Investment Summary

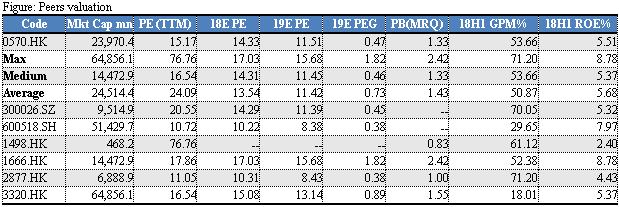

finished drugs is the only listed enterprise of Sinopharm Group focusing on TCM business. During FY15 to FY17, the company's operating income maintained a CAGR of 49.92%. The company has industry-leading growth and profitability. We give the target price-earnings ratio of 16 times in 2019, the expected earnings per share of 2019 is 0.36 RMB, the target price is HK$6.54, Buy rating. (Closing price at 21 Dec 2018)

Business Overview

The only listed enterprise of Sinopharm Group focusing on TCM business. In 1993, Rongshan International was listed on HK Exchange (code 570HK), engaged in the operation of fuel-fired power plants. In 2006, the listed company changed their main business from electric power to TCM manufacturing after selling out power plant business and purchasing Dezhong and Feng Liaoxing Pharma firms. In 2013, Sinopharm Group became a controlling shareholder through its Hong Kong entity, then the listed company was renamed "China TCM Co., Ltd." In 2015, it invested in Jiangyin Tianjiang Pharma and also became the controlling shareholder of Zhejiang Yifang (which was acquired by Tianjiang in 2008). So far, the company has earned 50% market share of concentrated TCM granules (CTCMG) in China. In 2018, the company introduced Ping An as a strategic investor.

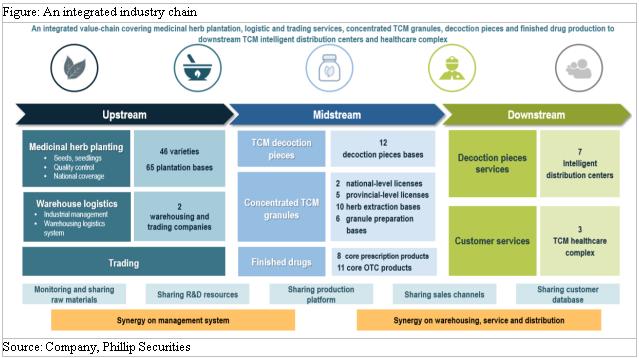

It forms an integrated TCM industry chain, covering herb planting, warehousing, logistics and technology R&D, and evolving the production of TCM decoction pieces, CTCMG and finished TCM drugs. For the downstream, it provides ready-to-use TCM decoction pieces services and healthcare services, for medical institutions, retail pharmacies and individual customers.

Centralized TCM decoction pieces business will maintain quick growth. The company is the market leader owning nearly half of the market share. Over the next four years, the industry scale is expected to maintain a CAGR of 40%. Growth momentum is mainly coming from favorable polices like keeping mark-ups, not accounting for drug sales in hospital, increasing consumer health awareness and consumption capacity. At present, national production and marketing license has not been opened. We believe that whether the market is open will be beneficial to the company. It now accelerates national distribution and expands its market share. We look forward to Matthew Effect in future, which means the strong will always be strong.

Productive capacity of TCMDP to ramp up, paving the way for future growth. TCM decoction pieces are main raw materials of finished drugs and CTCMG. It occupies 22% of market sales of TCM industry. In future, we expect that the industry will maintain relatively rapid growth, given the rising popularization of TCM healthcare, accelerated aging, rising public awareness. Through self-construction and acquisition, the company enlarges the production capacity of TCM decoction pieces, and actively builds intelligent distribution centers of TCM to enhance sales channel.

Finished drugs will develop steadily. The production and sale of finished drugs are the traditional business of the company, holding more than 500 pharmaceutical production approvals and over 60 exclusive drugs. In 2016, the company completed the acquisition of Huayi Pharma, and in 2018 it acquired 51% shares of Hubei Zhonglian Pharm, further enhancing product diversification. It proactively develops OTC channel and we expect steady development of this segment.

