Investment Summary

2018Q3 result stopped falling Y-o-Y with a surge of 1.8 times Q-o-Q

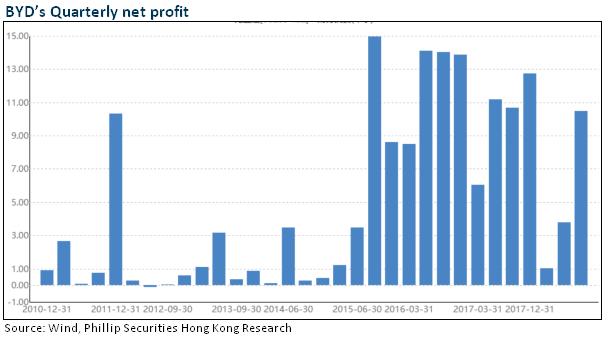

Data in BYD's report of the third quarter show that the revenue was increased by 20.5% Y-o-Y to RMB34.83 billion in the third quarter of 2018; the net profit attributable to shareholders was RMB1,048 million, a slight decrease of 1.92% Y-o-Y. Compared with the previous two quarters when BYD's earnings performance declined sharply, the profit status in the third quarter was much better: In the first and second quarter, BYD's net profit attributable was decreased by 83% and 66% Y-o-Y, respectively to RMB102 million and RMB377 million. In the third quarter, the profit stopped decreasing and returned stable, driving the accumulated reduction of BYD's profit in the first three quarters to slow down, leading to a decrease of 45.3%. The Company predicted that the change in the annual net profit would be from -32.94% to -23.1% Y-o-Y in 2018. Upon estimation, the profit in the fourth quarter of the Company would be from RMB1.2 billion to RMB1.6 billion, an increase of -5.66%-25.49% compared with the same period of last year.

The GM/cash flow both improved, while the financial expenses still enormous

With the end of the transition period, the sales volume of BYD's new energy vehicles hit the lowest point and then rebounded, facilitating the rapid recovery of its profitability. In the third quarter, the gross margin of the Company was increased by 2.3 percentage points to 17.2% Q-o-Q and decreased by 1.9 percentage points Y-o-Y. The ratio of expenses to sales was decreased by 0.1 percentage point Y-o-Y, while the ratio of administration expenses to sales was basically the same; the financial expenses set a new record, an increase of RMB190 million to RMB850 million Y-o-Y, and the financial expense ratio was up by 0.1 percentage point, exerting certain negative influence on profitability. However, other earnings made by the Company in the same period were up by RMB320 million compared with the same period of last year to RMB560 million. In the third quarter, the operating cash flows recorded a net inflow of RMB8.26 billion, nearly double that of the same period of last year, and the net outflow was greatly improved compared with the first half year.

The new generation of Dragon Face, vehicles of BYD Dynasty series, embraced a strong product cycle

From 2017H2 to 2018Q3, BYD launched multiple full-scale redesign, degeneration and facelift models for its Dynasty brand series. In these models, BYD made noticeable improvements in power, appearance and configuration etc., promoted the user experience greatly and facilitated the strong growth of the sales volume. The selling price of the new generation of Tang vehicles exceeded RMB200,000 and is still highly popular among buyers, which fully displays the strength of the new generation of the Dragon Face vehicles of the Dynasty series.

In October 2018, the Company recorded a sales volume of 48,497 vehicles, an increase of 30% Y-o-Y. In the first ten months, the accumulative sales volume was approximately 400,000 vehicles, an increase of nearly 30% Y-o-Y, exceeding the annual sales volume of 13% in 2017.

From the perspective of different types, the sales volume of the new energy vehicles reached 27,667 in October, a slight decrease M-o-M, and an increase of over 100% Y-o-Y. In the first ten months, the accumulative new energy vehicles sales arrived at 171,085, an increase of nearly 66% Y-o-Y, and the market share was 22.5%. Among others, the sales volume of the new energy buses was 9,301 in the first ten months, and the market share was increased from 12% in 2017 to 17%.

