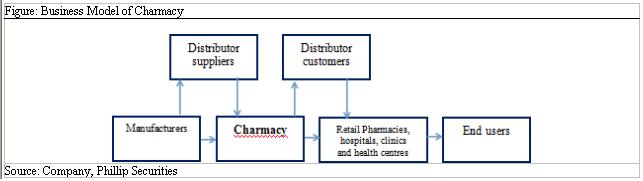

Business Overview

-Charmacy is dedicated to pharmaceutical distribution business. Its predecessor is founded in 1984, as a logistics and resources centre to supply raw materials and imported Chinese and western medicines to various units within the organization. The listed company was set in 2000. In 2011, the company set up logistic center in Foshan city. During 17H1, two subsidiaries were built in Zhuhai and Guangzhou, and in 18H1 a new branch in Shenzhen was established.

-A leading pharmaceutical distributor in Southern China. In 2016, the company ranked 37th among top 100 wholesalers nationally, in respect of principal business. According to a market research report (《中國醫藥行業市場研究報告》(2016)), in respect of sales scale, the company ranked 7th among the pharmaceutical distribution businesses in Guangdong Province and second among private firms. The company adheres to the strategy of intensive engagement in Guangdong and extensive coverage across surrounding areas. It has established logistics centers in Shantou, Foshan, Zhuhai and Guangzhou, equipping with professional transport teams. It has a highly efficient delivery mechanism of delivering pharmaceutical products three times per day for customers within a radius of 10 km, twice per day for customers within a radius of 50 km and once per day for those within a 250-km radius. Since 2015, the company has operated its own B2B e-commerce platform Charmacy e-Medicine (創美e藥), which at present, has 4,912 active trading customers, mainly end-users such as retail pharmacies, clinics and heal centers.

-Products portfolio. The company distributes medicines including western medicine, Chinese patent medicine, health products and etc. To improve its product mix, Charmacy increases the variety and scale of primary distribution products, and phases out some of the products with low gross profit margins and turnover rate. In 18H1, the company distributed 10,145 products, rising by 528 varieties (vs. 9,617 varieties in 17H1). Among them, the number of Chinese patent drugs increased by 890 to 3,436, and that of Western medicine decreased by 586 to 3,557. The number of products which Charmacy distributed as a primary distributor, increased from 5,542 in 2017 to 7,996 at present.

-Customer structure. Charmacy now covers 7,124 customers (17H1:6,330 customers), among which distributor customers and retail pharmacies contributed to 97% of total revenue. After the implementation of two-invoice system, the company continues to optimize client structure, reduce the proportion of distributor customers, and increase direct sales (given the number of retail pharmacy customers rose by 730 to 4770 in 18H1, and that of hospitals, clinics and health centers was up by 22).

