Company Profile

Flat Glass is headquartered in Jiaxing City, Zhejiang Province. Its main products involve four fields, including PV glass, float glass, architectural glass and household glass, as well as the construction of solar power stations and quartzite mining, forming a relatively complete industrial chain. Among them, PV glass is the most important product of the company. The ratio of PV glass/household glass/architectural glass/float glass to the company's total revenue is about 7:1:1:1.

Flat Glass is the world's second largest PV glass manufacturer, and by the end of 2017, the company accounted for 20% of the global share. At present, the company has a PV glass production line with daily melting capacity of 4,000 tons and a float glass production line of 1,200 tons per day. The production bases of the company are located in Jiaxing City, Zhejiang Province, and Bengbu City, Anhui Province. In addition, the PV glass production base in Haiphong, Vietnam is also under construction. About 60% of the products are sold in the domestic market, and 40% are exported to countries such as Japan/South Korea/Malaysia/Vietnam/India. At present, the company has sufficient orders and the production and marketing rate is 100%.

Takeaways from Company visit

In the middle of last month, we joined an investigation tour organized by the company, and visited the company's new factory in Fengyang County, Bengbu City, Anhui Province.

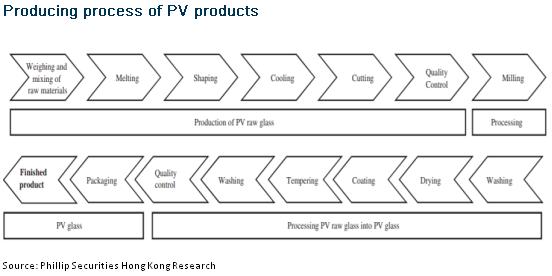

1. Product

The company's PV glass production process is mainly divided into two major stages, namely the original production stage and the post-processing stage (finished products). The procedure involved is as follows:

2. Factory

The new factory in Anhui Province covers an area of 650 mu (approximately 43.355 hectares) with a total investment of about RMB2 billion. The overall plan is to build three furnaces with a daily melting capacity of 1,000 tons and PV glass production lines. Among them, the first phase of the project, with the investment of RMB800-900 million, was put into operation at the end of 2017. The second phase was put into operation in June 2018, and the third phase is expected to be put into operation in the first half of 2019. Based on years of technical experience, the company's new factory in Anhui Province has adopted the most advanced PV glass production technology. The scale of the kilns is the largest at present, and the kilns possess unique multi-step structure and leading wide plate technology.

As a basic manufacturing industry, the scale effect of PV glass products is significant. The company's new production line has strong advantages in technology and scale. It is expected that the unit cost will be reduced by 20% compared with the company's Jiaxing factory after the formal commissioning.

At present, the total capacity of the company is about 4,000 tons per day, and it will reach 6,290 tons by the end of 2019 (after the third phase of Anhui factory and the new Vietnam factory being put into operation).

3. Takeaways from Investors conference

MGMT:Chairman Ruan Hongliang, Secretary of the Board of Directors Ruan Zeyun, Vice President Wei Zhiming, and Pan Rongguan, the person in charge of site operation of Anhui factory.

Q1: After the 531 New Policy, the capacity clearing of PV glass industry is still relatively slow. How can we realize the capacity clearing in the future?

A: Since there still existed the previous capacity, the industry's prosperity was under some pressure at the beginning of the 531 New Policy. In fact, from a global perspective, the global photovoltaic installed capacity this year is not much different from that in the last year. The 531 New Policy brings mainly psychological panic. 531 New Policy is mainly aimed at capacities of high energy consumption and low efficiency. The PV glass production capacity in China accounts for more than 90% of global production capacity. In 2017, China's photovoltaic installed capacity was 100GW, and the installed capacity in 2018 was almost 100GW. And even if the installed capacity in China is reduced, the amount in foreign countries (such as India) is increasing. If the industry's capacity drops, the market price of PV glass will rise. It is important to note that the demand for PV glass is also supported by the increasing proportion of applications of high-end products such as dual-glass photovoltaic modules.

Q2: As to the constitution of the company's product costs, can you split it up? Will the company negotiate with Sinopec when purchasing products?

A: Soda ash accounts for 30-40% of our direct material cost, while silica sand accounts for the rest. Fuel and electricity costs account for 30-40% of product costs. The price of raw materials will fluctuate with the market price. We will choose to sign some long-term orders by stages during the period when the price is relatively low, such as sodium carbonate. At the same time, new, reliable, stable and cheaper import channels are being developed.

Q3: What are the breakthroughs in the next generation of PV glass technology? What do you think?

A: We believe that the technological advances of next generation PV glass technology are mainly in high-power kilns, double-sided power generation and double-glass modules. Our R&D investment in these areas is also relatively large, and the Anhui factory has a capacity of 1,000 tons of PV glass. We are also the first domestic/fourth global manufacturer of coated glass certified by Swiss SPF.

