|

|

|

*Advertisement* |

|

|

|

|

|

7 Jan, 2019 (Monday) |

TIANGONG INT`L(826)

Analysis:

Tiangong International (826) is principally engaged in the manufacture and sales of high alloy steel (including die steel and high speed steel), cutting tools and titanium alloy. The Group has issued a positive profit alert. The Group is expected to record a significant increase of around 40% to 60% in its consolidated net profit for the year ended 31 December 2018 as compared to the audited consolidated net profit for the corresponding period in 2017. In March 2018, the Group commenced the construction of the first domestic powder metallurgy production line in China to fill the gap in domestic production of powder metallurgy materials for die steel and high speed steel, as well as to explore the international market of new materials. (I do not hold the above stock)

Strategy:

Buy-in Price: $1.70, Target Price: $1.90, Cut Loss Price: $1.60

|

|

HK & CHINA GAS(003)

Analysis:

The businesses of the Group are the production, distribution and marketing of gas, water supply and emerging environmentally-friendly energy businesses in Hong Kong and mainland China. For the six months ended 30th June, the revenue of the Group was HKD 19.24 billion, up 24.7% YoY; the net profit attributable to shareholders was HKD 5.37 billion, up 7.7% YoY. For the first half of this year, the total volume of gas sales in Hong Kong was 16,158 million MJ, up 1.6% YoY; while the appliance sales revenue also increased by 5.2%. The growth is attributed to the moderate growth in the economy in Hong Kong, which enhance the demand on gas for the restaurant and hotel sectors. As at 30th June 2018, the number of customers was 1,890,415, and increased by 7,000 approximately since the end of 2017. As for the business in Mainland, the Group has a total of 132 city-gas projects in mainland (including the Towngas China). And, the total volume of gas sales was 11,470 million cubic meters, up 18% YoY, with customers reaching 26.47 million. Since the possibility of economic downturn increased, we believe it will be better to invest in the business that is not susceptible to business cycle. Besides, although the dividend yield of the company is only 2% based on the current price, it distributed one share for every ten shares. Thus, it will be a good investment from a long-term perspective.

Strategy:

