Investment Summary

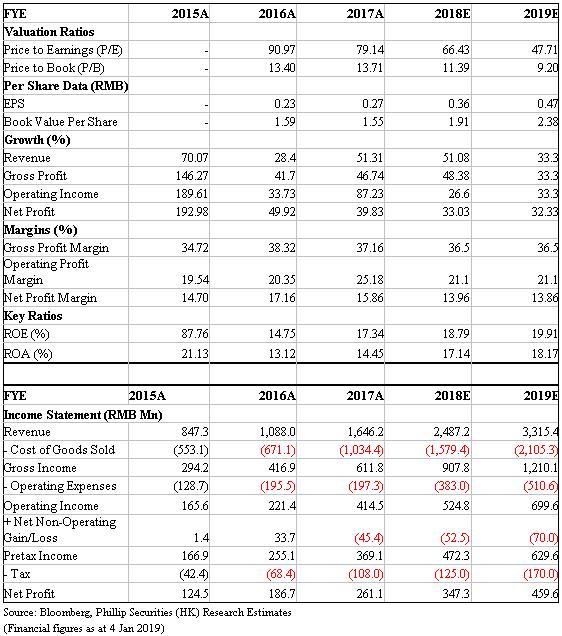

Yihai is a leading and fast-growing compound condiment manufacturer in PRC, the only supplier of hot pot soup flavoring products for Haidilao (6862HK). In 181H, the company achieved rapid growth, with revenue increasing by 59.1% yoy and net profit increasing by 170.4% yoy. We know from our checks that 18Q4 sales performed well and channel inventory is ideal. We expect 18E/19 revenue to be RMB2.487bn/3.315bn, and increase the target price to HK$18.91. The 1-y exchange rate is assumed to be 0.87 RMB/HKD. (Closing price at 4th Jan 2019)

Business Overview

18H2 results to be expected. In 18H1, the company delivered revenue of RMB1,004mn, an notable increase of 59.1% yoy, and net profit of RMB189.8mn, an increase of 170.4% over the previous year. We know from our checks that 18Q4 sales performed well, mainly arising from the expansion of Haidilao restaurants and the good performance of e-commerce in 18H2.

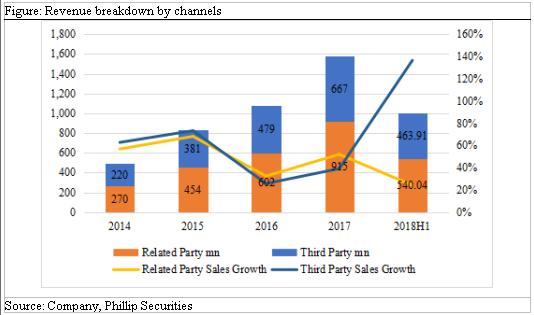

Related party sales. Haidilao Group is the largest Chinese catering brand in China. Haidilao Group has steadily increased the stores revenue, and has made sustained expansion in the number of stores. In 2018, the number of newly-opended stores was about 180 (the original guidance: 180~220), which is at the low level of the original guideline. The company's sales revenue to related parties was RMB540mn, an increase of 24.2% yoy. The company said that Haidilao will continue to expand in the future and actively expands overseas markets, but the specific expansion plan is not yet clear. According to Frost & Sullivan, the domestic hot pot restaurant market revenue in 2017 is RMB436.2bn. It is estimated that the compound growth rate will reach 10.2% and the scale will reach RMB707.7bn by 2022. And overseas Chinese catering market will grow at 8.3% in the next five years.

Distributor networks are sinking further. In 18H1, distributors covered 31 provincial areas in China, Hong Kong, Macao and Taiwan, and 24 overseas countries and regions. Sales to distributors in 18H1 amounted to RMB363.2mn, an increase of 117.2% yoy. In 18H2, the company further increase the penetration of sales channels, entering 320 prefecture-level cities. The distributor's pipeline inventory is healthy and inventory turnover days keep at about one month.

