Investment Summary

ChinaSoft International is one of the leading software and information services companies in China. Owing to the slowdown of emerging business and the presence of uncertainties in domestic economy, we revise down our revenue growth estimate. Based on 2018 net profit, we assume a P/E ratio of 16.5x (average over the past two years), deriving a target price of HK$5.37. 2.9% lower than previous target price, we reiterate a “Buy” rating with a potential return of approximately 46.3%.(Closing price at 8 Jan 2019)

Business update

The growth of Jointforce and hardware slowed down

Because of the economic fluctuation in China, the provincial governments were prudent to their spending, making the revenue growth of Cloud Software Park and Honeycomb that mainly serve the provincial governments slowed down. As for Cloud Software Park, the Group will reach an agreement with the provincial governments for building a localized website for their High-Tech Industrial Development Zone. And, it will assign staffs for sales and operating, so that it can enhance the informatization of the local enterprises, e.g. how to sign up for Jointforce, how to become a vendor and how to find a cheap IT vendor. The agreement generally lasts for three to five years, where the Group will receive operating fees every year from the provincial governments. As for Honeycomb, it is a smart manufacturing platform for small and medium-sized manufacturers, which provides diagnostic services to them, and the government subsidizes them. Thus, since the financial condition of provincial government is not so solid, it lower their demand for those two services.

Besides, the growth of member in Jointforce was lower than expected, only 40% YoY, because the force of the Group this year was on the services of Cloud Software Park, Cloud Integrative Service and Honeycomb.

Apart from Joinforce, the sales of hardware for transportation (i.e. Airport and Subway) were also lower than expected.

Solution and outsourcing business generally met expectation, while the ban on Huawei's 5G equipment has no effect on the Group so far

As the uncertainty on the economy goes up, the enterprises tend to cut costs, which in turn increase the demand of outsourcing, because it helps the enterprises to lower the operating cost of their non-core department. Therefore, we believe the outsourcing business will not be heavily affected even in an economic downturn.

Recently, there was news claiming that Huawei's 5G equipment 5G have been banned by several countries. Since a significant proportion of outsourcing business for the Group is from Huawei, the market worries the incident will adversely affect the Group's outsourcing business. However, the Group does not see any significant effect so far, and expect the growth of the business from Huawei in 2019 will be higher than that in 2018, above 10%. The recent recruitment was mainly for the business from Huawei, which added several thousand staffs to around 62,000. Even if Huawei's 5G equipment is really blocked, because the Group provides outsourcing services for Huawei's multiple businesses, such as mobile phones and cloud services, as long as Huawei does not reduce the overall investment in research, the impact of the Group's outsourcing demand from Huawei will not be too great.

Besides, the Group remains the estimate for the revenue growth from other clients, where we should see a 50% of revenue growth in 2018 from HSBC, reaching RMB 900 million. As the base has been increased, the growth rate may be as high as before, but it will remain on a relatively high level.

Share award scheme

On 10 December 2018, the Group announced to adopt the share award scheme. The scheme is to recognize the contributions by certain Employees by rewarding them company shares in order to retain them for continual operation and development of the Group, and to attract suitable personnel for further development of the Group. The Scheme shall last ten years, and the costs will be incurred when the reward. The number of shares will not be diluted, because the shares that reward the employees are bought from the market directly. As of 8 Jan 2019, the Group has repurchased eight times, accounting for 1.46% of total number of Shares issued.

Growth forecast

Due to the emerging uncertainties in domestic economy, the SMEs are going to bear the brunt, or even close down, leading to a less demand for emerging business. Thus, we lower the revenue growth estimate in 2018/19F from 80%/85% to 60%/65%. We believe the impact from economy on tradition business is relatively slow, so we slightly lower the revenue growth estimate in 2018/19F from 15%/14% to 11%/10%. Besides, since the proportion of emerging business dropped after the change in growth estimate, we reduce the GPM estimate in 2018/19F from 31%/31.5% to 30.7%/31.4%.

Valuation

Owing to the slowdown of emerging business and the presence of uncertainties in domestic economy, based on 2018 net profit, we assume a P/E ratio of 16.5x (average over the past two years), deriving a target price of HK$5.37. 2.9% lower than previous target price, we reiterate a “Buy” rating with a potential return of approximately 46.3%. (HKD/CNY=0.8765)

Risk

1. Slower-than-expected growth in SaaS market

2. Suddenly loss on major customers

3. New products replace the company's existing products

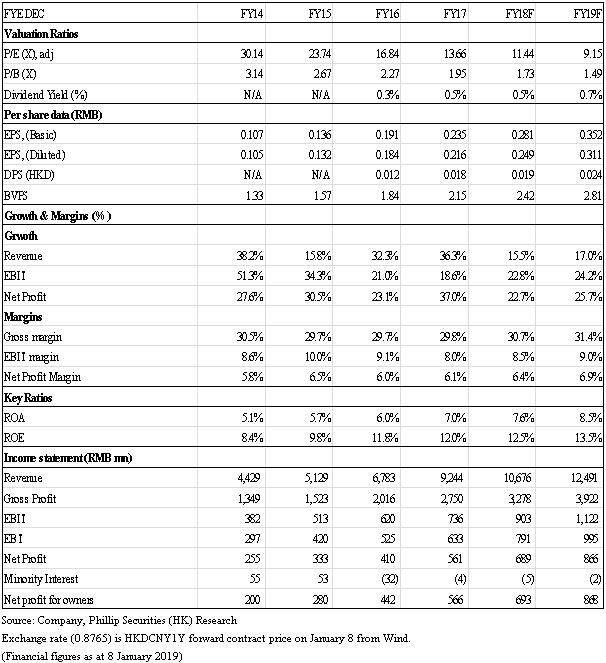

Financials

Click Here for PDF format...