Investment Summary

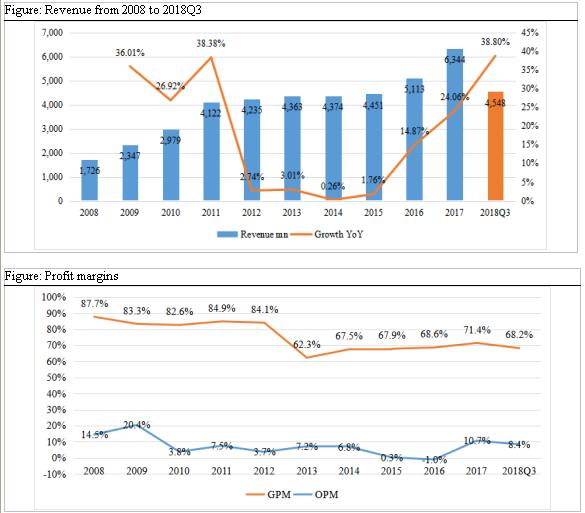

Yongyou is a leading provider of enterprise services in China, offering cloud, software and financial services. During FY15 to FY17, its revenue achieved a CAGR of 19.4%. Among the first three quarters of 2018, Yongyou achieved yoy revenue increase of 38.8%. With the development of new businesses and improved product and service mix, its income is expected to maintain rapid growth in future. We initiate target price of RMB27.8, Accumulate rating. (Closing price at 18 Jan 2019)

Business Overview

Founded in 1988, Yongyou initially focused on the development and sales of financial software. In 1991, it became the largest financial software company in China. In 1998, the company transformed focus from financial software to management software, released the first enterprise resource planning (ERP) software U8, and then developed high-end management software NC series catering to large corporate clients. In 2001, Youyou was listed on Shanghai Exchange, raising RMB8.8bn. In 2002, the company occupied the biggest market share in domestic ERP market. After the financial crisis in 2008, benefiting from favorable industrial policies, the enterprise resource planning software industry developed rapidly during 2009 to 2011. In 2012, European debt crisis triggered a wave of layoffs in multinational companies and China's economy growth slowed down. Thus the company's revenue growth fell into a stagnation period. Beginning from 2013, the company started exploring new areas such as mobile payments and cloud. In 2016, the management set three businesses of “software, cloud services, and finance” as core momentum. On the company's 30th anniversary, its 18H1 revenue increased by 38.8%, representing the beginning of a new development era.

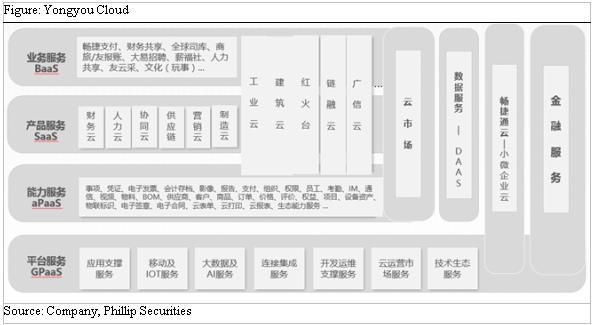

Cloud Business

Favorable policy environment. In Aug 2018, Chinese Ministry of Industry and Information Technology issued a notice (推動企業上雲實施指南(2018-2020年)), stating that by 2020, the widespread adoption of cloud computing in production, operation and management of enterprises should be realized. There should be one million new enterprises adopting cloud service, and more than 100 typical benchmark applications should be completed.

China's public cloud market will grow at a high speed. According to data from CAICT, the size of China's public cloud market reached RMB26.48bn in 2017, an increase of 55.7% yoy. The demand of Internet enterprises has maintained rapid growth, and the promotion of cloud application in traditional enterprises has accelerated, which has driven the rapid expansion of the public cloud market. During 2018 to 2021, China's public cloud market will maintain a high growth rate, and by 2021, the market size will reach RMB90.26bn with the industry CAGR of 35.88%.