In terms of fuel vehicles, the Company sold 20,830 vehicles in October, an increase of 4.1% M-o-M, and a decrease of 11% Y-o-Y. The sales volume in the first ten months was 228,930, an increase of approximately 10% Y-o-Y, among which, the high-end MPV Song MAX models occupied more than half, conducive to the improvement of the average sales price.

The new battery projects are gradually put into operation, which will release the bottleneck of the capacity

From the end of 2018 to the beginning of the2019, the Company will launch MPV model Song MAX PHEV, SUV model Tang EV600 and others. At present, the Company has good terminal sales demand, and the orders for some hot-sale models exceed the supply due to the bottleneck of the battery capacity. As at the end of 2017, the total capacity of BYD's power batteries was 16Gwh (10Gwh LFP batteries + 6Gwh ternary batteries). This year, BYD expanded 24Gwh capacity of ternary batteries in Qinghai, which will be completed in two phases. The first phase starting from June has been putting into operation and is expected to reach the target output by the end of the next year. The Company has sign contracts of the 20Gwh Chongqing Project and the 30Gwh Xi`an Project. In 2019, the Company plans to split its battery segment and make it listed independently, which will improve the valuation level of its battery business hopefully. As the battery capacity is being put into operation gradually, and with a large number of orders in hand, the new energy vehicles of the Company are expected to grow rapidly.

Investment Thesis

Although the results of BYD in 2018 are below our expectation, the technological improvement, transformation and implementation of BYD in recent years have activated its overall competitiveness again. The Company will fulfill its results. We believe that the Company has made forward-looking preparation for all kinds of challenges and its leading position will be enhanced. We are optimistic about the more stable and sustainable growth of the Company in the future.

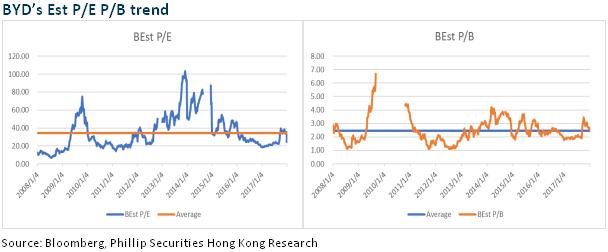

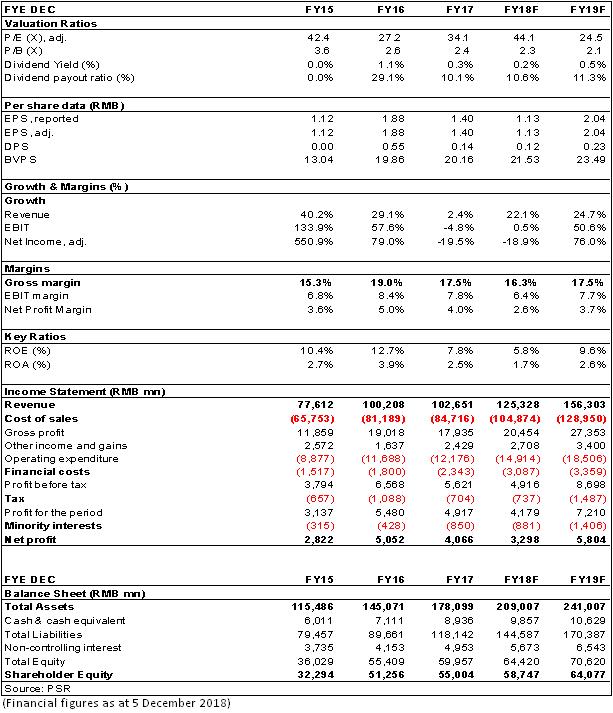

As the latest estimates, we revise the target price to HKD63, which corresponded to 2.5/2.3x P/B ratio for 2018/2019. We give the rating of “Accumulate”. (Closing price as at 5 December 2018)

Risk

Sales of new energy vehicles is not as good as expected

Cloud Rail business risk

Slow-down of Hand-set components business

Financials

Click Here for PDF format...