A National Complete TCM Industry China

China TCM is the only listed enterprise of Sinopharm Group focusing on TCM business. In 1993, Rongshan International was listed on HK Exchange (code 570HK), engaged in the operation of fuel-fired power plants. In 2006, the listed company changed their main business from electric power to TCM manufacturing after selling out power plant business and purchasing Dezhong and Feng Liaoxing Pharma firms. In 2009, the company acquired Guangdong Universal and Shandong Lukang, expanding the product line from traditional medicines to high-end drugs. In 2013, Sinopharm Group became a controlling shareholder through its Hong Kong entity, then the listed company was renamed "China TCM Co., Ltd." In 2015, it invested in Jiangyin Tianjiang Pharma and also became the controlling shareholder of Zhejiang Yifang (which was acquired by Tianjiang in 2008). So far, the company has earned 50% market share of concentrated TCM granules (CTCMG) in China. Through acquisition and self-construction, it continuously expands the production capacity of TCM granules and decoction pieces, and also purchases finished TCM drug companies, to further stretch its layout in TCM industry. In 2018, the company introduced Ping An as a strategic investor through issuing 602 million new shares and raised HK$2.67bn. Currently, Sinopharm HK, Ping An, CEO Wang Xiaochun and the public are holding 32%/12%/7.48%/48.46% shares respectively.

It forms an integrated TCM industry chain, covering herb planting, warehousing, logistics and technology R&D, and evolving the production of TCM decoction pieces, CTCMG and finished TCM drugs. For the downstream, it provides ready-to-use TCM decoction pieces services and healthcare services, for medical institutions, retail pharmacies and individual customers.

Building TCM herb planting bases. In recent years, the government has raised stricter requirements for the quality of TCMs. At present, 211 herbs have been purchased centrally, and the company is laying out the planting bases throughout the country for 136 main varieties. It has built planting bases in 14 provinces that with abundant resources of Chinese herbal medicines, including Anhui, Gansu, Sichuan, Shandong, Zhejiang, etc. Expanding the production capacity of raw materials in the upstream is conducive to ensuring the raw materials needed for the production of Chinese medicinal slices and CTCMG, controlling the cost and meeting the requirements of national supervision.

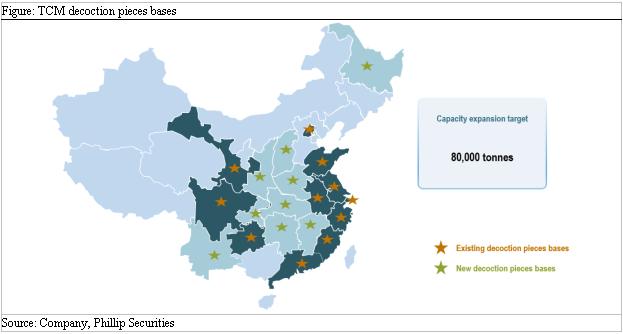

The collaborative production systems of two major business: CTCMG & TCM decoction pieces. CTCMG is now the biggest driving force for the company's growth. The company's strategy is to use CTCMG's hospital coverage to speed up the expansion of decoction pieces, so as to make the business of TCM decoction pieces a new driving force in the future. To this end, the company has established two production systems, Jiangyin Tianjiang and Guangdong Yifang. Factories are also built in the growing areas of genuine medicinal materials through self-construction or m&a. As of the first half of 2018, the company has 10 GMP bases for extracting TCM, covering 7 provinces such as Guangdong, Anhui and Jiangsu; 6 GMP bases for granules, covering 5 provinces such as Guangdong, Jiangsu, Gansu, Heilongjiang and Sichuan; 12 GMP bases for herbal pieces, covering 11 provinces such as Guangdong, Anhui, Jiangsu and Fujian. According to the company's development plan, the base plan of 23 provinces will be completed in 2019. It is estimated that the extraction capacity of TCM will reach about 80,000 tons, the production capacity of granules will be about 25,000 tons, and the production capacity of TCM pieces will be about 80,000 tons.