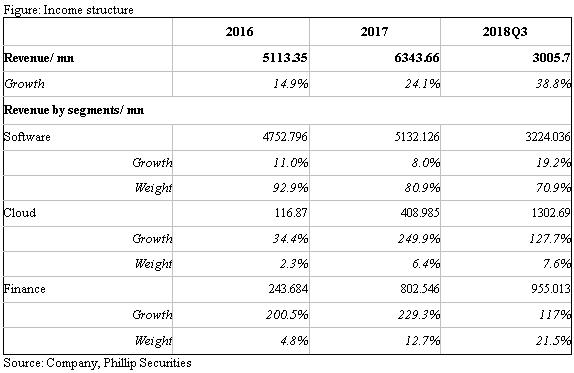

Cloud customers are expanding and the segment revenue grows rapidly. In 2017, cloud business revenue reached RMB409mn, a yoy increase of 249.9%. At the end of 2017, the number of corporate cloud customers was 3.93 million. As of the end of 18Q3, cloud business has accumulated 4.46 million registered corporate customers, and 324,500 paid ones, an increase of 39% from the end of 2017.

The cloud services focuses on following areas: Cloud platform, Cloud ERP, Domain Cloud, Industry Cloud, Changjietong yun, Enterprise Finance Cloud and Cloud Market. The income is mainly coming from operating service revenue, application service revenue, information and data service revenue, platform transaction revenue, share revenue from promotion of third-party applications, and charges for other value-added service.

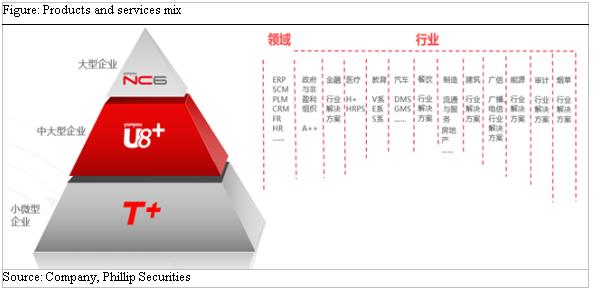

Software services business

Software service is the company's traditional business. The company started with financial software and gradually transformed focus to ERP software, expanding its business boundaries. Currently, the company has become the largest software services provider for management software, ERP software in Asia Pacific. It is also a leading provider of management software and services for multiple industries in China involving healthcare, finance, energy and so on.

Professional software products for large, medium and small micro enterprises, and also professional integrated solutions for multiple industries. It provides customers with standard products and solutions, specific services (like consultation, IT system construction, operational support), operational services (like business operations, application operations, platforms and data operations), etc. Income is mainly from standard product license charges and service charges. In 18H1, the amount of software customers totaled 2,170,900 (including 292,900 large and medium-sized enterprises and 2.418 million small and micro enterprises). In 18Q3, the software business realized revenue of RMB3.22bn, representing a yoy increase of 19.2%. We expect the segment maintain stable growth looking forward.

�Enterprise Finance Business

Providing financial services and acquiring payment licenses. The company established Beijing Changjietong payment technology company to carry out mobile internet payment services in 2013. In 2016, the company published Yongyou 3.0 Strategy and asserted finance segment as one of three major businesses. This segment mainly includes payment service business, Internet wealth management business and supply chain finance business for small and micro firms and individuals. In recent years, the financial services business has maintained a growth trend, and the scale of users continues to grow. During 18Q3, payment service income amounted to RMB88.28 mn, up by 51.9% yoy, and Internet investment and financing information service income amounted to RMB866.74mn, up by 120.9% yoy.

Changjietong payment services include: 1) RMB payment services for online Internet payment services (including gateway payment, express payment, bulk payment, scan code payment, authentication, etc.), through which users can purchase goods or services on Changjietong platform; 2) online collection, payment and authorization services; 3) offline POS billing and acquiring services for bank cards holders.