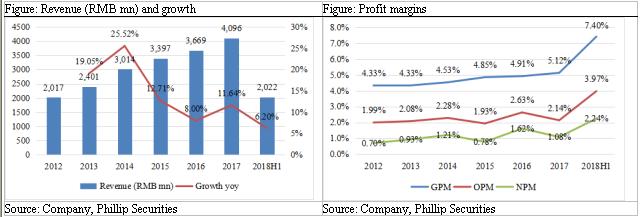

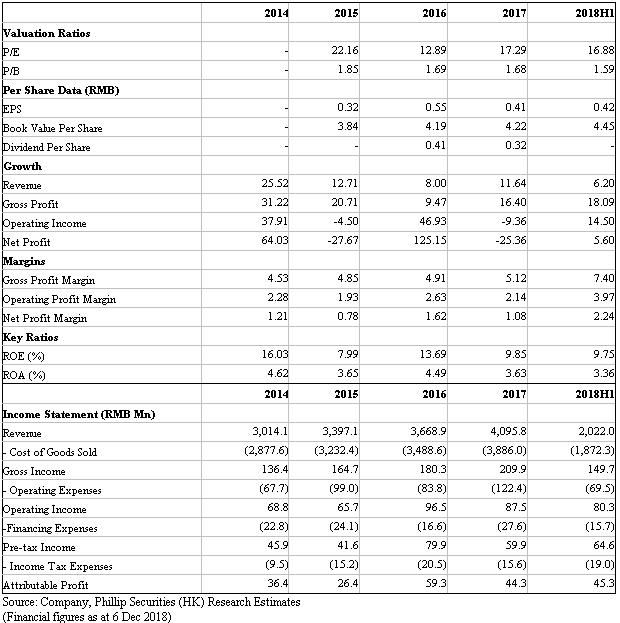

-Financial performance. From 2012 to 2017, its revenue achieved a CAGR of 15.22%, and net profit maintained a CAGR of 25.7%. In 2018, Charmacy's operating income increased by 6.2% to RMB2022mn, and net profit increased by 5.6% to RMB45.3mn. We highlight that its profit margin has continued to improve. In 18H1, GPM rose by 0.74ppts to 7.4%, mainly due to the reduction of VAT tax rate (from 17% to 16%) and the ramp-up of Chinese patent medicine products which have relatively higher GPM. Sales expenses increased by 12.5%, mainly attributing to warehouse rental fees for the newly established sites in Guangdong and Zhuhai, as well as moderately rising logistics costs. Besides, management costs was up arising from compensation to new staff of two new sites, and depreciation for newly-bought properties. However, due to the dramatic growth of operating income and the improvement of gross profit, the adjusted operating profit margin rose to 3.97% in 18H1.

Q&A Summary

We participated in the site visit organized by the company to the Foshan logistics distribution center. Located in Chancheng Distric, the center has a storage area of 21,300 sqm and can store 190,000 items, supporting sales of RMB3.36bn.

Q: What are the trends in the number and structure of distributor clients?

A: The number of our customers is showing an upward trend, mainly due to the continuous expansion of terminal networks such as retail pharmacies, clinics and health centers. In 18H1, we provide products and services to 7,124 clients.

Q: What customers are mainly covered by B2B platform (Charmacy e-Medicine)?

A: In 18H1, the platform has 4,912 active trading customers. The main customers of the platform are hospitals, clinics, and small and medium-sized pharmacies, etc. This platform provides customers with services, such as inquiry, order, payment, etc.

Q: What are gross profit margins of three major channels?

A: 2017 data shows that, GPM of distributor segment is the lowest (around 3.33%). Because the trade-off of large quantity and lower purchasing price finally leads to lower profitability. GPM of retail pharmacies is 5.83%. Highest GPM is from hospitals, clinics and health centers, around 14.73%, because individual consumers are not that sensitive to price. GPM rose from 4.54% in 2014 to 5.12% in 2017. We expect GPM to climb further, given improving client structure and product mix.

Q: Accounts receivables of three types of customers?

A: For newly developed small customers, we usually collect cash when delivery. For long-term cooperative distributors and chain pharmacies, the receivables` days are longer. We proactively manage accounts receivables, and the balance fell from RMB883 million at the end of 2017 to RMB757 million by this June end.

Q: What is the marketing strategy? Will it expand beyond Guangdong Province?

A: We started from Shantou, expanded to Eastern Guangdong, and then to the entire Pearl River Delta. Usually when we entered a new market, it takes time to cultivate the market. For example, we acquired Zhuhai site last year. In this October, we see its customer base and profits grow steadily. In future, we will further expand the market scale by relying on affluent primary distribution rights in Guangdong Province.

Q: Which pharmacies do the company cooperate with more?

A: Main pharmacy chains in Guangdong are almost our customers, with deep cooperative relationships for many years. Major pharmacies, such as Dashenlin and Nepstar, place orders at least 2-3 times a week.

Q: What is the dividend policy?

A: Still more than 20% of distributable profit will be distributed every year.

Q: Why did financial costs in 2017 rise?

A: The financial expenses in 2017 were RMB27.61mn, up by RMB17.34mn from RMB10.27mn in 2016. This is because of 1) exchange losses caused by exchange rates fluctuations of RMB and HKD, 2) expansion of financing scale led to an increase in interest expenditure, and 3) increasing inventory volume. (The inventory amounted to RMB352mn in 2016 and rose to RMB432mn at the end of 2017.)

Q: Please introduce the investment in Guangzhou? What will be growth prospects for future 2-3 years

A: Last July, we purchased property located in Nansha, Guangzhou, with RMB131mn. The expenditure was paid off (with RMB80mn of bank loans and RMB50mn through self-funding). We expect to invest RMB145mn to build Guangzhou distribution center, and has received long-term loans from ICBC. About 35mn will be put this year, and the rest will be invested in 2019. Average bank lending rate last year was about 5.2%. This year, because the discount rate on bank acceptance bills has been lowered, the overall interest rate level will not rise.We start to operate Nansha center on May 1st 2018. Sales revenue in the past few months meets our expectations, with average monthly income about RMB22mn.

Q: Dose informatization construction significantly improve profitability or efficiency?

A: Informatization projects can improve the overall logistics operational efficiency. From the end of first half, the number of logistics personnel did not increase compared with past.

Q: How about the company's refrigerated drug transportation business?

A: We now carry out distribution business of refrigerated products. As of June end, the company has 61 refrigeration vehicles, accounting for about two-thirds of total delivery vehicles. We expect that the proportion will still increase in the future. We know from our checks that government may come up with stricter requirements towards drug distribution vehicles and our refrigeration vehicles will be competitive for future.

Financials

Click Here for PDF format...