Investment Summary

China Education Group has engaged in higher and vocational education, and is now operating 7 schools in China. Based on the net profit attributable to owners in 2019, we assume a P/E ratio of 30 (the average of the past), deriving a target price of HK$13.41. We initiate a “Buy” rating with a potential upside of 26.0%. (Closing price at 22 Jan 2019)

The higher education industry has entered a stage of low growth, but the importance of private colleges has increased

Since 2000, the number of students in school has peaked, and in 2007 it has dropped to a single-digit growth rate. The growth rate of the new enrollment for the regular undergraduates and college students also dropped, from the highest in 1999 to 47.4%, to 1.7% in 2017. We predict that the proportion of the population aged 18-22 will continue to decline, but the rate of decline will slow down and is expected to reach 5.2% in 2022. In the 13th Five-Year Plan for the Development of National Education, the government aims to reach 50% in the gross enrollment rate of higher education in 2020. Thus, we estimate that the number of students enrolled will remain a low single digit growth in the future.

Despite the slowdown in the overall demand for higher education, the importance of private colleges in the higher education industry has increased. The number of new enrollment and students in the school in private colleges has been higher than the overall.

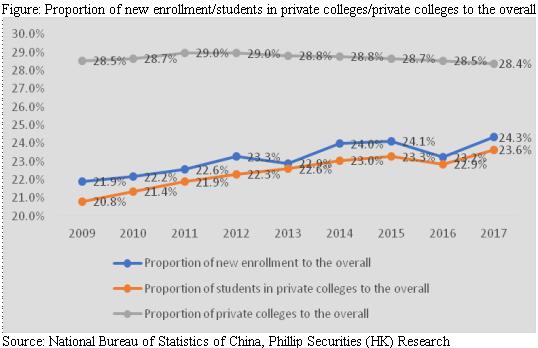

The proportion of private college enrollment to the overall has increased from 21.9% in 2009 to 24.3% in 2017; the proportion of students in private colleges to the overall also increased from 20.8% in 2009 to 23.6% in 2017. However, the proportion of private colleges to the overall has remained at around 28.5% between 2009 and 2017. We believe that the data shows the attractiveness of private institutions is gradually rising, and the public is increasing their acceptance to them.

Excellent education qualities in schools can be a buffer to the decline in the number of students

The schools of the Group are highly recognized by many institutes, e.g. nseac.com and iResearch China Alumni Association Network. In the "Chinese University Evaluation Research Report in 2019", Jiangxi University of Technology was rated as 6 stars and China's top private universities; Guangdong Baiyun University was also rated as a 3-star and regional first-class private university.

Good cost control

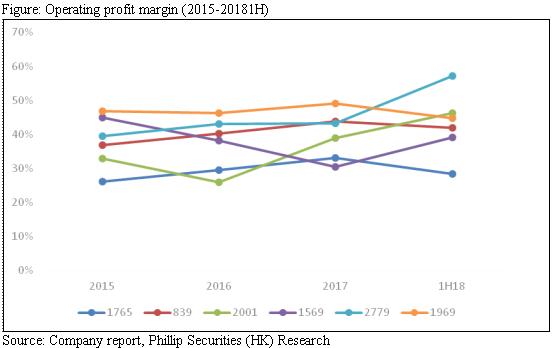

The cost control of the Group also performed well in comparison to the peers. From 2015 to the first half of 2018, the Group's operating profit margin increased steadily, at an average of 40.7%, ranking third, only lower than China Chunlai(1969.HK) and China Xinhua Education (2779.HK).

Abundant cash on hand with a clear plan on short, medium and long-term development

In the short term, the Group held cash of RMB 1.907 billion. In the medium term, the Group can raise RMB 2.6-3.2 billion through debt financing in the future. In the long run, the Group will make use of China Education Fund jointly with Value Partners for acquisitions.

Experienced management team

The co-chairs of the Group, Mr. Yu Guo and Mr. Xie Ketao, have been working in the education industry for 24 and 28 years respectively. Jiangxi School and two Guangdong schools have become well-known schools in the region under their leadership.

