Investment Summary

SUNeVision is one of the leading carrier-neutral data center operators in Hong Kong, owned 74.04% by Sun Hung Kai Properties (16.HK). On December 12, the Group announced that it has successfully acquired a data center land site in Tseung Kwan O for HK$5.46 billion. If the judicial review is successful, it could undermine the data center operators in Tseung Kwan O industrial estate and even help the Group to monopolize the area. But, we expect the gearing ratio to increase significantly. Considering the increase in interest expenses, we give a target price of HK$5.67. Due to the recent stock price correction, we upgraded the rating to “Buy” with a potential upside of approximately 21.15%. (Closing price at 20 Dec 2018)

Corporate Update

Successfully acquisition of a data center site in Tseung Kwan O for a total consideration of HK5.46 billion

On December 12, the Group announced that it has successfully acquired a data center site in Tseung Kwan O for HK$5.46 billion. The land area is approximately 295,407 square feet. The upper and lower limits of the total gross floor area are 1,212,457 and 727,474 square feet respectively, implying at HK 4,503 per sq. ft. If the upper limit is taken, the scale will be nearly 2.5 times larger than the Mega Plus. In addition, for those three data center sites previously allocated by the government in Tseung Kwan O, the first one has been acquired by the group in 2013, and this time the two remaining sites for data center were combined for sale. Meanwhile, since 2015, the industrial estates under the Hong Kong Science and Technology Park have no longer approved any lease for a single user to build their own factories. In other words, there is currently no land supply in Tseung Kwan O.

Land price

The price is significantly higher than the market expectation of HK 3,100 per sq. ft., which is close to 45%. Compared with the site that was acquired by the group in 2013 (Mega Plus), the price per sq. ft. (HK 904) is also nearly five times higher. We believe that the attractive price in 2013 is no longer existed due to the rising demand for data centers and lack of data center land supply. However, we believe that the price of the land acquisition is too high, making the project return rate not too attractive.

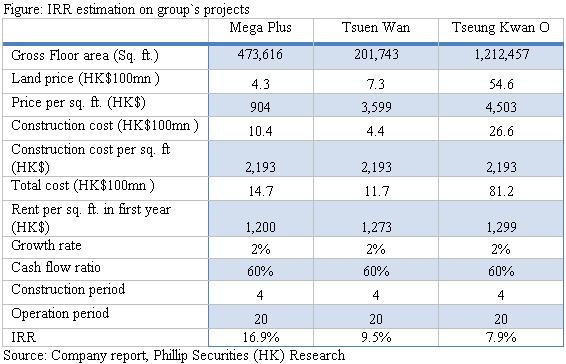

In our estimation of the IRR on the group's projects, we assume that the construction cost per sq. ft. of Tsuen Wan and Tseung Kwan O projects is the same as that of the Mega Plus. As construction costs will rise along with inflation, we believe that the actual construction cost per sq. ft. of the Tsuen Wan and Tseung Kwan O projects should be higher than that of Mega Plus. However, without actual data, we believe that the construction cost per sq. ft. of Mega Plus is a reasonable estimation input. In addition, we assume that Mega Plus's rent per sq. ft. in the first year is HK$1,200 (including other value-added service revenue), which is about 20% higher than the rent of the Group. Since Mega Plus mainly serves high-end tenants, we believe that its rent will be higher than other data centers of the Group. We also expect an annual rent growth of 2%, 60% of cash flow ratio, four years of construction period, construction costs to be shared equally within the period, and twenty years of operation periods. Since the Tsuen Wan and Tseung Kwan O projects are expected to be completed in 2021 and 2022 respectively, we assume that the rent for each in the first years will be the rent for Mega Plus for the corresponding year.

According to estimates, Mega Plus has the highest IRR, about 16.9%, mainly due to a very cheap land price at the time. The IRR for the Tsuen Wan and Tseung Kwan O projects was 9.5% and 7.9% respectively, much lower than Mega Plus. If the construction cost has been adjusted along with inflation, the IRR of the Tsuen Wan and Tseung Kwan O projects should be lower than the current level.

