Investment Summary

- Hengan has recently been attacked by short-selling organization, alleging the fabrication of the profitability of sanitary napkins business, bank deposits and interest income, and the non-disclosure of connected deals from real estate project. Although the allegations have been clarified by Hengan one by one, we expect that the negative impacts on the overall image of the company will be difficult to be digested by the market in the short term and the stock price will be under pressure. We believe that the stock price under pressure provides good opportunity to buy in, Hengan has also purchased back 7.08 million shares since December 17. We are optimistic about the long-term development of Hengan. It continues to promote Ameba reform, while promoting sales, improving operational efficiency and improving the expense rate.

Hengan is more profitable than its peers in sanitary napkin business. In our point of views, it is understandable. As the leader of China's sanitary napkin industry, its long-establish customer base and distribution channel network help to strengthen its bargaining power with suppliers on pricing and maintain a stable supply of raw materials from suppliers. In the first half of this year, the sanitary napkin business accounted for 31.8% of total revenue. Thanked for the increase in the proportion of high-end and upgraded products in the product mix during the period, offsetting the impact of rising petrochemical raw materials costs. Gross profit margin increased by 0.6 ppt to 69.3%. According to the information given by the management, the sanitary napkins increased by less than 5% in the third quarter, but still maintained a market share of 27% and maintained the leading position in the industry. The recovery trend in the fourth quarter has been accelerated. Considering the low base factor last year, we expect that this year end's performance will be better.

The management also maintains the guidance of overall sales revenue for the next three to five years with double-digit growth and same as its tissue business. Among them, the sanitary napkin business is expected to be difficult to achieve double-digit growth as the market is already saturated, so it will be repositioned as premium personal hygiene business. Hengan originally planned to launch new product categories such as cosmetics, cotton pads and facial care masks this year. As related R&D and registrations still need time, it is expected to be launched as soon as next year. We expect it will become a new growth driver of revenue.

- In the first half of this year, Hengan's overall revenue increased by 16.3% y.o.y., among which the tissue business grew by 21.1%, sanitary napkins 5%, and diapers 9.9%. The management said that due to factors such as the advance payment of 618 e-commerce consumption, the household paper business recorded only a single-digit growth in July to August, but the growth rate was better than that of competitors. It resumed to double-digit growth at the end of the third quarter and the fourth quarter.

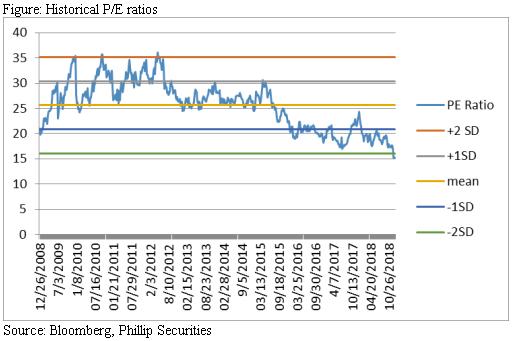

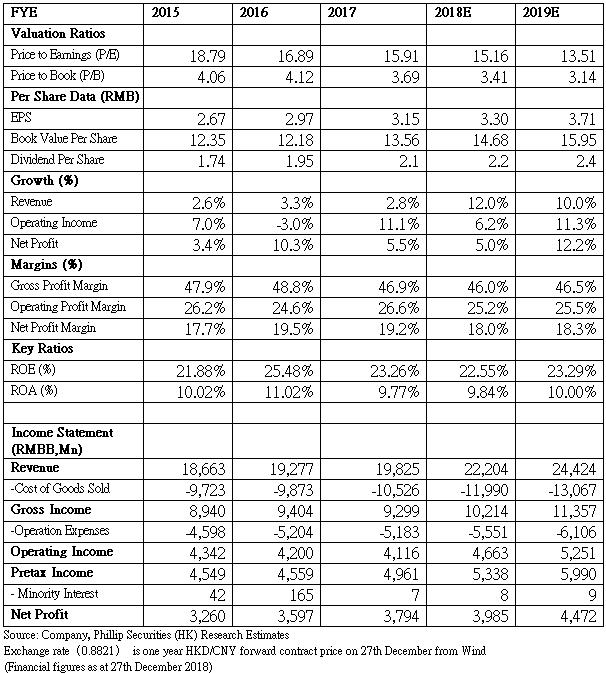

We believe that the overall revenue growth can reach double-digit target this year, and the growth is mainly driven by sales volume. Compared with its competitors` multiple price hikes, Hengan only raised price of 3 to 5% for rolled paper products in the first half of the year, which made some products cheaper than its competitors and help driving sales. Affected by the depreciation of RMB, the gross profit margin of tissue business is expected to be continued under pressure. We expect the EPS for the two fiscal years from 2018 to 2019 to be RMB 3.3 and 3.71, respectively, and the corresponding PE ratios are 15.16 and 13.51 times respectively. We give Buy rating, a forecast PE ratio of 18.4, and thus a target price of HKD77.5. (current price as of December 27, 2018)