Utilizing regional medical resources to build “healthcare complex” to reach more end-users. The company currently operates three national medical centers in Chongqing, Guizhou and Foshan, and has five under construction. In 2017/18H1, the revenue of healthcare complex reached RMB58/25.mn (accounting for 0.5% of the total income), and the annual number of patients reached 37,000. The company tends to enhance business diversification through developing healthcare complex. Since that the construction is mostly through cooperation with local famous TCM brand, it can make use of local famous brands to expand the scope of business. Besides, through the operation of health care service institutions, the company's products and services can reach more end-users and therefore, improve brand awareness.

Establish a TCM logistics warehousing company to guarantee the supply of raw materials and build a transaction platform for TCM materials. The company has established two pharmaceutical warehousing and trading companies, and plans to build another four platforms in Gansu, Anhui, Sichuan and Guangxi with a covering area of 600,000 square meters as well as supporting constructions of quality inspection center and trading platform. These four platforms will be open to external needs. They will not only be used to store the medicinal materials and decoction pieces, but also provide inspection, storage and other services to other medicinal materials management organizations. The establishment of storage and trading platform is conductive to ensure raw materials for production needs, control costs, and facilitate the distribution, so as to expand hospital sales.

Leading CTCMG Player Expanding Nationwide

CTCMG are the development trend of modern Chinese medicine industry. CTCMG is made from single TCM decoction pieces by extraction. It guarantees all the characteristics of the TCM decoction pieces, has strong medicinal properties and high efficacy, and has many advantages such as direct flushing, safety and hygiene, convenient carrying and preservation, and is suitable for industrial production.

The industry of traditional Chinese medicinal granules will maintain a high growth rate. From 2006 to 2016, the national sales of traditional Chinese medicinal granules increased from Rmb228mn to RMB11.825bn, with a CAGR of 48.42%. In Japan and Taiwan, the sales of CTCMG account for most of the TCM sales, while in China, the proportion is only about 5%. Therefore, we estimate that with technological progress, policy improvement and market cultivation, the replacement of granules for pieces will continue to advance. According to Frost & Sullivan's forecast, the sales of CTCMG are expected to maintain a CAGR of 40% in the next four years, reaching about RMB44bn by 2020. Industry growth momentum mainly benefits from following aspects. (1) The state allows the retention of 15% mark-up for CTCMG, and not accounting for the proportion of hospital drug use. Due to the implementation of policies such as tightening medical insurance expenses, cancellation of drug mark-ups and centralized procurement bidding, the profit space of pharmaceutical manufacturers has been squeezed. CTCMG are allowed to retain a 25% mark-ups in hospital sales, which leaves considerable profit margin for enterprises. (2) The trend of consumption upgrading. Because the CTCMG have the advantages of exact curative effect and convenient use, patients have a high willingness to use them. Even in some areas without medical insurance coverage, sales have maintained a relatively rapid growth. With the increasing health awareness and consumption capacity of consumers, we expect that formula granular products will maintain a high growth rate in the future.

At present, the national production and marketing license of Chinese herbal CTCMG has not been opened. In 2003, the government has issued six national licenses to six enterprises (Guangdong Yifang Pharm, Jiangying Tianjiang Pharm, Shenzhen Sanjiu Pharm, Sichuan Neo-Green Pharm, and PuraPharm), and after that the state has suspended the issuance of national production licenses. The main obstacle to the opening of national license plates is that there is no uniform technical standard for CTCMG, which makes it difficult to manage the production, efficacy evaluation, sales and preservation. In recent years, the state has issued policies to promote the development of modern Chinese medicine industry, and improves related favorable policies. In 2015, the government issued a document (《中藥配方顆粒管理辦法(徵求意見稿)》), allowing enterprises to register with local regulatory authorities for the production and sale of CTCMG locally. At present, the state is actively formulating relevant technical standards, with 300 formula granule quality standards will be issued in the near future, and production and sales licenses will also gradually be opened.