Considering the IRR alone, we believe that the return rate of this project is not attractive. However, the above analysis ignores the synergies between the Mega Plus and Tseung Kwan O projects.

Benefits

We tend to believe that this expensive acquisition is a strategic move of the Group, which might be related to the judicial review with Hong Kong Science and Technology Parks Corporation, alleging that it is indulging its tenants for sub-leasing to third parties in the industrial estates. It is allegedly some operators in Tseung Kwan O industrial estates are taking advantage of the grey area in the lease terms to provide subletting. Currently, there are nine data center operators in the industrial estate, including: China Mobile, NTT Communications, HKCOLO and Digital Realty Trust. If the loophole is closed due to the success in judicial review, the operators in TKO industrial estate may be either slapped with penalties or forced to cease the lease agreement. This means that if the government stops looking for land supply in Tseung Kwan O and Tseung Kwan O industrial estate cease the lease with data center operators, the Group will monopolize the data center supply in Tseung Kwan O and become the only data center in the region that can sublet. Therefore, we believe that this land acquisition has a strategic consideration. If succeed, it will greatly enhance the moat of the group's data centers. From the land price that is 45% higher than market estimation, it shows that the Group is so determined to acquire this site.

As for the judicial review, we believe that the main point of the judgment is how the court defines the term "subletting". Since the leases in industrial estate are subsidized by the government, so it is lower than market price, implying that sub-leasing mush be prohibited in this case. However, the question of what is "subletting" is controversial. At present, there are two explanations on the market: (1) renting cabinets is an action of sub-leasing and (2) renting cabinets alone is not an action of sub-leasing, as long as the land use rights are not in the third party, that is, the employees of the third party cannot stay and manage the servers.

If "sub-leasing" is defined as the first explanation, the data center of Tseung Kwan O industrial estate will be considered as illegal. The Science and Technology Park should cease the contract with them, enabling the Group to successfully monopolize the data center supply of Tseung Kwan O. However, Tseung Kwan O industrial estate provides a large supply to the Hong Kong data center market and is also the location of the data center of the Hong Kong Stock Exchange. Considering that the cancellation of the lease with the current data center operators has a significant impact on data center supply and important facilities in Hong Kong, the Government may adopt an eclectic approach, such as charging penalties to industrial estate operators and even just requiring them to pay the land premium. This will not affect the current supply and will maintain a fair competition inside and outside the industrial estate. Although the Group has not been able to monopolize the data center supply in Tseung Kwan O in this case, it will help boost the operating costs of the industry and indirectly help the Group to be more competitive in the industry.

If "sub-leasing" is defined as the second one, the data center of Tseung Kwan O industrial estate is not necessarily considered to be illegal, but its service will be limited to some extent. For example, cabinet tenants cannot send staff to stay in the data center for server management. This will bring some advantages to the group, because they are not affected by the sub-leasing regulations. However, how to effectively implement the regulations in this situation will be a big problem. If there are loopholes in the implementation of the regulations, this will not bring obvious benefits to the group.

Effects on financial condition

In the announcement, the Group stated that the funding for the Tseung Kwan O project will be from internal resources and external resources (including unsecured loans borrowed from Sun Hung Kai Properties Group). However, as of June 30, 2018, the bank balances and deposits of the group were only 466 million. Therefore, we believe that the source of funds for this project will mainly come from borrowing and at least HK$5 billion in order to pay the land price.

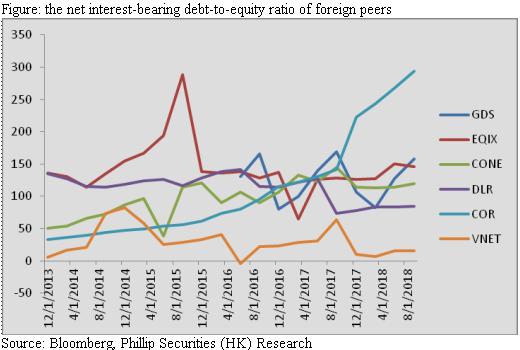

If the group borrows HK$5 billion, the net interest-bearing debt-to-equity ratio will rise sharply from 39% to 166%. Compared with foreign peers, we believe that the ratio for the Group has been quite high, but it is still within a reasonable level, because the data center business is relatively stable, and the debt level is generally high.

