Investment Summary

On 23rd December, China Shengmu Organic Milk (1432) announced to sell to Inner Mongolia Mengniu 26.67% interest in the Target Company, and Shengmu High-tech agreed to sell to Inner Mongolia Mengniu 24.33% interest in the Target Company. Upon the completion of the share purchase agreement, Inner Mongolia Mengniu will hold 51% interest in the Target Company, and is expected to be recognized as a subsidiary of Inner Mongolia Mengniu in its consolidated financial statements.

The consideration of the sale and purchase of the sale shares under the share purchase agreement is RMB 303,419,400. Among which RMB273,419,400 will be paid with five business days after the date of the payment confirmation certificate and the remaining RMB30,000,000 will be paid within five business days from the first anniversary date of the payment confirmation certificate.

Shengmu is the largest organic dairy company in China with the largest herd of organic dairy cows nationwide. It is the only vertically integrated organic dairy company in China that meets E.U. organic standards. It is the only dairy company in China that offers branded organic dairy products that are 100% processed from raw milk produced by self-owned certified organic dairy farms.

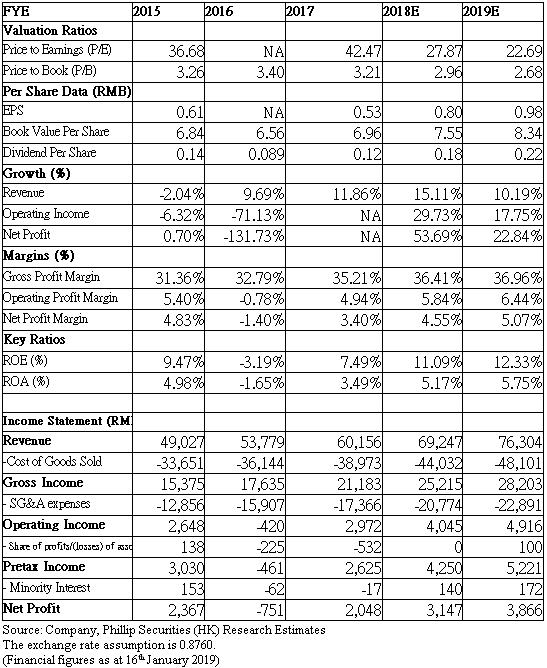

The target company recorded losses before taxation of RMB68.44 million and RMB1194.92million respectively in 2016 and 2017, and losses after taxation of RMB76.99million and RMB1185.44million. Shengmu has announced profit warning expecting to record a loss for the year ending 31 December 2018. Because of the impairment provisions made for trade receivables and other receivables, its total profit for the year ending 31 December 2018 is expected to be decreased by approximately RMB1.06billion.However, if we only look at the liquid milk product business, the revenue in 1H of last year was RMB480 million, which accounted for only 1.4% of Mengniu's revenue in the same period.

The principal businesses of Mengniu are liquid milk, ice cream, milk formula and other products. Liquid milk business accounted for 83.9% of total revenue in 1H of 2018. UHT milk business accounted for 47.4% of the revenue of the liquid milk segment. Revenue of UHT milk during the period grew 16.3% which was driven by a variety of mid- to high-end products that emphasize high-quality milk sources, including organic Milk Deluxe, Future Star which was made will premium milk in limited supply from selected ranches, Greenhouse fresh milk, and Xianyu Pure Milk with China Modern Dairy.

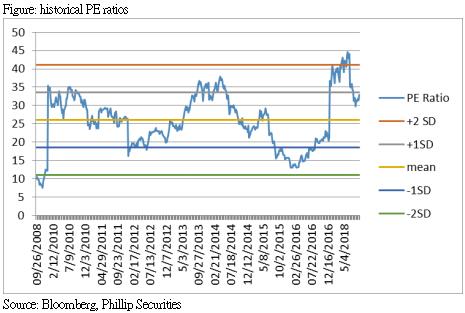

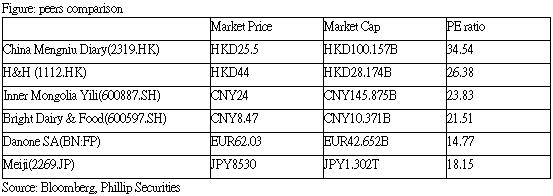

We believe that the acquisition may bring slight pressure on Mengniu's short-term performance. In the medium and long term, it will not only provide Mengniu with a stable supply of raw milk, especially the organic raw milk supply, it will also enrich Mengniu's product categories in the end market, that can provide growth drivers for revenue.We believe that the dairy industry in China is with rigid demand and the impact from economic slowdown is limited. The double-digit growth target for the whole year is still able to meet. We believe that the recovery of raw milk prices in 2H will help its material associate China Modern Dairy (1117) to further reduce its loss. Sales and distribution expenses are expected to be lower than 1H. We maintain a forecast PE of 31 times and target price of HKD28.5. (current price as of 16th January, 2019)

Business/Industry Overview

Mengniu's interim revenue increased 17% y.o.y. to RMB34.474 billion, of which 7% came from sales volume growth, and more (10%) came from the increase in ASP, driven by the improvement in product portfolio, and decrease in discount rate. Gross profit margin(GPM) increased 3.6ppt y.o.y to 39.2%.

In terms of GPM, the stable raw milk procurement cost coupled with the higher growth rate of the high-margin Deluxe, room-temperature yogurt and milk powder, led to the increase in overall GPM. The management stated that the high GPM in 1H of the year was sustainable and that it could be maintained throughout the year and next year. The raw milk price in 2H is expected to be higher than 1H due to seasonal reasons, but it is believed that it will be at reasonable and controllable level. The annual raw milk price is expected to be flat y.o.y.

Valuation and risk

We are optimistic about the industry and the company's prospects, thus maintain forecast PE ratio of 31 times and target price of HKD28.5. Potential risks include failure to meet revenue growth, lower profit margins than expected, and huge fluctuations in raw milk prices. (current price as of 16th January 2019)

Financials

Click Here for PDF format...