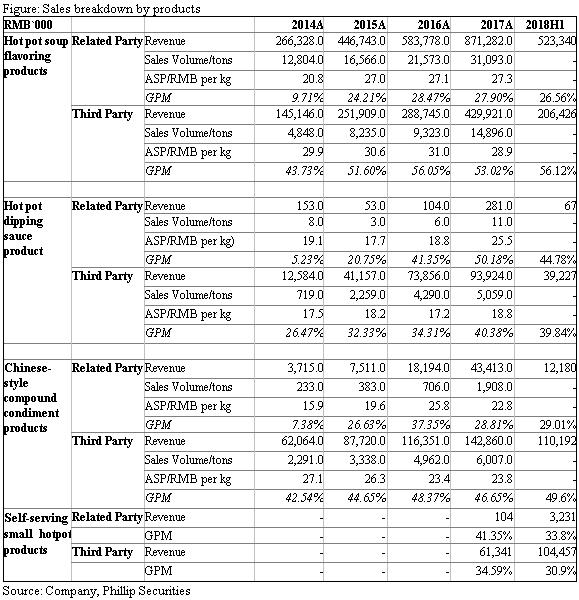

E-commerce channel. In 18H1, e-commerce revenue reached RMB80.2mn, rising by 372.4% yoy. The company launched a number of new products on e-commerce platforms. It set up warehouses in East China to accelerate delivery efficiency for consumers in East China in 18H1, and opened warehouses in South China in 18H2 to further enhance delivery efficiency in Guangdong, Fujian, Guangxi, Yunnan and Hainan. At present, the company has five flagship stores in online platforms involving Tianmao, Jingdong and other e-commerce platforms. In 18H2, the segment revenue was facilitated by e-commerce promotion festivals. Sales on Tianmao and JD accounted for half of the e-commerce revenue.

Third-party catering business has been significantly boosted. In 18H1, third-party catering business sales reached RMB20mn, rising by 70.8% yoy, attributable to promotional activities and the expansion of product mix. As the standardization of catering production process is a future trend, Yihai's third-party catering business is expected to continue growing. In addition, the company explores regional and sub-division products, and launches three new flavours of crawfishcondiments, one rice blending sauce and three types of self-serving small hot pot products. The introduction of new products can alleviate seasonal problems of hot pot products, further promote consumption, and also improve brand awareness. The company will also introduce self-serving rice and other new products to drive sales growth.

Expanding production capacity. The newly established factory located in Maanshan of Anhui Province formally commenced operation in 18H1. The first phase of Bazhou project (with an investment of RMB300mn) was completed and put into operation in 18H2, and the second phase project will be completed and put into use in 2020E. In the future, the company still has plans to continue to increase production capacity, and upgrade warehousing equipment. Capital expenditure will remain around RMB350mn in 2018E/19E.

Valuation & Risks

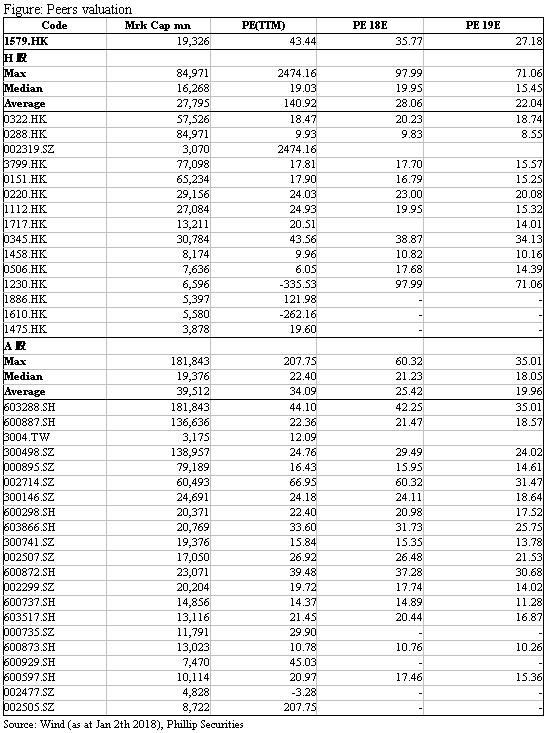

We give target price of HKD18.91. Sales will benefit from Haidilao's continued growth as well as the acceleration of overseas expansion. However, it should also be noted that the number of new stores opened in 2018 is at the low level of the guideline range, and the future expansion plan is not yet clear. We expect 18E/19 revenue to be RMB2.487bn/3.315bn, and increase the target price to HK$18.91. The 1-y exchange rate is assumed to be 0.87 RMB/HKD.

Risks include: Rising COGS; Fierce competition; Haidilao expansion fails expectations; Food safety problem.

Financials

Click Here for PDF format...