Investment Summary

The State Council did not restart the cross-border e-commerce(CBEC)positive list policy at the end of the year, which is in line with our expectations. On this basis, it announced that from 1st January 2019, the current policy on CBEC retail imports will continue. No requirements of licensing, registration or record-filing for first-time imports shall apply to the retail imports through CBEC platforms, but receive regulation as personal use.

This shows that the policy direction has been further relaxed. The State Council also extend the implementation of this policy from 15 cities such as Hangzhou to another 22 cities such as Beijing which have just established comprehensive CBEC pilot zones. Goods included in the CBEC retail imports list have so far enjoyed zero tariffs within a set quota and had their import VAT and consumer tax collected ar 70% of the statutory taxable amount. Such preferential policies will be extended to another 63 tax categories of high-demand goods. The quota of goods eligible for these preferential policies will be raised from RMB2,000 to RMB5,000 per transaction and from RMB20,000 to RMB26,000 per head per year.

We believe that the new measures show the Chinese government's positive stance on support and encouragement for the long-term and steady development of CBEC, eliminating the market's earlier concerns about the risk of policy changes in the industry. Moreover, under the current Sino-US trade war, it will also help to demonstrate China's determination to further open up the market, promote diversification and steady growth of imports, and stimulate domestic consumption and employment.

At the same time, the first import of goods categories like cosmetics, nutritional supplements and infant formula through ECBC will no longer be subject to regulatory restrictions, which will help H&H's Swisse products that rely on ECBC entering China market, including non-vitamin SKUs which will be negatively affected under positive list.

-In the past 11th November, the company launched new products such as oral-intake hyaluronic acid and collagen jelly, and recorded good results. According to Tmall's statistics, Swisse is the number one brand in both imported and health care categories.

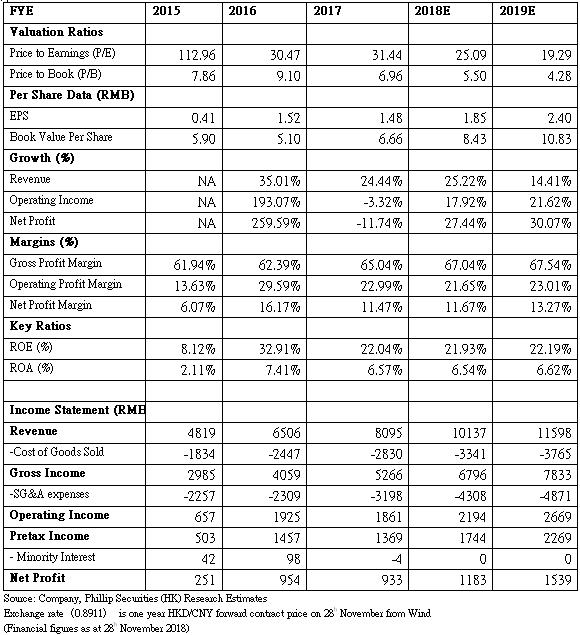

-In the middle of September, the company redeemed the value of RMB 125 million in bonds through its own cash and bank loans. We expect this can continue bringing down the financial cost and is expected to decline year by year in the next two years. We give forecast P/E ratio 23.9 times, the corresponding target price HKD60.72. (current price as of November 28, 2018)

Business Overview

New acquisition

For BNC, during Q3, the company completed the acquisition of “Good Gout”, the fastest growing organic baby food company in France, costing 20 to 30 million euros. The management team hopes through the acquisition, it can better capture the strong growth momentum of organic baby food segment in France, China and international markets.

For ANC, it had completed the progressive transfer of Swisse distribution rights from PGT by the end of last June. It now has the full ownership of the rights in Hong Kong, Singapore, Italy, Netherlands and the United Kingdom. However, the newly added market is smaller and contributes less than 5% to the ANC business. Therefore, the growth in Q3 is mainly from the original China and Australia.

Q3 performance review

For BNC, during Q3, the company completed the acquisition of “Good Gout”, the fastest growing organic baby food company in France, costing 20 to 30 million euros. The management team hopes through the acquisition, it can better capture the strong growth momentum of organic baby food segment in France, China and international markets.

For ANC, it had completed the progressive transfer of Swisse distribution rights from PGT by the end of last June. It now has the full ownership of the rights in Hong Kong, Singapore, Italy, Netherlands and the United Kingdom. However, the newly added market is smaller and contributes less than 5% to the ANC business. Therefore, the growth in Q3 is mainly from the original China and Australia.

-In Q3, H&H's overall revenue rose by 27.3% y.o.y to RMB 2.745 billion , and the first three quarters rose by 28.2% y.o.y to RMB 7.326 billion. For ANC business, revenue increased by 40.8% y.o.y in Q3., higher than 29.3% in the first three quarters (36.6% on a currency-adjusted basis), which is higher than 30% of the management's full-year guidance (with currency adjustment). The reasons for the acceleration in Q3 include the company increased its product supply to meet market demand and strong demand in China market.

As the company's new products are about to be launched and begin contributing revenue, we expect that the fast growth trend of ANC will continue in Q4. Two new online products (pregnancy and baby health products and adult probiotic products) are expected to have a significant contribution from Q4.

In Q3, BNC (infant nutrition and care products) increased by 17.8% y.o.y. Revenue of infant formulas was increased by 17.9%, mainly driven by high-end and ultra-high-end products. The growth of organic milk powder remained rapid. Revenue of BNC and infant formulas in the first three quarters increased 27.4% and 23% respectively, reflecting the one-time replenishment factor of the newly registered milk powder product distributors in 1H of the year, but it was in line with the management's annual guidance of above 20%.

Revenue of probiotics supplements increased by 15.4% y.o.y., significantly lower than the 45.2% in the first three quarters, reflecting the one-time replenishment factor in the first quarter, which was out of stock at the end of last year, and the base factor. However, it is still higher than about 30% of the annual guidance. Revenue of other infant products increased by 24.9% y.o.y. in Q3, and 40.7% y.o.y. for the first three quarters.

Maintain mid-year guidance / market share

- The company has positioned this year as investment year, and will continue to increase spending on marketing activities, but will ensure profit growth. The guidance for BNC and ANC EBITDA will remain at 20% and 30% respectively. The management team has confident to achieve.

As of the end of September, the company's market share of infant formula in China was 5.9%, which was the same as that in 12months by the end of June, up from 5.5% in 12months by the end of September. Swisse's market share of vitamins, herbal and mineral supplements in Australia increased from 16% in 12 months by the end of September to 18.9% in 12 months by the end of September, and 18.6% higher than the 12 months ended in June.

Investment Thesis & Valuation

We give forecast P/E ratio 23.9 times, the corresponding target price HKD60.72. Potential investment risks include revenue growth and channel expansion not meeting expectation, policy changes and the competition of infant milk powder market deteriorating (current price as of 28th November, 2018)

Financials

Click Here for PDF format...