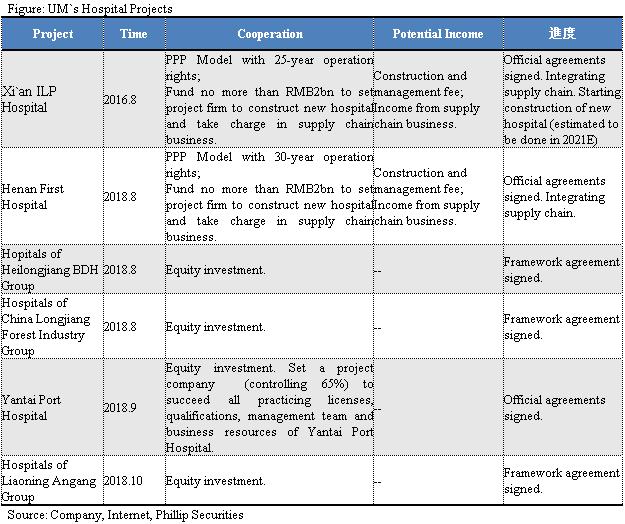

Launching new projects in Handan, Heilongjiang and Yantai in 2018. UM has signed formal cooperation agreements for Xi`an, Handan and Yantai projects, and framework agreements with Heilongjiang BDH Group, China Longjiang Forest Industry Group and Liaoning Angang Group. We notice that new cooperation projects are almost equity investments. Equity investment will make UM have stronger control over medical institutions and greater voice over hospital management, so as to more effectively promote hospital restructuring and reform, improve efficiency of hospital management and operation, and upgrade technology strength.

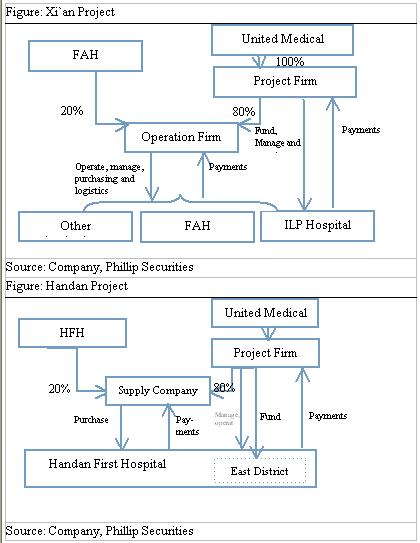

Xi`an International Land and Port Hospital: Xi`an FAH is a large-scale comprehensive third-class A-level hospital managed by NHC. In Aug 2016, UM signed an agreement with First Affiliated Hospital of Xi`an Jiaotong University. UM will construct the new International Land Port Hospital for FAH and provide supply chain services for FAH and ILP Hospital through the project company (holding 80%). ILP hospital is positioned as a non-profit comprehensive three grade hospital. It will offer 1000 beds at the first stage. The future benefits will come from construction and management fee (based on a certain proportion of hospital profits) and earnings of supply chain companies. UM will invest no more than RMB2bn for the project. Currently, UM has sorted out procurement options for FAH, as well as the pharmaceutical delivery and upstream production enterprises, and signed a Sunshine Procurement Service Agreement (《陽光採購服務協議》) with FAH in early Aug 2018. We expect the integration of supply chain business will be completed by 2021E. Meanwhile, the master plan and building layout plan for International Land Port Hospital have already been finalized, while relocation and construction of the high-voltage lines and other related work are underway. In future, UM will continue to progress the construction and engineering of ILP Hospital, and speed up supply chain operation.

New East District of Handan First Hospital: An announcement in Aug shows that UM has signed a cooperation agreement with Handan Health Commission and Handan First Hospital. HFH is a leading comprehensive third-class A-level hospital in Handan City. UM will build and operate a new Eas District with HFH. The planned new district, with 2000 beds planed, will become a branch of HFH. UM will provide a total of no more than RMB2bn in cash for the construction and participate in the management and operation of HFH (including HFH and NED). It will also invest no more than RMB28mn (80% of shares) to establish a medical supply company with HFH to provide medical services. Future income will come from construction and management fee charging on HFH and NED and earnings from supply chain firm.

Yantai Port Hospital: In Sep, UM announced an agreement on the restructuring and cooperation of Yantai Port Hospital with Yantai Port Group, which stipulates that a UM subsidiary shall invest in cash (65% of shares) and YPG shall invest in net assets (35% of shares)to form a joint venture company. JV will inherit all practicing licenses, qualifications, management team and business resources of YPH. YPH is a non-profit second class A Hospital Affiliated to YPG with 500 beds. In the future, the capital invested by UM will be used for further bed expansion and equipment allocation. UM will also systematically improve the technical level and service capacity of the hospital through disciplines upgrading, technology introduction, personnel training, management and mechanism optimization. We estimate that if the transformation of the non-profitable YPH into a profitable hospital would succeed, UM's potential benefits will come from hospital earnings and supply chain business, etc. If not, UM may also collect management fees or supply business earnings.