The company is the market leader of CTCMG, accounting for nearly half of the market share. The company acquired Jiangying TianJiang in 2015 (Tianyin TianJiang acquired Guangdong Yifang in 2008). Therefore, now it has two national production licenses (Yifang and Tian Jiang), and production licenses in six provinces and municipalities. According to the disclosed sales of listed companies, in 2016, the company's sales of CTCMG accounted for 49% in market, making it undisputedly the leading enterprise.

Whether the new national license is released or not would be beneficial to the company. Before the release of new national license, enterprises registered in provinces and cities are allowed to produce and sell Chinese medicine CTCMG locally, while enterprises with national licenses could produce and sell CTCMG nationwide. So the existing six companies would continue to have relative advantages. After the opening of the market, CTCMG will be able to enter more medical institutions for sale, since that before opening up, they can only be sold in hospitals above level II. Hence, it is expected that after opening up, the market itself will increase considerably. Secondly, after the introduction of standards and the liberalization of the market, there will be a transition period of two to three years for the existing six producers. During this period, they can continue to produce according to their existing standards until gradually synchronized with the national standards.

China TCM actively participate in the formulation of national standards. In August 2016, the authority promulgated a draft, specifying the technical requirements for quality control and standardization of CTCMG (中藥配方顆粒質量控制與標準制定技術要求(徵求意見稿)》). China TCM has prepared standard decoction and carried out research on more than 170 varieties, and completed research and submitted to the the authority for evaluation of 123 varieties (68 by Guangdong Yifang, 55 by Jiangyin Tianjiang). The company and third party research institutes have tackled key technical problems such as fingerprint detection and content determination of CTCMG. Participation in the formulation of technical standards verifies the company's strong technical strength, the capacity to produce many products, and also leaves the late comers a certain cost to follow the existing standards.

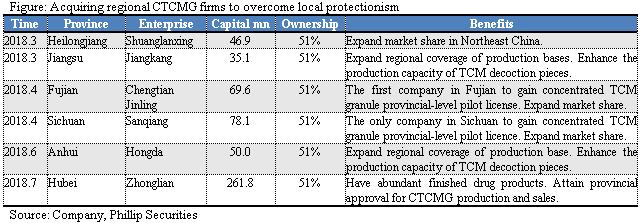

The company accelerates its national expansion. In the short and medium term, before the introduction of national standards and the opening of access policies, China TCM seizes the opportunity to expand its market share and cover more hospitals and retail pharmacies by laying intelligent dispensing machines in hospitals and building TCM industrial parks. At the same time, the company also actively improves capacity of producing TCM decoction pieces and CTCMG, strives to form scale advantage, ensuring raw material supply and meeting expansion demand. As for the protection barrier of regional governments, the company purchases the local enterprises with provincial and municipal pilot licenses, so as to enter more regional markets. So the company can combine its CTCM production approval, technical standards with high-quality resources of local enterprises to achieve Matthew effect, making the strong remain strong.

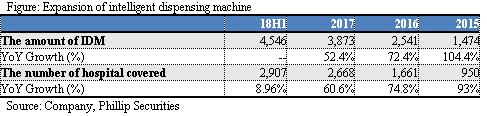

Intelligent dispensing machine quickly occupies the market. The company is able to expand large and medium-sized hospital customers with the intelligent dispensing machine systems that it developed. The dispensing machine is specially designed for its CTCMG, setting a high threshold for later competitors as well as a higher cost for the hospitals to replace suppliers, thus improving the stickiness of hospital customers. By laying dispensing machines to more hospitals to occupy the hospital sales pipeline, and by continuously improving the intelligent level of prescription granules in hospitals, the company can provide patients with better experience. At present, the company has already provided 4,546 dispensing machines to medical institutions, covering 2,907 hospitals. The proportion of sales through dispensing machines increased from 29.6% in 17H1 to 44.1% in 18H1.

