|

|

|

*Advertisement* |

|

|

|

|

|

20 Dec, 2018 (Thursday) |

TIME INTERCON(1729)

Analysis:

Time Interconnect Technology (1729) primarily manufactures and supplies a wide range of cable assemblies which are produced in accordance with the specifications and designs of individual customers. Its products are widely used in a variety of market sectors including telecommunications, data centre, industrial and medical equipment. Despite the overall slowdown in the growth of the global economy, the Group reported solid operating results in the six months ended 30 Sep. Its revenue increased by 35.1% to HK$835 million. All of its business sectors have different degrees of increase in revenue. Total profit increased by 10.5% to HK$88.4 million. In order to satisfy future demand, the Group decided to acquire a parcel of industrial land which is located about 1.2 km away from the Group`s existing Huizhou factory. The acquisition will increase the production floor area by about 32,400 sq.m. which will offer more than 120% of the increased production capacity. (I do not hold the above stock)

Strategy:

Buy-in Price: $0.46, Target Price: $0.51, Cut Loss Price: $0.435

|

|

UCD(1599)

Analysis:

The company is dedicated in the design, survey and consultancy segment as well as the construction contracting segment (in particular, urban rail transit). We see that macroeconomic policies were tightened, rail transit investment slowed down, and market competition became more intense. In 18H1, BUCDD realized income of RMB3.418bn, up by 12.73% yoy. Net profit reached RMB269mn, up by 19.03% yoy. In July 2018, Chinese government issued a file in which it decided to further improve the application standards for subways and light rails, and further standardize the review and approval of relevant administrative matters. Successively it approved the construction of urban rail transit projects in Changchun, Suzhou, etc. Looking forward, the company adheres to growth as main line, further strengthens the design and consultancy business and construction contracting business, and expands new business. Considering the accelerated infrastructure investment from 18H2, the company`s orders are expected to continue solid growth in the next few years.

Strategy:

Buy-in Price: $2.48, Target Price: $3.00, Cut Loss Price: $2.00

|

| |

|

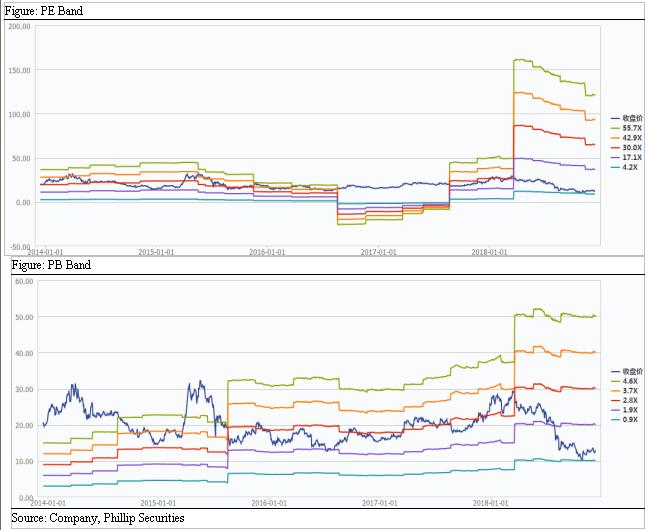

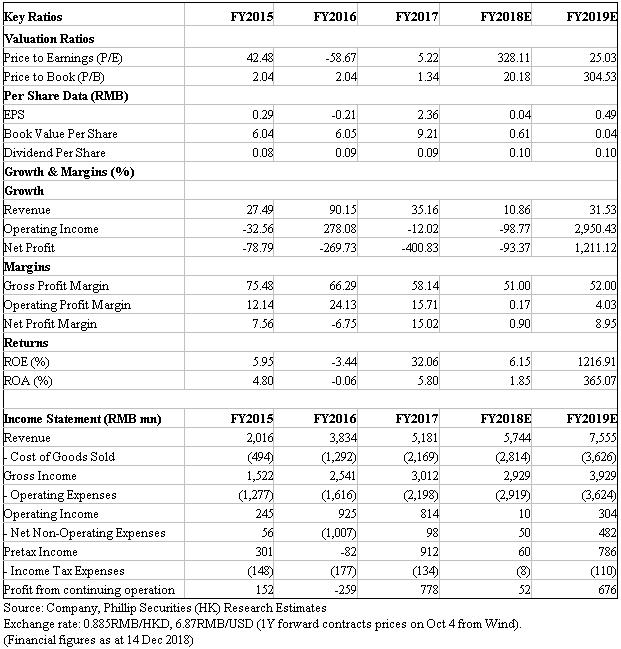

Kingsoft (3888.HK) - 18Q3 Reporting Losses; Expected Improvement Next Year

Investment SummaryKingsoft reported loss in 18Q3, given game revenue declined, while cloud services and WPS software delivered notable growth. We maintain the target price of HK$18.8, BUY rating. (Closing price at 14 Dec 2018) Business OverviewLosses in 18Q3. Kingsoft reported revenue in 18Q3 of RMB1,537.7mn, up by 18% yoy and 14% quarter-over-quarter. Revenues from online games, cloud services, WPS office software accounted for 44/39/17%, respectively. Gross profit decreased by 7% to RMB694.5mn, up 3% from 18Q2. Gross profit margin was 45%, 12ppts lower than 17Q3 and 5ppts lower than the previous quarter, mainly due to changes in business portfolio. The loss attributable to the parent company is RMB59.3mn (2017Q3: 238.5mn; 18Q2: 100.9mn). Before deducting the cost of share package, the loss attributable to the parent company amounts to RMB21.6mn, representing a net loss rate of -1% (2017Q3: 306.7mn, 12%; 18Q2 138.9mn, 10%). Online game revenue declined. The revenue of 18Q3 online game business was RMB678.3mn, down by 9% yoy and up 17% qoq. It is because that existing games entered natural decline period, though the decrease is partly offset by the rising contribution of newly launched mobile games (mainly due to the contribution of JX II released on iOS platform in July). Daily average peak concurrent users is about 0.7 million, down 16% yoy and 9% qoq. The average monthly paying accounts is RMB3.4mn, down 16% yoy and up 5% qoq. Cloud business has grown significantly. It contributes RMB603.3mn in revenue, up 68% yoy and 29% qoq. The growth is mainly due to the steady increase in mobile video and Internet businesses. WPS office software revenue maintained momentum. This segment reported revenue of RMB256.1mn, up by 29% yoy and down 13% qoq. The growth was mainly attributed to the rapid growth of revenue from WPS Office personal value-added services. By providing members with useful functions and content services, the company improves user stickiness. The decline in revenue was mainly due to seasonal effect. Valuation & Risks We maintain our target price of HK$18.8. Next year is likely to experience improvement. New games (JX II and JX III mobile) will be launched in 19H1, and revenue from game business is expected to recover in 2019. Monetization of WPS office software will continue through providing more qualified value-added services to users. Cloud business will continue to expand leveraging on exploring advantage areas. Downside risks include: Revenue growth fails expectations; Exchange rate risk; Policy risks.

Financials

Click Here for PDF format...

| Recommendation on 20-12-2018 | | Recommendation | BUY | | Price on Recommendation Date | $ 12.320 | | Suggested purchase price | N/A | | Target Price | $ 18.800 |

| |

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the “Group”) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products’ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

版權所有, 翻印必究。

Copyright(C) 2018 Phillip Securities (HK) Ltd. All Rights Reserved.

|