UM has signed framework agreements with Heilongjiang Beidahuang Group, Heilongjiang Forest Industry Group and Liaoning Angang Group, while formal agreements are yet to be signed.

Hopitals of Heilongjiang BDH Group: In Aug 2018, UM and BDH signed a cooperation framework agreement, which will integrate the existing foundation and development needs of individual hospitals under BDH Group, through capital investment, technology introduction, hardware updating, etc, to improve the technical standard and service ability of BDH hospitals. BDH Group has 9 administrative bureaus, 113 farms and pastures and 983 SOE enterprises. It has a large number of medical institutions, with a total of more than 10,000 beds, covering all levels from tertiary hospitals to primary hospitals. It is the main medical resource cluster serving the workers of BDH Group and effectively covering the people around the reclamation area.

Hospital under Heilongjiang Forest Industry Group: HFIG is the largest state-owned forest region and forest industry group in China. It produces more than 120 medicinal plants. Now it has 8 medical institutions. UM will cooperate with HFIG to promote the development of healthcare business and achieve a win-win situation, while a joint-stock medical healthcare platform company is about to be set firstly.

Liaoning Anshan Angang Group Hospital: In Oct 2018, UM and Angang Group entered into a framework agreement on restructuring of AG's health industry. In the future, AG will be built into a domestic hospital group with technological innovation, sustainable development and differentiated management capabilities.

To building a first-class healthcare group. UM is trying to build a first class healthcare group with four core segments providing medical financial services, medical technology services, hospital investment management services and hospital digitalization services. Conforming to the rising domestic residents` medical demand, UM seizes the strip-off opportunity of SOEs` hospitals to attain hospital assets, and further expands hospital business scope by the on-going reconstruction and expansion of hospitals. Besides, UM's financial and technological advantages will help hospitals to upgrade scale, enhance technical strength, improve efficiency and profitability.

Valuation and Risks

We highlight that the strong market demand, good asset quality, and appropriate risk control of financial leasing business, which is expected to maintain steady growth. In addition, we are optimistic about hospital investment management business. UM is expected to obtain more SOEs` hospital projects relying on the SOE shareholder's background and outstanding medical resources, also leveraging on potential purchase of private hospitals in future, to build a first-class medical management group. At the same time, hospital resources will feed back the company's original businesses like financial lease, medical digitalization, industry consultation and others, forming a virtuous circle.

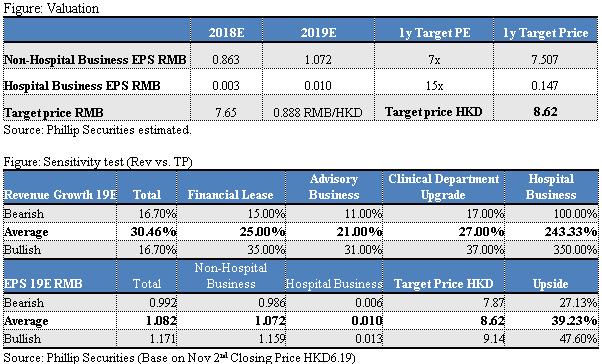

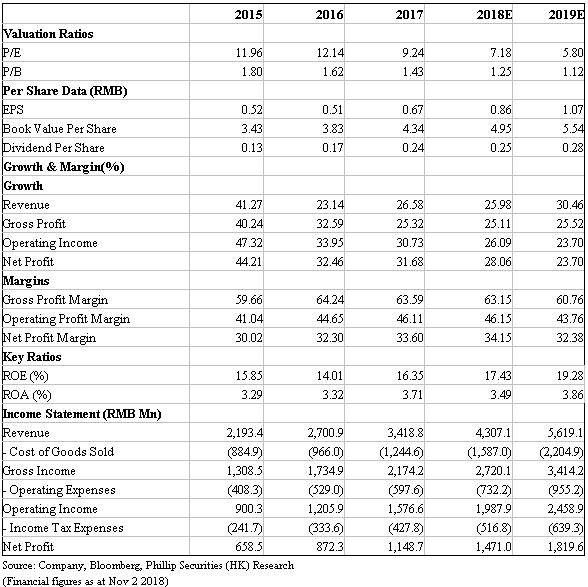

Our target price is HK $8.62 based on SOTP method. We estimate the growth rate and profit of these two parts and derive EPS estimation of medical finance leasing in 18E/19E to be RMB0.863/1.072, and EPS of hospital investment management business to be RMB0.003/0.01. Considering good quality of finance lease assets, declining non-performing asset ratio and 30-day overdue rate, we give target P/E ratio 7x to finance lease segment, and refer to the average expected P/E ratio 15x of hospital peers, and get target price of UM should be HKD8.62, BUY rating.

�Financials

Click Here for PDF format...