Investment Summary

Minth's 2018H result slightly lower than forecast, but the increasing trend of the topline and core profit is still to continued. In the near future, Minth's production structure are expected to continue improving, triggered by increased investment on technology upgrades and product optimization We maintain the opinion that Minth's existing businesses indicate a robust growth momentum, while great potential boom lies before the new ones, on the base of more input on R&D etc. We gave target price of HK$ 33.1 and Buy rating. (Closing price as at 13 November 2018)

One-time factor resulted in lower-than-expected results, core net profit up by 10%

During the 2018 H1, Minth Group reported total revenue of RMB5.99 billion, up 14% yoy, and net profit of RMB980 million, down 6% yoy. The lower-than-expected results were due to 23 million administrative expenses resulting from the sale of stock options this year, compared with the previous year when net profit was boosted by investment income totaling RMB152 million from employee welfare properties and the sale of Minth subsidiaries. If this effect is taken out, the net profit from core business grew by about 10%.

Domestic market outperformed the overseas market on growth prospects

Specifically, the domestic business grew rapidly, reporting a revenue of approximately RMB2.68 billion and achieving a growth of approximately 17.5%, owing to the sales growth of Japanese and Chinese brands in the domestic Chinese market. The overseas market recorded a turnover of approximately RMB2.31 billion and a yoy growth of around 8.4%, benefiting from the growing businesses with European clients including Daimler and Volkswagen. Compared with the same period of last year, the growth rate of overseas business was dragged down by the lower-than-expected capacity utilization rate of North American factories. In an attempt to improve production efficiency, the Company moved the well-developed domestic equipment to overseas factories, and commissioned as well seasoned domestic factory management personnel to assist in the management of the Mexican factory. The management expects that the negative impact of overseas factories on the Company's gross margin will be confined since 2018.

Gross margin remained stable

During the reporting period, the overall gross margin remained approximately at 33.4%, down around 0.4 percentage point from the 33.8% for last year, mainly due to price cuts of old products, rising prices of raw materials, and unfavorable exchange rates. Hence, the Company implemented lean production and optimized the production layout to improve production and management efficiency, vigorously adjusted the product mix, and improved gross margin of Mexican factories, so as to maintain the overall gross margin at a stable level. Having maintained the gross margin guidance of 33-35% for the fiscal year, the Company takes confidence in the 2019 gross margin, which will be supported by the efficiency improvement and digital transformation of overseas factories.

The new pipeline rolled out successfully bringing sufficient backlogs

The Company has attached great importance to R&D investments and technological innovation with the R&D expenditure increased by 0.3 percentage point to 4.3%; in the light of strategies on light emission, intelligence and electrification, the Company achieved excellent results in the business development of new products.

In the development of light emission products, the Company has successively obtained purchase orders for its aluminum battery box/aluminum door frame products/electric rear compartment cover; in the development of intelligent products, the Company acquired orders in such new businesses as car camera/ACC labels, which has empowered its further expansion into intelligence products. Product development has accumulated more momentum. By the end of 2017, the Company has received purchase orders totaling a value of RMB92.2 billion, with a total order amount of RMB3 billion in 2018H1. Up to now, the annualized value of new orders reached 5.5 billion, making it very likely for the Company to accomplish its annual sales target.

Short-term challenges exist but long-term competitiveness is reinforced

The China-U.S. trade frictions have led the market to worry that the Company's export business would be slowing down. At present, the exportation to the United States accounts for about 7% of the total revenue and is mostly generated through FOB model, which means that the increased tariff in the short run is transferred to clients. In response to potential risks associated with growing tariffs, the Company is also considering expansion plans for North American and Thai plants. We believe that the Company will retain its competitive strength in the long run and grow exponentially in its future new businesses owing to its beforehand strategic layout.

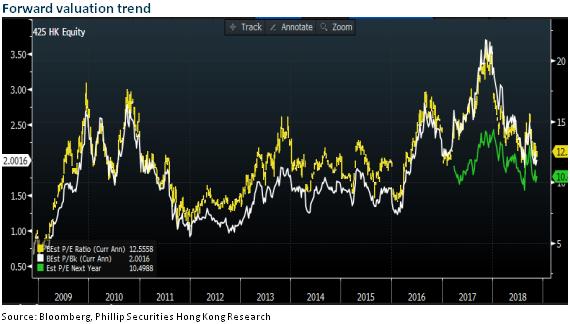

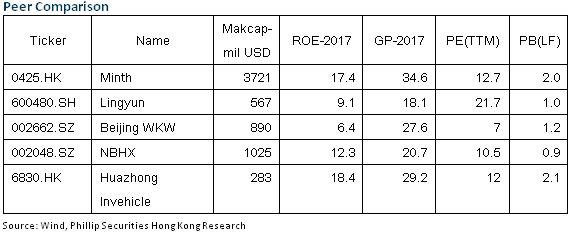

Valuation

The Company has a solid financial condition, with near 4.5 billion cash in hand. Besides, its operating net cash flow has increased to 1.05 billion. It is believed that the high dividend payout ratio will maintain. We believe that it is reasonable to give the company a valuation of 16.5x/12x P/E in 2018/2019, equivalent to target price of HK$ 33.1 and Buy rating.

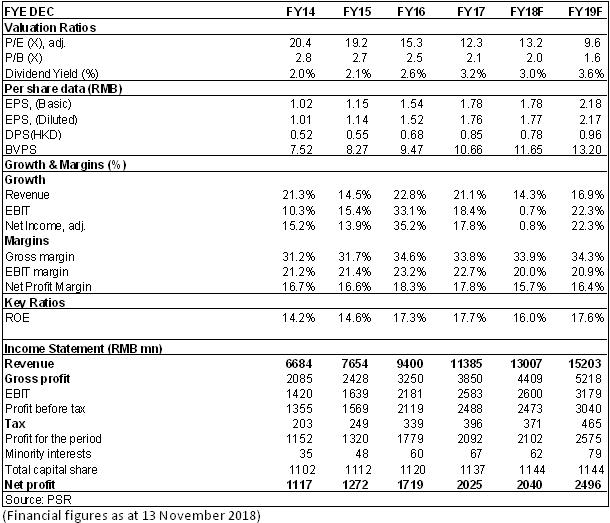

Financials

Click Here for PDF format...