Ping An Life becomes a strategic shareholder, to introduce advanced overseas experience. On March 19, 2018, the company signed a share subscription agreement with Ping An Life Insurance. Ping An subscribed for 604.3 million new shares at HK$4.43 per share, raising about HK$2.674bn. After the completion of the placement, Ping An has 12% of total shares, becoming the second largest shareholder. By introducing Ping An Group as a long-term strategic partner, China TCM will gain the advantages of Ping An in terms of technology, online platform and resources of customer base, sales pipeline. In addition, Ping An is the largest shareholder of Tsumura & Co, the leading company in Japanese Kampo Medicine (a CTCMG producer with the largest market share in Japan). In the future, China TCM will cooperate with Tsumura & Co in the fields of material planting, storage, R&D of classical prescriptions and sales of health products, introducing leading technologies, so as to achieve synergistic effects.

The production capacity of Chinese Herbal Pieces ramps up

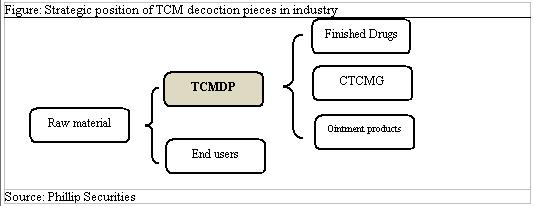

TCM decoction pieces are processed (such as cleansing, cutting, steaming, stir-frying, baking, shaking, etc.) according to TCM theory . Chinese herbal decoction pieces are the main raw materials of Chinese finished medicines and CTCMG. In 2016, the sales of TCM industry amounted to RMB870 bn, of which RMB190 bn (22%) were TCM decoction pieces (including CTCMG).

TCM decoction pieces will maintain a relatively rapid growth in the future. A research institute (前瞻產業研究院) predicts that the sales revenue of TCM decoction pieces industry will maintain a CAGR of about 15% in 2018-2023, and the sales scale is expected to exceed RMB50bn by 2023. On the supply side, compared with the common pressure of drug price, TCM decoction pieces enjoys a favorable price policy, as it is allowed to retain a 25% mark-ups in public medical institutions and not account for the proportion of hospital drug use, which promotes the enthusiasm of production enterprises. From the view of consumption side, due to the popularization of TCM, the acceleration of aging and the enhancement of residents` health awareness, the demand for TCM is increasing.

The production capacity of the company's slices has been improved to achieve the national layout. Through self-construction and m&a, the company has established TCM decoction bases in six provinces and municipalities, with a production capacity of nearly 40,000 tons (in construction capacity of 14680 tons). In the future, the company plans to continue to build or merge TCM decoction factories, targeting at a production capacity of 80,000 tons in 2019.

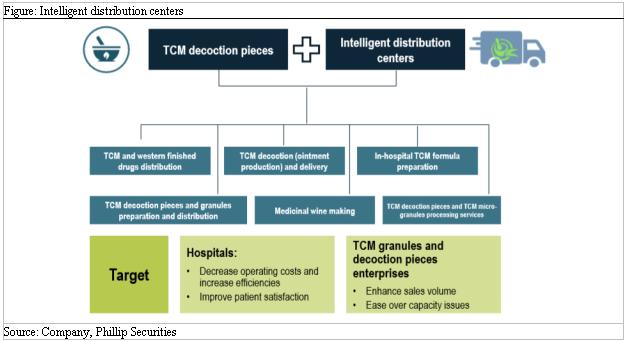

Intelligent distribution centers are built, focusing on small and medium-sized hospitals and retail pharmacies. The products and services provided by intelligent TCM distribution centers include: distribution of decoction pieces and CTCMG; TCM decoction (ointment production) and delivery; in-hospital TCM formula preparation; the distribution of finished drugs; the medicinal wine making service. Traditional supply mode can not meet the needs of small and medium-sized medical institutions, while the intelligent distribution center has differential competition with small and medium-sized suppliers to better meet the needs of clients. This mode has developed rapidly. As of the first half of 2018, seven distribution centers have come into service, including Guangdong Zhongshan Distribution Center and Hebei Shijiazhuang Distribution Center (that are newly put into operation this year). Besides, Foshan Center has signed cooperation agreements with 139 local community hospitals. The distribution center supplies decoction pieces to hospitals, and provides services such as frying and distribution of decoction pieces.