Business Overview

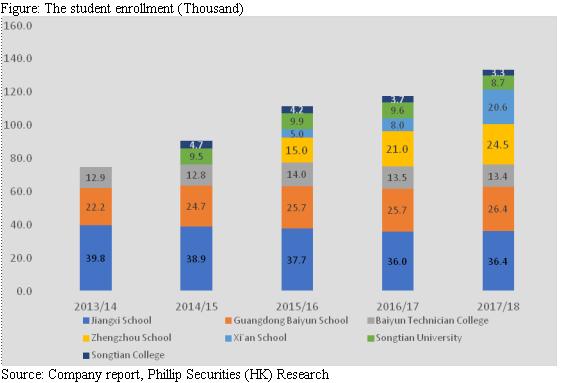

The Group are operating seven schools in Jiangxi, Guangdong, Henan and Shaanxi Provinces, and it just acquired a independent college in Shandong on 14 Jan this year.

Jiangxi University of Technology:

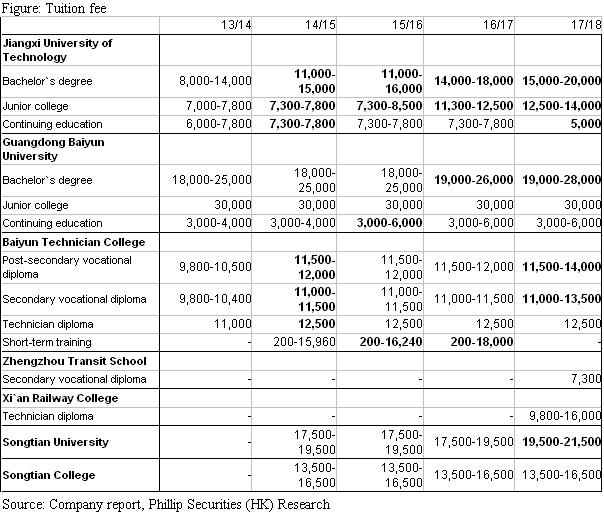

Established in 1994 by the co-chairman Yu Guo, the school is located in Nanchang, Jiangxi Province, formerly known as “Jiangxi Bluesky Academy”. The school is a private undergraduate college and offers 44 general undergraduate courses and 35 general specialist courses, including automotive service engineering, international economics and trade, computer science and technology, and has 12 colleges and 15 research institutions. The campus has an area of approximately 1.3 million square meters. As of the 2018/19 academic year, the number of students enrolled in schools was approximately 37,000. According to the Frost & Sullivan Report, the school is the largest private undergraduate college in China according to the student enrollment. The tuition fees for the general undergraduate, general and continuing education courses for the 2017/18 academic year are 15,000-20,000, 12,500-14,000 and 5,000, respectively.

Guangdong Baiyun University:

Founded in 1989 by co-chairman Xie Ketao, the school is located in Guangzhou, Guangdong Province. It is a private undergraduate college offering 52 general undergraduate courses and one general specialist course, including mechanical design and manufacturing and automation, business management, fashion design and engineering, and 16 colleges and 6 research institutes. The current campus area is approximately 351,100 square meters. The group is also building a new campus for the school. Once completed, the area will rise to 498,000 square meters. In the 2018/2019 academic year, the number of students enrolled was approximately 27,000. The tuition fees for the general undergraduate, general and continuing education courses for the 2017/18 academic year are 19,000-28,000, 30,000 and 3,000-6,000, respectively.

Baiyun Technician College:

Also founded by co-chairman Xie Ketao in 1989, the school is located in Guangzhou, Guangdong Province. The school is a private technical school with eight colleges, including: Mechanical and Electrical Engineering, Information Engineering, Economic Management, Tourism and Hospitality Management, etc., and provides 123 vocational education courses, including interior design and civil engineering, accounting, e-commerce and cooking. The campus covers an area of 61,800 square meters. In the 2018/2019 academic year, the number of students in school was about 13,000. The tuition fees for the Higher Vocational Education Diploma, Secondary Vocational Education Diploma and Technician Diploma in the 2017/18 academic year are 11,500-14,000, 11,000-13,500 and 12,500 RMB respectively.