However, in addition to the land price, the group also needs to pay for the subsequent construction costs, so we expect the debt ratio of the group to rise further. In order to reduce the level of debt and interest payable, we believe that the dividend payout ratio will be significantly reduced in the future, so we have significantly reduced the projected dividend payout ratio from 95% to 50%.

Besides, since the interest expense will be capitalized during construction, we believe that interest expense should not affect the income statement so much before it is completed. At the same time, the Group's EBITDA in 2018 is as high as HK$870 million, so we believe the Group is able to cope with the huge interest expenses. However, if the interest cost of borrowings is floating, the interest expenses will rise further along with the rising interest rate.

To conclude, in the short term, although the debt level has risen sharply, we believe that its financial position is still stable, and it can handle interest expenses as long as the dividend payout is reduced. In the medium and long term, we believe that the return rate of Tseung Kwan O is not very attractive in itself. Therefore, the focus will be on whether the Group can win the judicial review and thus undermine the data center operators in the Tseung Kwan O industrial estate. If succeed, this will help improve the return on the Tseung Kwan O project.

Valuation

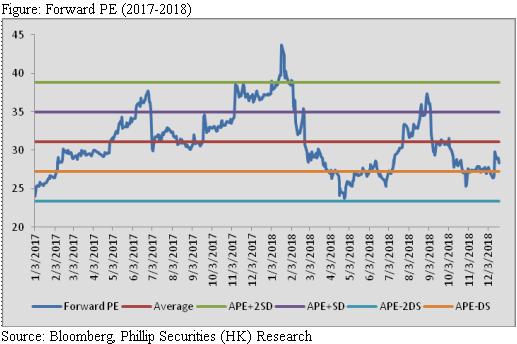

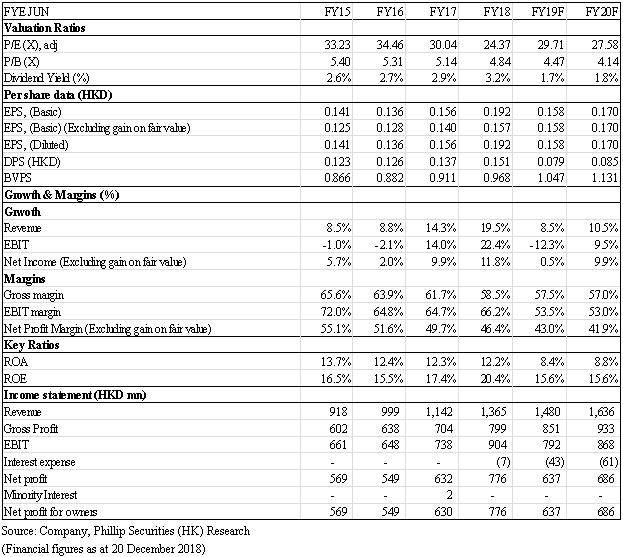

As the debt level has further increased, we have raised our forecast for interest expense for 2019/20. Besides, we believe that this expensive acquisition also reflects the confidence in the data center business from the group, so we also slightly increased the 2019/20F revenue growth rate from 7.5/10.4% to 8.5%/10.5%. Assuming 2019F P/E 36x, we give a target price of HK$5.67, down 0.9% then previous TP, due to the increasing interest expenses. With 21.15% potential upside, we upgrade to the rating to “Buy”.

Risk

1. Slower than expected demand on data center

2. Significant increase in land supply for data centers within a short period

3. The entry of cloud service giant players to data center industry in Hong Kong

4. Loss on judicial review

Financials

Click Here for PDF format...