Q4: How much will the production cost of 2.5mm be decreased compared with that of 3.2mm in double-sided PV glass? If the thickness is reduced by 20%, what are the differences between the unit price of the products and the unit gross profit cost? Will the unit price of domestic and foreign sales be different?

A: 2.5mm is a critical point parameter. As to PV glass below 2.5mm, the price will be higher as the thickness decreases, because this kind of PV glass is more difficult to produce. In marketing, the price difference between 2.5mm and 3.2mm is not very large. At present, the deep processing ability (such as coating) of making ultra-thin glass in the industry requires high support capacity, so the price naturally rises. The price for export is higher than that for domestic sales. Specifically, it depends on the quality requirements of customers. Many foreign customers have very high requirements for product quality, and the price is relatively high. We belong to the first echelon of the industry.

Q5: Xinyi PV Glass was established later than Flat Glass Group, why the company develops faster and has larger capacities?

A: In the second half of 2015, Xinyi PV Glass started to surpass us in production capacity. Before 2015, we had a larger scale. Since we were officially listed on the Hong Kong Stock Exchange in November 2015, we had a lot of pressure on financing before that time. There are ups and downs in the photovoltaic industry, and we are cautious about the expansion plan. As a result, we did not expand production capacity after 2013. Xinyi Glass, the parent company of Xinyi PV Glass, has been listed on the Hong Kong Stock Exchange in 2005. After that, Xinyi Solar was split and listed. The overall financing ability of Xinyi Glass is relatively strong. The company has expanded against the trend during the downturn of the industry and has invested and built many new capacities.

Q6: The unit cost of Anhui new production line is 20% lower than that of Jiaxing factory, mainly from what aspects?

A: Cost reduction mainly comes from: 1) The improvement of finished product rate. The finished product rate of Anhui new factory can reach about 80%, and that of Jiaxing factory is about 75%. 2) Unit energy consumption can be reduced by 30%. 3) Other costs in Anhui Province, such as labor costs, are also lower than those in Jiaxing.

Q7: What are the reasons for the price fluctuation of PV glass in the past few years?

A: The price of PV glass is closely related to the prosperity of the photovoltaic market. Now it is about RMB20-30 per square meter. Historically, the market price can reach up to RMB100 per square meter. But as costs fall, our costs are also reduced. The second phase of Anhui Project adopts the experience of the first phase, the production cost will continue to be decreased, but the decline will certainly be narrowed.

Our export ratio is relatively high, so the price will decline more smoothly. At present, the market price is relatively low, but the price lower than the cost of small businesses will not last long. We expect the price to pick up a bit, but it is unlikely to return to 30 or above.

Q8: What are the company's predictions for the global and Chinese PV glass market demand and price trends in 2019? What is the company's long-term positioning under the continuous optimization of competition pattern?

A: We expect that the photovoltaic installed capacity in 2018 will not differ greatly from that in 2017, and it will show a steady growth. After the 531 New Policy, the entire industry chain reflects that the price of the most terminal PV modules is very close to the market price without subsidies. Globally, though some countries have no government subsidies, the enthusiasm for PV installation is still relatively high. We expect that the output of the industry will increase gradually in the next few years, but the price will still fall. Future manufacturers will focus on improving performance and reducing production costs. The concentration of PV glass industry will be higher and higher, and the profits of the top five are currently more than 60% of the entire industry. Our products are in the leading position in technology/cost/scale, so we are confident to continue to take the lead.

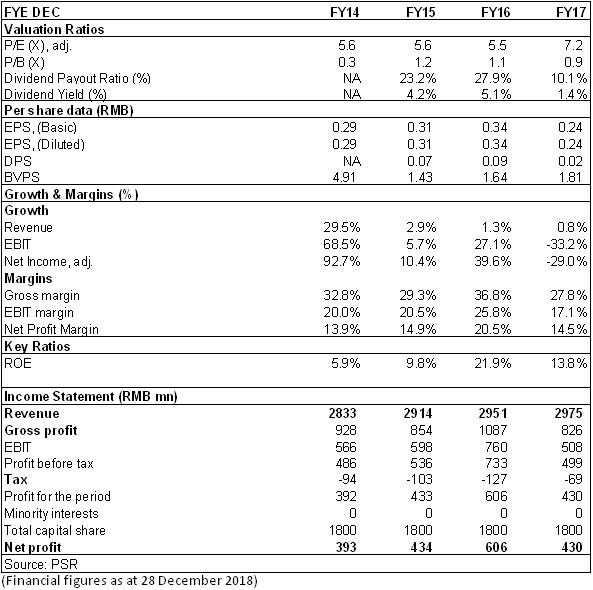

Financials

Click Here for PDF format...