Business Overview

Continuing pushing high-margin products, the market share of paper towels has increased

Tissue business is still the largest source of income for Hengan, accounting for about 50.2% of total revenue in the first half of the year. During the period, the business recorded a 21.1% increase, which was the main driver of overall revenue growth. It was mainly driven by sales volume. It was mainly benefited from Hengan's Amoeba model, traditional channels and modern channels significant improvement, e-commerce channel sales continuing growing, as well as market share.

During the period, the prices of paper pulp continued to rise y.o.y, dragging down the overall gross profit margin by 4.1 ppt to 39.6%. Hengan has continued to increase the proportion of high-margin products, and the revenue of wet tissue has maintained a rapid growth of more than 10%. Its strategy was successfully reflected in the increase in market share. The market share of tissue business reached 22% in the second half of the year, higher than last year's 19 to 20%, and it still the market leader.

During the period, the company increased brand promotion, resulting in promotion and distribution costs and administrative expenses increased by 7.1% compared with the same period of last year, but the proportion to revenue still fell by 1.4 ppt to 17.2%, which was mainly attributable to the implementation of “small sales team” operation model which effectively improved the sales efficiency.

According to the management team, there is investment in branding and special promotion such as for new products this year. For next year, investment will mainly focus on special advertising next year. We expect that if the income growth this year can reach double digits, the expenses to revenue ratio will be improved.

proportion of cooperation with distributors and direct sales will increase

The diaper business accounted for 8% of the overall revenue in the first half of the year. Traditional channel sales accounted for about 40% of the business revenue. In recent years, it has been following the market turning down sharply, with a y.o.y. decline of more than 30%. Although the proportion of e-commerce platform business has risen to over 30%, the overall revenue of the business still recorded a decline. During the period, the company narrowed the online and offline price gaps and increased the proportion of high-margin products, which helped to stabilize the gross profit margin at 39.9%, compared with 40.4% in the same period last year.

According to the management team, revenue of diaper business has still fallen since the third quarter, and it has not improved much comparing to the first half of the year. In terms of channels, traditional channels include small shops, revenue has dropped 40 to 50% (about 40 to 50% of the diaper business), while e-commerce channel has recorded a 20 to 30% increase (about 30%), and supermarket 10% increase (10%), and the maternal and child stores high single digit increase ( high single digit).

The management had previously proposed at the interim results meeting that distributors with poor performance would be eliminated and replaced by Amoeba's self-operated team, to directly expand the terminal market. However, it still needs time to judge distributors` business situation and make improvements. It is expected that the proportion of cooperation with distributors and direct sales will increase next year, and the top line will resume positive growth next year. The market share of diapers business is 4 to 5%, which is similar to last year and ranks first among domestic brands.

Continue to pay attention to suitable merger opportunities

In the first half of the year, Hengan announced the purchase of Finnpulp Oy. We expect this will strengthen the medium and long-term cost advantage and reduce the impact of pulp price volatility on gross profit margin. It is expected to supply 600,000 tons of long-fiber pulp to Hengan by 2021. It also actively explored the possibilities of sale of excess wood pulp in China and Southeast Asia as an additional source of income.

In addition, Hengan has also announced the acquisition of the entire issued share capital of Sunway Kordis, which is mainly engaged in manufacturing of food wrap film and plastic bags in the PRC. The sales are mainly export-oriented, which can help Hengan to diversified income sources and overall growth.

According to the management team, it has an open attitude towards suitable M&A projects in the future, with objectives including projects that can benefit existing product portfolios, as well as projects that can help develop new markets in China's neighboring countries such as Southeast Asia and India.

Investment Thesis, Valuation & Risk

Our valuation model suggests a target price of HK$77.5: We give Buy rating, a forecast price-earnings ratio of 18.4, and thus a target price of HKD77.5. The risks that need to be watched include top-line growth rate missing from expectation, wood pulp prices fluctuating sharply, industry competition increasing significantly, and Ameba units missing sales target. (current price as of December 27, 2018)

Financials

Click Here for PDF format...