Buy-in Price: $16.00, Target Price: $17.60, Cut Loss Price: $15.20

|

| |

|

Report Review of December 2018

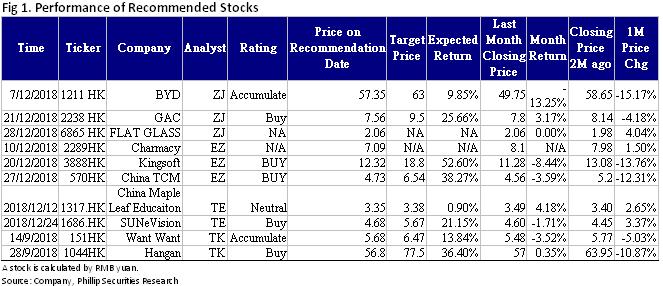

Sectors: Air, Automobiles (ZhangJing) Healthcare, TMT (Eurus Zhou) TMT, Education (Terry Li) Retail, Property (Tracy Ku) Automobile & Air (ZhangJing)This month I released 3 updated reports of BYD (1211 HK), GAC(425 HK)), and Flat Glass (6865 HK), which got success by their unique Competitive edge.The Q3 revenue of GAC was down about 3.3% Y-o-Y to RMB16.31 billion, net profit attributable to the parent company up by 6% Y-o-Y to RMB2.95 billion, equivalent to an EPS of RMB0.29. From the sales volumes of the first two months (October/November) in the Q4, sales volume of GAC Toyota improved, that of GAC Honda regained its momentum, that of GAC's independent brands continued to recover slightly, that of GAC FCA remained weak, and the sales growth of GAC Mitsubishi Motors slowed down, with their growth rates of 10.74%/65.8%/1.8%/-45.9%/-2%, respectively, sales volume increments of 14,723/46,074/1,558/-15,128/-462 vehicles, respectively. In terms of new cars, GAC Mitsubishi Motors will have its new model Eclipse Cross come out at the end of the year. In 2019, GAC Honda will put on the market Acura RDX, the new model of Vezel. GAC Toyota will have Levin PHEV, the new-generation RAV4. The Group's independent brand Trumpchi has new GS5, new GA6 and MPV GM6, as well as two 100% electric models based on an exclusive platform. It is expected that the Company will maintain steady growth in the future under the strong product cycle of the Japanese-brand JV. Healthcare & TMT (Eurus Zhou)This month I released 3 equity reports, including Charmacy (2289HK), Kingsoft (3888HK), and China TCM (570HK). We tend to highly recommend China TCM (570HK). The company forms an integrated TCM industry chain, covering herb planting, warehousing, logistics and technology R&D, and evolving the production of TCM decoction pieces, CTCMG and finished TCM drugs. Centralized TCM granules business will maintain quick growth. The company is the market leader owning nearly half of the market share. At present, national production and marketing license has not been opened. We believe that whether the market is open will be beneficial to the company. Productive capacity of TCMDP is to ramp up, paving the way for future growth. TCM decoction pieces are main raw materials of finished drugs and CTCMG. It occupies 22% of market sales of TCM industry. In future, we expect that the industry will maintain relatively rapid growth, given the rising popularization of TCM healthcare, accelerated aging, rising public awareness. Finished drugs will develop steadily. The production and sale of finished drugs are the traditional business of the company, holding more than 500 pharmaceutical production approvals and over 60 exclusive drugs. It proactively develops OTC channel and we expect steady development of this segment. TMT & Education (Terry Li)I released two reports on China Maple Leaf Education (1317.HK) and SUNeVision (1686.HK). We highly recommend SUNeVision. On December 12, the Group announced that it has successfully acquired a data center site in Tseung Kwan O for HK$5.46 billion. The land area is approximately 295,407 square feet. The upper and lower limits of the total gross floor area are 1,212,457 and 727,474 square feet respectively, implying at HK 4,503 per sq. ft. Although the acquisition price is higher than the market expectation, we tend to believe that this expensive acquisition is a strategic move of the Group. It is because On 10 Sep 2018, the group applied for a judicial review, accusing Hong Kong Science & Technology Parks Corporation (HKSTP) of allowing its tenants subletting to a third party in the industrial estates, and asking for the enforcement of the lease terms. Currently, there are nine data center operators in the industrial estate, including: China Mobile, NTT Communications, HKCOLO and Digital Realty Trust. If the loophole is closed due to the success in judicial review, the operators in TKO industrial estate may be either slapped with penalties or forced to cease the lease agreement. This means that if the government stops looking for land supply in Tseung Kwan O and Tseung Kwan O industrial estate cease the lease with data center operators, the Group will monopolize the data center supply in Tseung Kwan O and become the only data center in the region that can sublet. However, it is believed that the debt ratio will rise substantially, but we think it is still acceptable as the business nature of data center is relatively stable. Retail, Property (Tracy Ku)This month I released the first coverage report of Want Want China(151) and Hengan(1044). Hengan has recently been attacked by short-selling organization, alleging the fabrication of the profitability of sanitary napkins business, bank deposits and interest income, and the non-disclosure of connected deals from real estate project. Although the allegations have been clarified by Hengan one by one, we expect that the negative impacts on the overall image of the company will be difficult to be digested by the market in the short term and the stock price will be under pressure,which provides good opportunity to buy in. In the first half of this year, the sanitary napkin business accounted for 31.8% of total revenue. According to the information given by the management, the sanitary napkins increased by less than 5% in the third quarter, but still maintained a market share of 27% and maintained the leading position in the industry. The recovery trend in the fourth quarter has been accelerated. Considering the low base factor last year, we expect that this year end's performance will be better. The management also maintains the guidance of overall sales revenue for the next three to five years with double-digit growth and same as its tissue business. Among them, the sanitary napkin business is expected to be difficult to achieve double-digit growth as the market is already saturated, so it will be repositioned as premium personal hygiene business. Hengan originally planned to launch new product categories such as cosmetics, cotton pads and facial care masks this year. As related R&D and registrations still need time, it is expected to be launched as soon as next year. We expect it will become a new growth driver of revenue.

Click Here for PDF format...

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the “Group”) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products’ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

版權所有, 翻印必究。

Copyright(C) 2019 Phillip Securities (HK) Ltd. All Rights Reserved.

|