Investment Summary

Net Profit in the First Three Quarters Hits a New High, Growth Rate Slows Down under a High Base

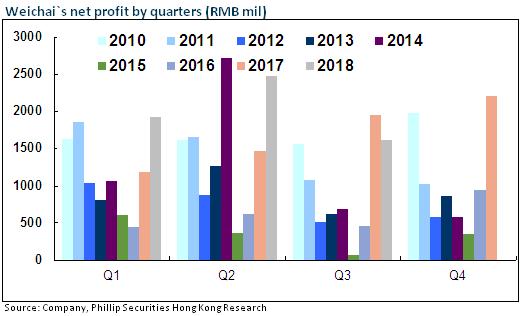

The Q3 revenue of Weichai Power in 2018 was down about 8.5% yoy to RMB35.92 billion, net profit attributable to the parent company down by 17.6% yoy to RMB1.91 billion, and the EPS stood at RMB0.2. The yoy decrease in Q3 was mainly due to the high base caused by the high prosperity of the heavy truck industry in the same period of the previous years, while the growth rate of the heavy truck industry slowed down significantly during the period.

In the first three quarters, the Company reported a revenue of RMB118.18 billion, up by 5.94% yoy, and a net profit attributable to the parent company of RMB6,001 million, up by 30.4% yoy, and the EPS stood at RMB0.75. Net profit of the Company in the first three quarters hit a record high since its listing.

Gross Margin Basically Stays Flat and Expenses Are Well Controlled

The Company's integrated gross margin in the first three quarters was 21.65%, basically staying flat and down by 0.04 ppts slightly, and the rise in the price of raw materials and the shift in product mix basically offset each other. The expenses of the Company were well controlled, the three rates were 12.92%, down approximately by 0.8 ppts over the same period last year, among which the sales expense rate was 6.7%, down by 0.32 ppts yoy, the administration expenses + R&D expenses rate were 6.17% (-0.05ppts yoy), and the financial expenses rate was 0.08% (-0.46ppts yoy).

The Company Has Stable Advantage in Heavy Truck Industry Chain. Non-engine Business Gradually Takes off

During the period, the Company's heavy-duty engine has been in a stronger position in heavy truck market, five-ton loader market and the market of passenger vehicles above 11 meters. In the first three quarters in 2018, the market share of the Company's heavy truck engine reached 30.2%, maintaining its leading position. We expect that the future heavy truck engine business of the Company will continue to benefit from the upward trend in the sales structure resulting from upgrading consumption in heavy truck industry.

Based on golden industry chains of heavy truck (engine + gearbox + axle + complete heavy truck), Weichai Power has steadily expanded its business scope since 2012, and laid out an industry chain featuring intelligent logistics solution through the acquisition of Baudouin, Linde Hydraulics, Kion and Dematic. In H1 of 2018, the sales revenue of Linde Hydraulics (China) doubled yoy, and the revenue of Kion in the Q3 stood at EUR1.9 billion (+3.5% yoy), the amount of order was EUR2.06 billion (+11.5%yoy) and net profit was EUR100 million (+21.8%yoy).

In addition, the proportion of the Company's non-road heavy truck engine has also been increased to about 30%, which is complementary and synergistic with the original business. The Company's "power + hydraulic" strategic framework is clear, which helps smooth the original business affected by periodic fluctuations of heavy truck industry, and the business structure is more balanced.

The Company Increases Input in New Energy Sector

After 2017, the Company has been keeping exploration in the field of new energy strategy and invested Ballard Power Systems in Canada, Foresight, Ceres Power in Britain, PSI in the US, and the Company also increased input in R&D to enter the new energy field of fuel cells. At present, the Company has taken control of high-quality resources, such as hydrogen fuel cells and solid oxide fuel cells in new energy business. In future, the Company will strengthen R&D in core technology and accelerate the implementation of new energy business.

Investment Thesis

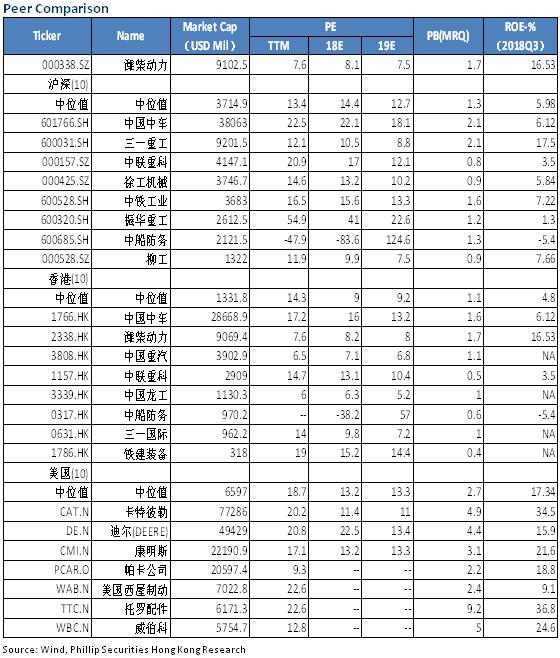

We believe that although the high prosperity of heavy truck industry is unlikely to continue, factors such as stricter environmental protection policies, upgrading of emission standard, overload control and rapid development of e-commerce logistics will support the stable sales of heavy truck in China. The chairman of the Company also serves as the chairman of Sinotruk, and it is expected that Sinotruk will increase engine purchasing volume of the company in the future. We reaffirm the "Accumulate" rating with the target price to HKD 10.65, equivalent to 9.9/9.8x P/E ratio in2018/2019. (Closing price as at 10 January 2019)

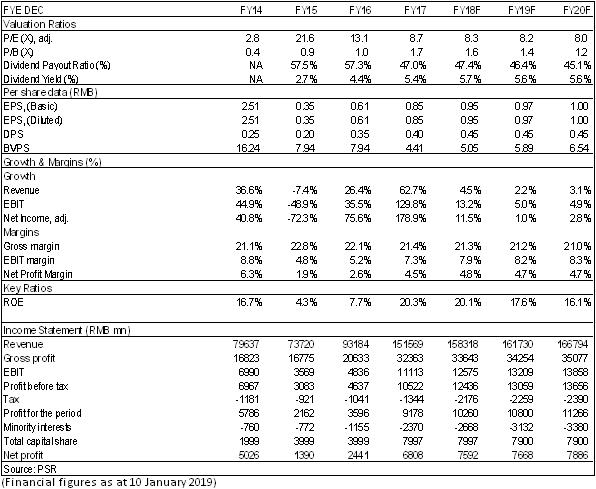

Financials

Click Here for PDF format...