Zhengzhou City Rail Transit School:

Established in 2010 as a secondary specialized school for urban rail transit talents, the school is located in Zhengzhou City, Henan Province. The group acquired 80% of the equity in March 2018 for RMB 850 million. It now has 10 secondary vocational education diploma courses, including: urban rail transit operation management, urban rail transit vehicle use and maintenance, urban rail transit power supply, urban rail transit signals, four majors as the core specialty. The campus area is about 300,000 square meters. The number of students in the academic year 2018/2019 is about 27,000. The tuition fee for the Diploma in Secondary Vocational Education for the 2017/18 academic year is RMB 7,300.

Xi`an Railway College:

The school is located in Xi`an, Shaanxi Province. The group acquired 62% of the equity in March 2018 for RMB 580 million. Founded in 1997, the school is a full-time orbital comprehensive vocational college, which aims to train high-speed rail application talents. The school consists of three parts, including: high-speed rail passengers, railway technology, and intelligent applications, and nine vocational education courses, including railway passenger transport services, urban rail transit operations and management, electrified rail power supply, railway engineering technology, and cruise crew services. . In addition, the campus's total area is more than 300,000 square meters. In the 2018/19 academic year, the number of colleges was about 28,000. The tuition fee for the Diploma in Technology for the 2017/18 academic year is RMB 9,800-16,000.

Songtian University:

The school is located in Guangzhou, Guangdong Province. It was established in 2000 and is an undergraduate independent college acquired by the group in June 2018. It offers 30 general undergraduate courses. In the 2018/2019 academic year, there were more than 9,000 students.

Songtian College:

The school is located in Guangzhou, Guangdong Province. It was also established in 2000. It was acquired by the group in June 2018 with RMB 540 million together with Songtian University. The school is a private higher vocational college with 7 teaching departments and 22 general specialist courses. In the 2018/2019 academic year, Songtian College's full-time students were approximately 4,000 students.

On January 14 2019, the Group announced the acquisition of an independent college in Shandong Province, University of Jinan Quancheng College, with a total consideration of RMB 252 million for 50.91% equity. It has 38 undergraduate majors and 9 specialties, covering 6 disciplines including economics, management, literature, science, engineering and art. There are currently 8,529 students. As of December 31, 2018, the school's net profit after tax was RMB 404,000. The Group's current aim is to acquire the remaining 49.09% equity through the tendering process by the Shandong Cultural Property Exchange. Upon completion of the acquisition, the group will own 100% of the equity. We have not included this acquisition into our earnings forecast yet.

Industry Overview

History of development

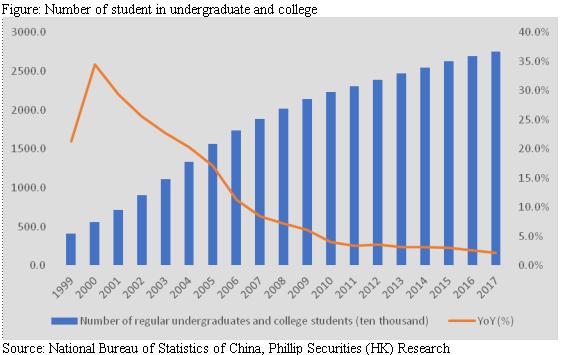

Under the rapid growth of the higher education industry in the past two decades, the number of students enrolled in undergraduate and college has increased from 4.13 million in 1999 to 27.536 million, with a CAGR of 11.1%. However, since 2000, the number of students in school has peaked, and in 2007 it has dropped to a single-digit growth rate. After 2010, it entered a stage of low single digit growth rate (as low as 5%), where it grew by only 2.1% in 2017.

The increase in the number of students enrolled in undergraduate and college can be interpreted as the difference of the number of new enrollment and the number of graduates. Since the number of graduates can be estimated from the number of new enrollment in the previous three to five years, so the increase in new enrollment has a significant impact on the growth of the number of students enrolled.