Besides, Yongyou Lihe financial services firm, one subsidiary, is committed to provide investment information services for investment clients and borrower clients. It helps clients direct borrowing by offering services like credit assessment, risk management, loan matching and other services. Clients are mainly white-collar workers, small and micro-enterprise owners and individual industrial and commercial households. Income is from agency information service fee paid by the borrowers.

Investment Thesis & Risks

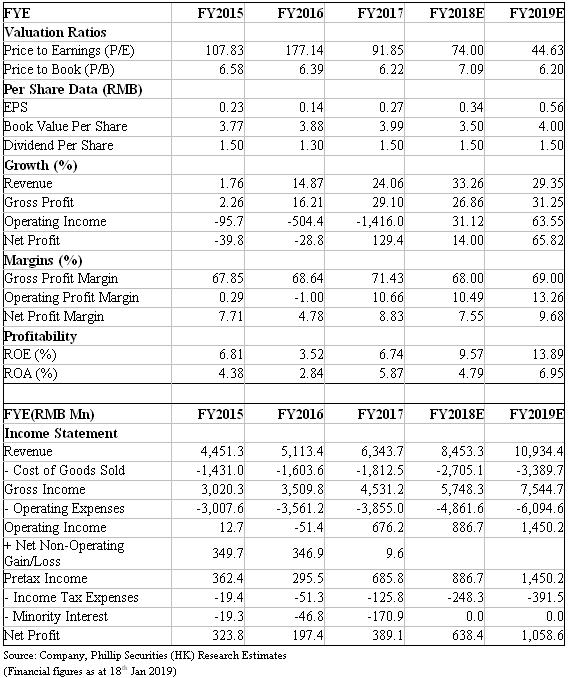

During 2012 to 2015, revenue growth slowed down dramatically. From 2013, the company began to deploy new business areas such as mobile payments and cloud. In 2016, the company asserted three core businesses of software, cloud services, and finance. We see from 2015 to 2017, business revenue rebounded, with a CAGR of 19.4%. In 18Q3, the company reported income of RMB4.548bn, a yoy increase of 38.8%, and realized net profit excluding non-recurring items of RMB317mn, turning losses into profits. In recent years, the proportion of cloud business and financial business has been increased. With the development of new business and improved business structure, we expect the company's revenue to maintain rapid growth in future.

Investment Thesis & Risks

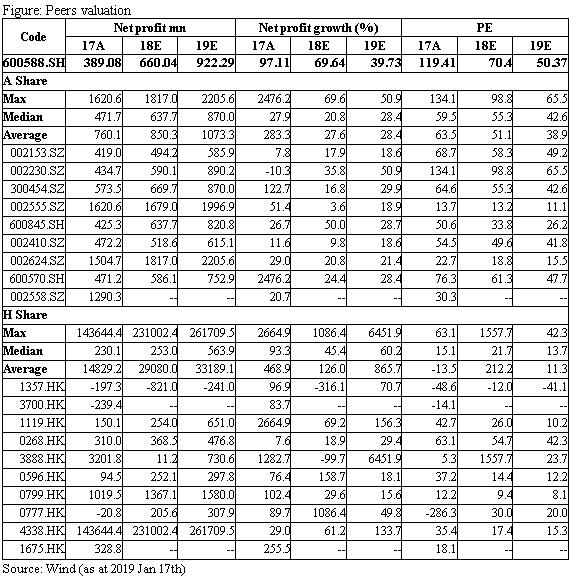

We initiate 2019 target price of RMB27.8. The revenue of cloud business and financial business will grow rapidly, and the software service business will develop steadily. It is estimated that the growth rate of topline in 2018E/19E will be around 33%/29%, and the net profit is expected to reach RMB638mn/1058 mn. Giving target price-earnings ratio 50 times, we initiate target price of RMB27.8.

�

Financials

Click Here for PDF format...