Investment Summary

On Nov 14, the Chinese government approved the pilot program of centralized drug purchase, which will negatively affect CMS drug prices and lead to a potential profitability decline. We highlight the strong growth potential of CMS in long run and also the introduction of new products which will enrich the pipeline mix. We lowered the rating to Neutral with TP of HKD9.98. (Closing price at 21 Nov 2018)

Business Overview

Volume-based procurement policy was approved. VBP emphasizes that when bidding or negotiating the centralized purchasing of drugs, the purchasing quantity should be clearly defined, so that enterprises can quote price with consideration of the specific quantity. On Nov 14, the Chinese government adopted the pilot program for centralized drug purchase. In opposite to tenders without purchasing quantity (which tends to lead to no actual purchase later), VBP is expected to facilitate final purchasing, thus increase the sales of drugs, though generally reduce the drugs price.

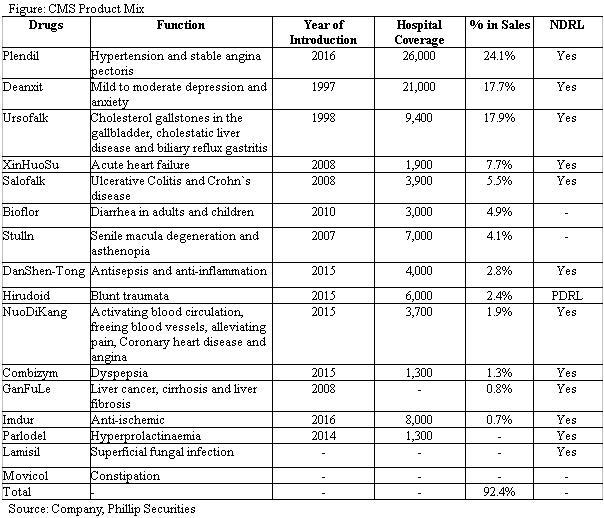

ASP of two main drugs will be adversely affected. The bid drugs should be ones passing the BE tests. The company will have two main products that may face fierce competition due to peers passing BE tests, namely, Deanxit (for treatment of depression) and Plendil (for the treatment of hypertension and angina pectoris). In a previous con-call, CMS illustrated that if it does not accept the price cut and quit tenders in 11 pilot cities, 20-40% market of the two would be transferred from hospitals to OTC market. Thus the sales revenue of the two will be reduced by 8.4-11.2% and the company's overall revenue will be reduced by 3.6-4.8%. If the policy effect extends from 11 pilot projects to the whole country and 20-40% market is transferred to OTC, the overall revenue may decline by 11.1-14.9%.

Purchase of R&D products. Except for Deanxit and Plendil, there are almost no competitors in other products of CMS, so we regard their market growth potential still strong. In Sep, the company announced the acquisition of exclusive, permanent R&D and commerce rights of VAXIMM AG, which owns pharmaceutical products (including VXM01, the leading product at present), in China, Singapore, Philippines, Korea, Malaysia and other designated Asian countries. VXM01 is an oral T cell immunotherapy consisting of live attenuated Salmonella typhimurium carrying eukaryotic expression plasmid encoding vascular endothelial growth factor receptor 2 (VEGFR2) gene. VXM01 will be mainly developed for the treatment of recurrent glioblastoma (GBM) at this stage. It has been designated as an orphan drug for glioma by EU and FDA of the United States.

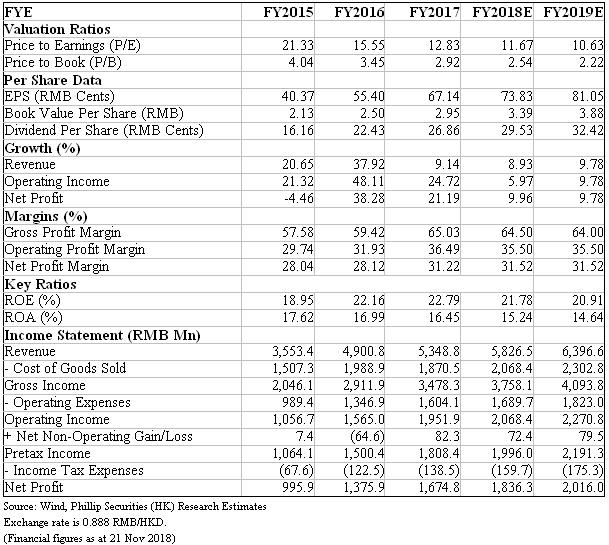

18H1 results. Total turnover fell by 1.2% to RMB2,655mn, while excluding two-invoice system revenue it increased by 10.3% yoy to RMB2,974.3mn. Gross profit increased by 13.3% to RMB1,883.7mn (excluding TIS effect up by 9.5% yoy to RMB1,744.9mn). In Jun 2018, its cash and bank deposits amounted to RMB1,097.8mn and bank acceptance drafts cashable at any time amounted to RMB245.5mn. The interim dividend is RMB0.1536 per share, up by 18.8% yoy.

�Investment Thesis, Valuation & Risk

We lowered the target price to HK$9.98. We slightly downgraded the revenue growth forecasts of Deanxit and Plendil, and adjusted EPS forecasts to be RMB0.74/0.81 in 2018E/19E. Based on target PE 12x (the peers` target median PE is 15x) we lower the target price to be HK$9.98, Neutral rating. Risks include: R&D fails expectations; Policy risks; Exchange risk; New introduction fails expectations. (Ex rate=0.888RMB/HKD)

Financials

Click Here for PDF format...