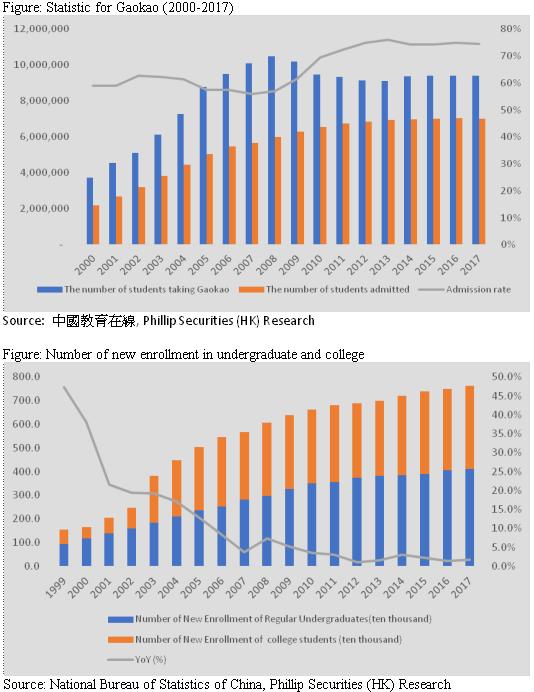

In the major enrollment channel - National Higher Education Entrance Examination (Gaokao), the number of candidates for Gaokao reached its peak in 2008, about 10.5 million. It then fell back to the level of 9 million, where the recent number of candidates in 2017 was 9.4 million. Although the number of candidates has decreased, the number of students admitted has remained stable at about 7 million because of the increase in admission rates. Due to the decline in the number of new enrollments in Gaokao, the growth rate of the new enrollment for the regular undergraduates and college students also dropped, from the highest in 1999 to 47.4%, to 1.7% in 2017.

Future development

The number of students in undergraduate and college can be decomposed into the population aged 18-22 multiplied by the gross enrollment rate of higher education, so we can estimate the number of students enrolled in the future from these two factors.

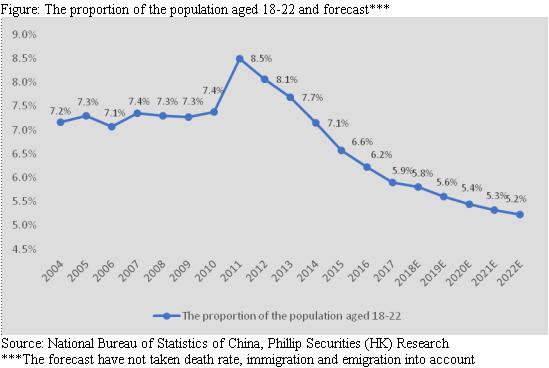

The population aged 18-22

Based on the population data of the National Bureau of Statistics, we estimate that the proportion of population aged 18-22 to the total population from 2004 to 2017. From 2004 to 2010, the proportion has remained at 7.1%-7.4%. However, since the sharp rise to 8.5% in 2011, the proportion has been going down, mainly because the birth rate has been falling since 1987. In 2017, this percentage has fallen to 5.9%, the lowest since 2004.

According to the results of the National Bureau of Statistics` population sampling survey, we predict that the proportion of the population aged 18-22 will continue to decline, but the rate of decline will slow down and is expected to reach 5.2% in 2022.

The gross enrollment rate of higher education

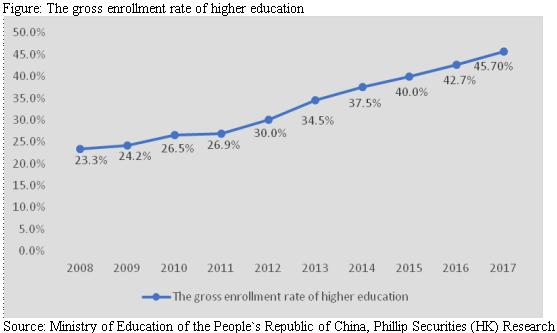

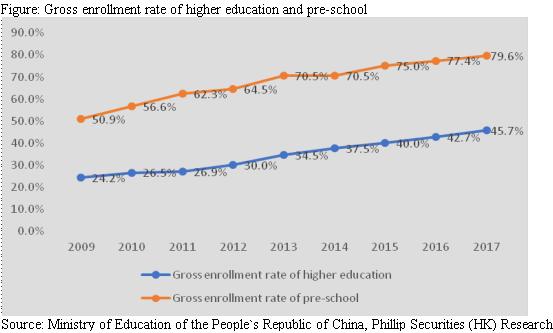

The gross enrollment rate of higher education in China has been uptrend, rising from 23.3% in 2008 to 45.70% in 2017. In the hope of universal higher education, the government has been working hard to increase the gross enrollment rate of higher education in the country. In the 13th Five-Year Plan for the Development of National Education, the government aims to reach 50% in the gross enrollment rate of higher education in 2020. In the past gross enrollment target, the government's goals can usually be reached, or even exceeded, so we believe that the gross enrollment rate can reach 50% by 2020, and help to increase the number of students in undergraduate and college.

