Investment Summary

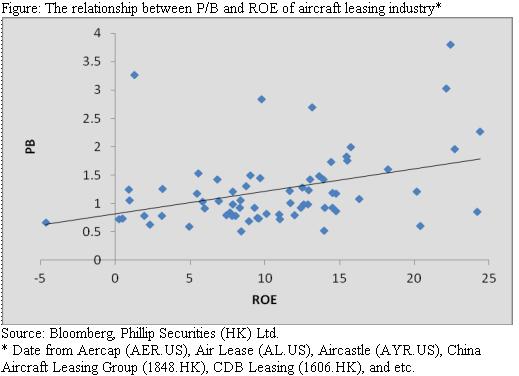

BOC aviation (BOCA) is a leading global aircraft operating leasing company in Asia, currently with a portfolio of 294 owned and 26 managed aircrafts. We remain an “Accumulate” rating based on a Price-to-book ratio vs. Return on Equity method, deriving a target price of HK$70.5, 18.5% potential upside. (Closing price at 23 November 2018)

Aircraft fleet

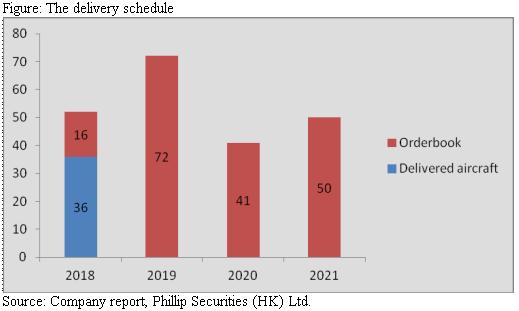

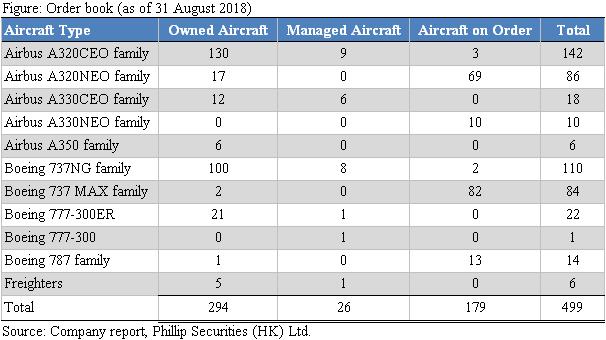

The total fleet of owned aircraft in 3Q18 was 294, dropped by 1 compared to 1H18. That of managed aircrafts was also down by 3 to 26, while the aircraft on order increased by 16 to 179, resulting in an increase in the total fleet of aircrafts of 12 to 499. BOCA sold 12 aircrafts in 3Q18, where 9 are owned and 3 are managed.

Aircraft delivery

In 3Q18, BOCA has delivered 9 aircrafts, where they delivered their first A321 NEO aircraft in August 2018. Meanwhile, it added three new airline customers to its customer portfolio. The Group expects there will be 16 aircrafts to be delivered in 4Q18, making a total delivery of 52 aircrafts in 2018. The delivery was six less than expected in 1H18, because of the manufacturer production delays. And, BOCA expects the problem takes 2-5 months to be resolved, meaning those have been deferred to 2019. However, the management believes there will be no significant influence in the 2018 bottom line, because a delay in the delivery will not bring any penalties. Meanwhile, BOCA has signed 35 lease commitments in 3Q18, further securing the portfolio utilization in the future.

PLB deals

There was no additional Purchase and lease back (PLB) deals in 3Q18, as the management claimed that airlines usually seek for PLB 12-18 months earlier before the aircraft delivery, implying that the PLB agreed now will be reflected in 2019.

Capex and Aircraft NBV

BOCA sees an increase of USD 2.5 billion in aircraft NBV, expecting a capex of USD 4 billion in 2018 and an offset of USD 0.5 billion in depreciation and 1 billion in aircraft disposal. Meanwhile, the capex will peak in 2019, and drop in 2020.

Average aircraft age and lease term

Based on the weighted net book value of owned fleet, the average fleet age rose by 0.1 to 3.1 years, and the average lease term dropped by 0.1 to 8.2 years.

Leverage target & proportion and dividend payout

BOCA still remains its target on leverage ratio to be 3.5x-4.0x, and continue to increase in the proportion of fixed rate loan, as it expects more fixed rate term coming up. Moreover, the Group has signed a single tranche unsecured term loan facility of USD 750 million in October 2018. Besides, it will cling to 35% annual payout ratio.

Valuation

We see the 3Q18 performance generally in line with our forecast, so we remain our target price to be HK$70.5 based on the NAV in 2019F, implying P/B 1.50x/1.36x/1.25x in 2018/19/20F respectively and maintain an “accumulate” rating. (HKD/USD: 7.8)

Risk

1. Higher-than-expected increase in interest rate

2. The demand for traveling and aircrafts slow down

3. Delayed aircrafts deliveries

4. Depreciating value for aircrafts in secondary markets

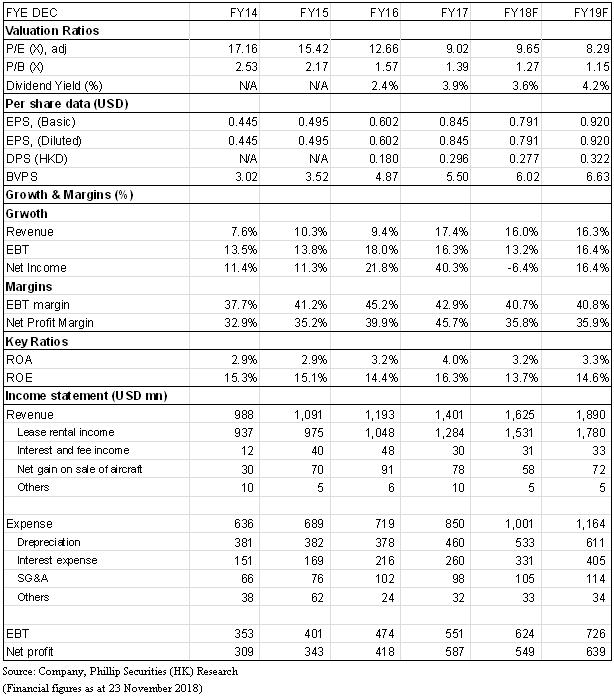

Financials

Click Here for PDF format...