Investment Summary

Benefiting from the devaluation of the RMB and an one-time investment income from transferring asset, Fuyao Glass recorded brilliant result in 2018Q3. Excluding these effects, the Company's pretax profit in the third quarter increased by about 3%. Gross margin bottom out from 42% by 2018H to 44%. Unlike the slow-down domestic business, Fuyao's overseas business recorded more than 20% growth ratio. With the further improvement of productivity utilization and smoother man-machine running-in, it is expected that the U.S. factory will become a new profit growth point. We upgrade to the "Buy" rating,with target price to be HK$ 31.15. (Closing price as at 6 November 2018)

50% growth of results in the first three quarters and 84% jump in the third quarter

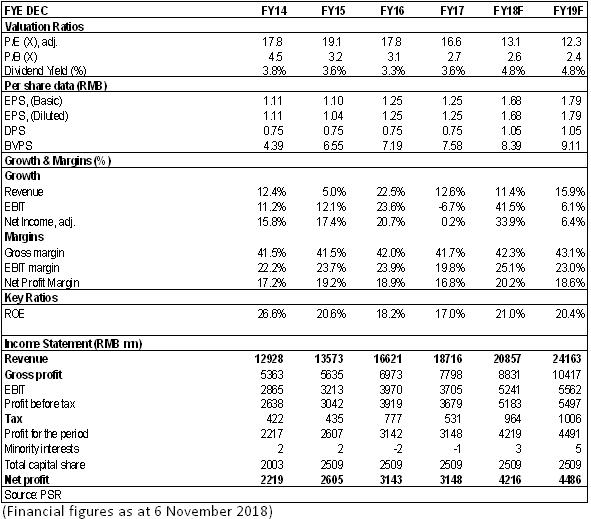

In the first three quarters of 2018, Fuyao Glass recorded a revenue of RMB15.12 billion, a year-on-year growth of 12.9%; a net profit for the year attributable to the shareholders of the Company of RMB3.26 billion, a year-on-year growth of 52%; a profit for the year attributable to the shareholders of the Company, net of non-recurring profit or loss of RMB2.8 billion, a year-on-year growth of 35%; and the earnings per share of RMB1.3. Among others, in the third quarter, the Company reported a revenue of RMB5.04 billion, a year-on-year growth of 7.5%; a net profit for the year attributable to the shareholders of the Company of RMB1.39 billion, a year-on-year growth of 84%.

Exchange earnings and one-time revenue boost of assets disposal

The Company's brilliant result mainly comes from: 1) Benefiting from the devaluation of the RMB, the Company recorded an exchange earnings of RMB242 million in the third quarter (this compares with a loss of RMB133 million in the same period last year); 2) during the reporting period, the Company transferred 51% of Beijing Futong's equity, and recorded an investment income of RMB0.45 billion. Excluding these effects, the Company's pretax profit in the third quarter increased by about 3%.

Gross margin steadily increased, and operational efficiency continued to improve

Fuyao's gross margin was 42.68% in the first three quarters, a year-on-year decrease of 0.13 percentage point. The Company's gross margin in the third quarter was 44.14%, a year-on-year growth of 1.64 ppts, and a quarter-on-quarter growth of 2.14 percentage points. Among them, the devaluation of the RMB contributed about 1/2, 1/4 came from the improvement of the operational efficiency of those projects in the U.S.A, and 1/4 from the Company's internal industry chain integration and fine management that promote the efficiency and reduce the cost. In addition, in the third quarter, the days of turnover for the accounts receivable of the Company decreased by five days, and those for the inventory by seven.

Domestic business is affected by the market, but still better than average

In the first three quarters, the income of Fuyao's domestic business only increased by 3.7% year-on-year, while in the third quarter, the income from its domestic business declined by 3.15%. Apart from the influence brought by the selling of the Beijing factory, it was mainly affected by the slowdown of the domestic automobile market as a whole. The income of the overall industry declined by about 5.7% in the third quarter, and the Company's performance was better than the average, as its market share and unit price have risen against the trend. We believe that the main reason is that the Company has conducted more export business than its counterparts, and the marketing activities have been strengthened/the product structure has been optimized.

The internationalization is becoming increasingly apparent, and overseas revenue is advancing rapidly

In the first three quarters, the Company's overseas revenue, as one of the contributing forces to beat the market, increased by 22.9% year on year, faster than the growth rate of the income from domestic business which is 3.7%. The U.S. factory achieved a profit of USD32.1 million in the first three quarters, but it recorded a loss in the same period last year. The capacity of the U.S. factory is 5.5 million sets, with 15% of development capacity being deducted. Actually, its capacity for normalized production is 4.6 million sets. This year, the sales volume will reach 3.1 million sets. Next year, the target is 3.9 million sets, a growth of 25%. There is still a big gap between the profitability of the U.S. factory and that of domestic factories. With the further improvement of productivity utilization and smoother man-machine running-in, it is expected that the U.S. factory will become a new profit growth point.

On the other hand, excluding the factor of the exchange rate, the Company's Russian factory recorded a loss of more than RMB30 million in the last year. It is estimated that the loss will be narrowed to about RMB10 million, because the factory began to make profits in October. Russia's auto industry is hitting the bottom from the recession caused by U.S. sanctions As the Company's bridgehead for further expansion into Europe, we predict that the Russian factory will operate better next year compared with this year.

Investment Thesis

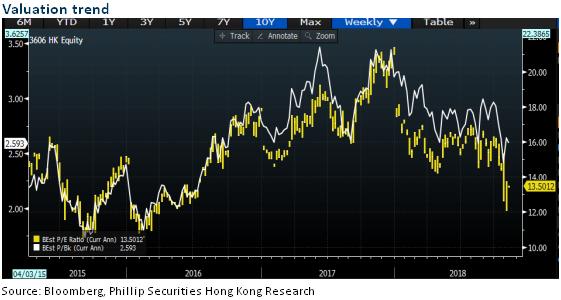

Overall, the improvement of overseas business marks the effect of the global strategy of the Company for several years. At the same time, the steady leading position, continuous optimization of the product structure and a high dividend rate provide a greater margin of safety for the Company. We upgrade to the "Buy" rating,with target price to be HK$ 31.15, equivalent to 16.3/15.3x P/E for 2018/2019E.

Risks

Demand for automobiles keeps sluggish; cost of raw materials increases; RMB appreciates

Catalyst

Success market development of overseas automobile market; rebound of domestic demand for automobile; depreciation of RMB

Financials

Click Here for PDF format...