Finished drug business remains steady growth

Chines finished medicines are processed from materials like TCM herb. They have various dosage forms, such as capsules, granules, powders, pastes or pills. China TCM has many well-known finished drug brands with a long history, such as "Dezhong", "Fengliaoxing", "Tongjitang". It holds more than 500 drug production approvals, including more than 60 exclusive drugs. Eight exclusive products, such as Xianling Gubao Capsule, Yupingfeng Granule, Jingshu Granule, Runzao Zhiyang Capsule, Biyankang Tablet, Fengshigutong Capsule and Zaoren Anshen Capsule, have been included in National Essential Medicines Catalogue. The production and sale of finished drugs is the traditional business of the company. From 2006 to 2015, the company mainly engaged in the production and sale of Chinese finished drugs. Not until the acquisition of Tianjiang Pharm that its core business was changed to CTCMG. In 2016, the company completed the acquisition of Huayi Pharm. In 2018, the company acquired 51% of the shares of Hubei Zhonglian Pharm from the Sinopharm and injected capital, to continuously enrich its drug varieties.

Acquisition of Zhonglian Pharmaceutical Co,. Ltd. In July 2018, through equity transfer and capital increase, the company controlled 51% of the equity of China Union Pharmaceutical Co., Ltd. ("China Union Pharmaceutical") of the State Pharmaceutical Group. With a history of more than 400 years, Zhonglian Pharmaceutical Industry is an old name in the Chinese medicine industry, focusing on the production and sale of classical finished drugss, focusing on products involved in liver medication, respiratory medication, gynecological medication, cardiovascular and cerebrovascular medication and other characteristic areas. There are 348 registered medicines, 161 national medical insurance varieties, 70 varieties listed in the national basic medicine catalogue and 18 national exclusive varieties. The first one is Biejiajiajian pill, which is a TCM for pulmonary fibrosis in the medical insurance catalogue. It has a history of more than 2,000 years and is the classic prescription of Zhang Zhongjing in the Han Dynasty. The second one is Jinyebaidu Granule, which is the respiratory medicine in the medical insurance catalogue. After the merger and acquisition of Lianliang Pharmaceutical Industry, the product line of exclusive varieties of proprietary medicines will be increased. The company will reform the sales mode of finished drugss in China Union Pharmaceutical Industry, strengthen academic promotion and expand the market share of its products.

