|

|

|

*Advertisement* |

|

|

|

|

|

19 Dec, 2018 (Wednesday) |

PERFECT SHAPE(1830)

Analysis:

Perfect Shape Medical Limited (1830) announced that in connection with the Potential Spin-off of the PRC and Macau businesses of the Group on a stock exchange in the PRC, the Group was notified by the Hong Kong Stock Exchange that the Listing Committee had agreed that the Group may proceed with the Potential Spin-off under Practice Note 15 of the Listing Rules. The Potential Spin-off and the Listing, if proceeded, will better position the Group as well as the spun-off entity for growth in their respective lines of business. The Group has established a network in China and Macau. As at end of September 2018, the Group operated direct service centers in five metropolitan cities, i.e. Beijing, Shanghai, Guangzhou, Shenzhen and Macau. (I do not hold the above stock)

Strategy:

Buy-in Price: $2.05, Target Price: $2.25, Cut Loss Price: $1.95

|

|

MOBVISTA(1860)

Analysis:

The company is a leading technology platform for global application developers to provide mobile advertising and mobile analysis services, based on its strong big data system. Its customers are application developers. The company carries out cost-effective publicity activities for them in different media, and charges based on advertising effect (i.e. customer traffic generated). Its revenue increased from US$167.2mn in 2015 to US$313mn in 2017, with an average compound annual growth rate of 36.8%, and delivered revenue of US$184.5mn in 2018H1. Profit increased from US$8.7mn in 2015 to US$27.3mn in 2017, with a compound annual growth rate of 77%, which reached US$10.1mn in 2018H1.

Strategy:

Buy-in Price: $3.90, Target Price: $5.00, Cut Loss Price: $3.50

|

| |

|

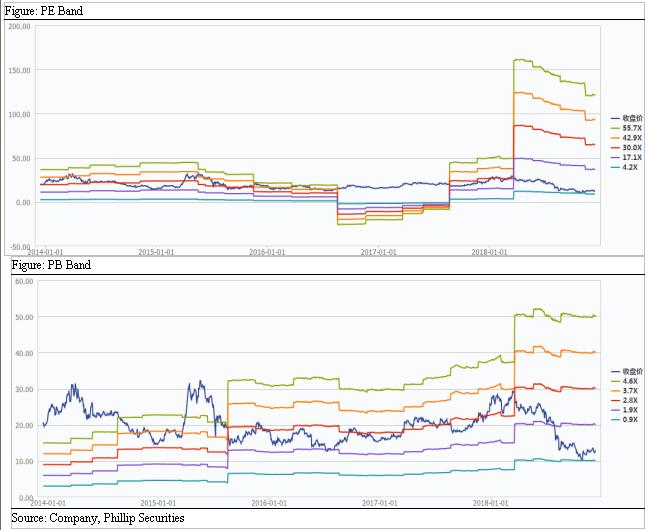

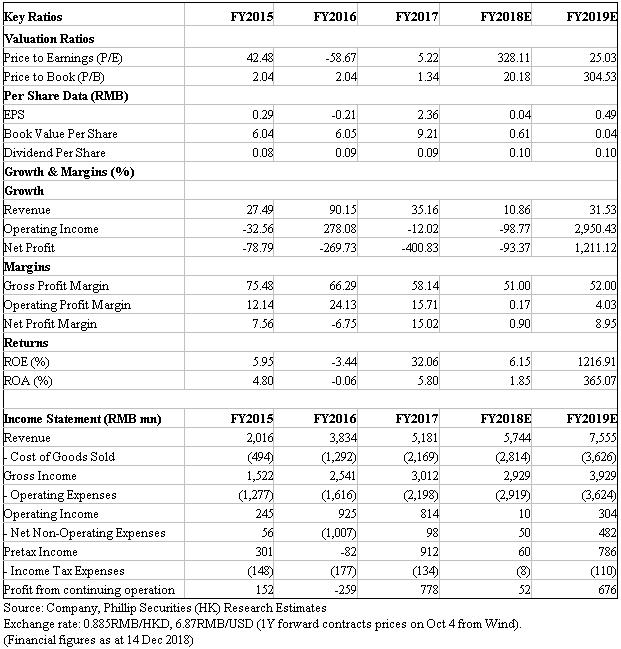

Kingsoft (3888.HK) - 18Q3 Reporting Losses; Expected Improvement Next Year

Investment SummaryKingsoft reported loss in 18Q3, given game revenue declined, while cloud services and WPS software delivered notable growth. We maintain the target price of HK$18.8, BUY rating. (Closing price at 14 Dec 2018) Business OverviewLosses in 18Q3. Kingsoft reported revenue in 18Q3 of RMB1,537.7mn, up by 18% yoy and 14% quarter-over-quarter. Revenues from online games, cloud services, WPS office software accounted for 44/39/17%, respectively. Gross profit decreased by 7% to RMB694.5mn, up 3% from 18Q2. Gross profit margin was 45%, 12ppts lower than 17Q3 and 5ppts lower than the previous quarter, mainly due to changes in business portfolio. The loss attributable to the parent company is RMB59.3mn (2017Q3: 238.5mn; 18Q2: 100.9mn). Before deducting the cost of share package, the loss attributable to the parent company amounts to RMB21.6mn, representing a net loss rate of -1% (2017Q3: 306.7mn, 12%; 18Q2 138.9mn, 10%). Online game revenue declined. The revenue of 18Q3 online game business was RMB678.3mn, down by 9% yoy and up 17% qoq. It is because that existing games entered natural decline period, though the decrease is partly offset by the rising contribution of newly launched mobile games (mainly due to the contribution of JX II released on iOS platform in July). Daily average peak concurrent users is about 0.7 million, down 16% yoy and 9% qoq. The average monthly paying accounts is RMB3.4mn, down 16% yoy and up 5% qoq. Cloud business has grown significantly. It contributes RMB603.3mn in revenue, up 68% yoy and 29% qoq. The growth is mainly due to the steady increase in mobile video and Internet businesses. WPS office software revenue maintained momentum. This segment reported revenue of RMB256.1mn, up by 29% yoy and down 13% qoq. The growth was mainly attributed to the rapid growth of revenue from WPS Office personal value-added services. By providing members with useful functions and content services, the company improves user stickiness. The decline in revenue was mainly due to seasonal effect. Valuation & Risks We maintain our target price of HK$18.8. Next year is likely to experience improvement. New games (JX II and JX III mobile) will be launched in 19H1, and revenue from game business is expected to recover in 2019. Monetization of WPS office software will continue through providing more qualified value-added services to users. Cloud business will continue to expand leveraging on exploring advantage areas. Downside risks include: Revenue growth fails expectations; Exchange rate risk; Policy risks.

Financials

Click Here for PDF format...

| Recommendation on 19-12-2018 | | Recommendation | BUY | | Price on Recommendation Date | $ 12.320 | | Suggested purchase price | N/A | | Target Price | $ 18.800 |

| |

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the “Group”) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products’ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

版權所有, 翻印必究。

Copyright(C) 2018 Phillip Securities (HK) Ltd. All Rights Reserved.

|