Financial Analysis

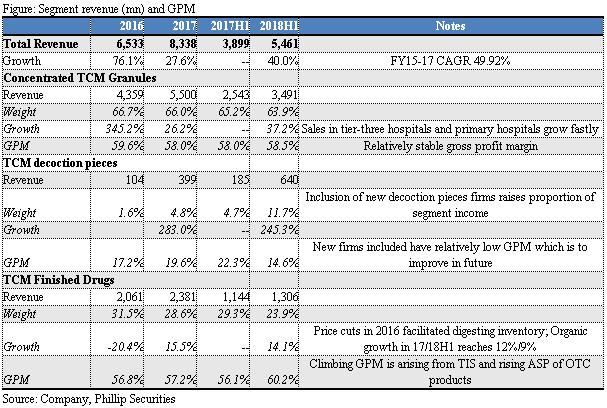

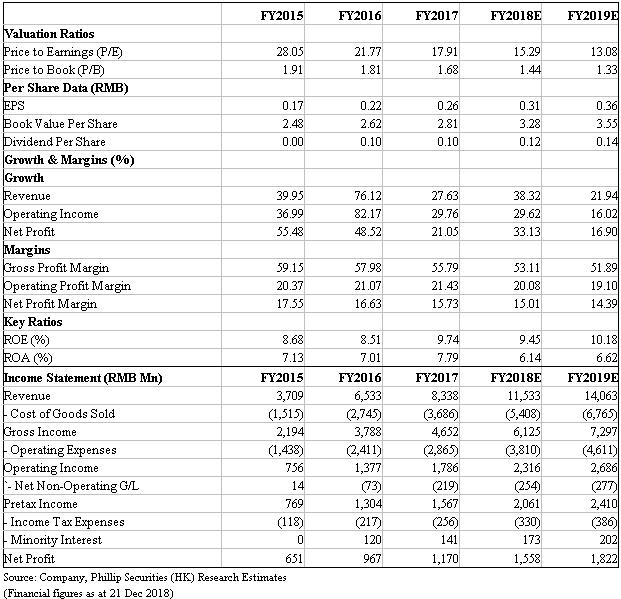

In FY15 to FY17, the company's business revenue maintained a CAGR of 49.92%, mainly due to the rapid growth of sales after the incorporation of TCM CTCMG business in 2015. (1) TCM CTCMG: From 2017 to 18H1, the sales of CTCMG maintained a rapid growth of 26.2%/37.2% respectively, and the gross interest rate was stable at about 58%. It is expected that they will benefit from the expansion of new hospitals and the sales volume of intelligent TCM industrial park in the future and maintain a relatively high growth rate. (2) TCM Decoction Pieces: Since the company merged and purchased Chinese Medicine Decoction Enterprises in2017, this sector has achieved a high growth rate of over 200% in 2017/18H1, accounting for 11.7% of revenue. It is expected that this proportion would continue to increase rapidly with the expansion of the production capacity of Chinese Medicine Decoction Pieces, and gross interest rate will rise steadily to normal level with the further integration of purchasing enterprises. (3) Finished drugss: In 2016, because of the unfavorable policies such as two-ticket system, second round bargaining, zero-markups, the company cut the price of finished drugss, promote inventory digest thus recorded a decline in revenue. In 2017/18, the business of proprietary medicine gradually recovered after adjustment (with the effect of TIS removed, the real growth rate was 12%/9%). At present, the proportion of the finished drugs business in the company's revenue is still about one-fourth. With the consolidation of Zhonglian, it is expected to be further enlarged. The business of finished drugs is predicted to maintain steady growth in the future.

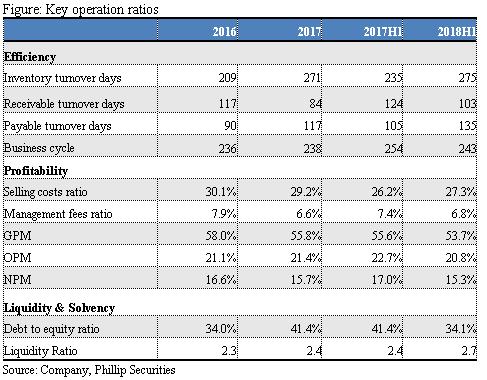

Key business indicators. Due to the low inventory base in 17H1, the inventory turnover in 18H1 increased, and is now at the same level as the overall level in 2017. The receivable turnover in days have been reduced under the accounting standards of Sinopharm; the receivable turnover days have increased by 30 days due to the increase of raw material consumption, and the ability of suspending payment to suppliers was enhanced. The overall business cycle decreased from 254 days in 17H1 to 243 days, showing that the business efficiency improved. Gross profit margin is generally stable and slightly declined, mainly due to the low gross profit margin of newly merged decoction pieces enterprises. Operating profit margin decreased by 1.9 percent, mainly due to the increase in sales costs (increased input in dispensing machines of CTCMG, consolidation of sales costs of new subsidiaries and high opening costs of patent medicine business affected by TIS). The net profit margin dropped by 1.7 ppts. It is estimated that the profit margin will rise after the newly-acquired enterprises run smoothly. Debt level is stable and liquidity is sufficient, because the previous placement enlarges capital, repays some debts, and prepares more cash for further external expansion.

Investment Thesis, Valuation & Risk

Our valuation model suggests a target price of HK$6.54. The company has notable growth and profitability in industry. We give a target PE ratio of 16x in 19E, predict earnings per share to be RMB0.36 for 19E, and derive a target price of HK$6.54, Buy rating. (Exchange Rate: 0.885 RMB/HKD.)

Risks include: Inefficiency in the integration after acquisitions; Less than expected sales growth; Fierce competition; Industry policy risks.

Financials

Click Here for PDF format...