Although the gross enrollment rate of higher education has increased significantly, the number of people aged 18-22 has decreased, thereby offsetting the increase in the gross enrollment rate. In view of this, we estimate that the number of students enrolled will remain a low single digit growth in the future.

A more prominent role of private college

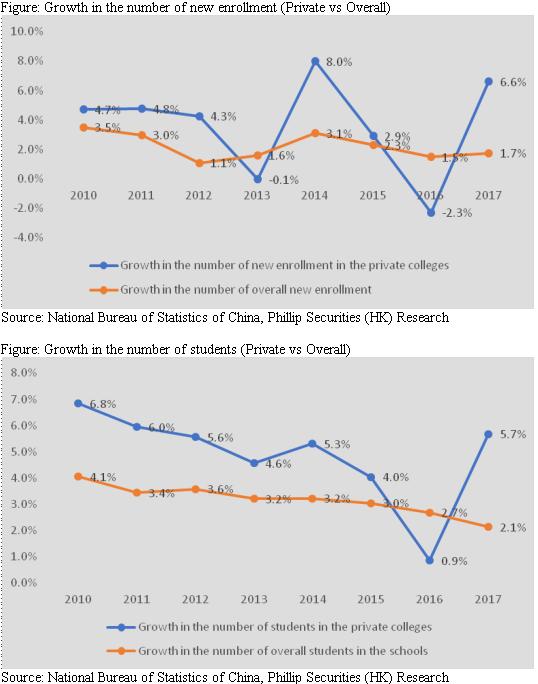

Despite the slowdown in the overall demand for higher education, the importance of private colleges in the higher education industry has increased. The number of new enrollment and students in the school in private colleges has been higher than the overall. In terms of the number of new enrollment, the growth in private colleges was higher, reaching 8% in 2014, but the growth rate was more volatile than the overall. In 2017, the number of new enrollment in private colleges increased by 6.6%, 4.9% higher than the overall growth. In terms of the number of students in the school, the growth of private college is also higher, except for 2016. In 2017, the number of students in the school in private colleges has increased by 5.7%, which was 3.6% higher than the overall growth.

In addition, the proportion of new enrollment and students in private colleges to the overall has shown the importance and attractiveness of private colleges are gradually increasing. The proportion of private college enrollment to the overall has increased from 21.9% in 2009 to 24.3% in 2017; the proportion of students in private colleges to the overall also increased from 20.8% in 2009 to 23.6% in 2017. However, the proportion of private colleges to the overall has remained at around 28.5% between 2009 and 2017. In other words, the increase in the number of new enrollment and the number of students in private schools is not due to the increase in the number of schools. We believe that the data shows the attractiveness of private institutions is gradually rising, and the public is increasing their acceptance to them.

Policies in the industry

Compared to the compulsory education industry, we believe that the policy risk of the higher education industry is lower because the government indicates that the higher education business allows for profitability. In November 2016, the 12th National People's Congress voted to amend the "People's Republic of China Private Education Promotion Law" and proposed the implementation of classified management - for-profit and non-profit, where it clearly indicates that compulsory education can only choose non-profit. In other words, the profits made by compulsory education listed companies will not be able to be distributed. Although compulsory education listed companies are currently making use of related party transactions for profit transfer to pay dividends, we believe that such practices are likely to be regulated in the future because non-profit schools do not pay taxes on tuition fees, which means it is detrimental to the fairness the taxpayers of the country, so we believe that this practice may be rectified.

In contrast, higher education can choose for-profit. Although the company needs to pay taxes and pay land transfer fees after choosing for-profit, it is believed that there will not be such a big impact as compulsory education. Besides, as education is one of the major industries that await for development, the market generally believes that profits tax is likely to be only 15%. The land transfer fees can be amortized into 50 years, so the impact on the income statement is not significant. This shows that the impact of higher education on policy is not as large as the market thinks.

Although it is possible to choose for-profit, some still think that the education industry is risky. On November 7, 2018, the State Council promulgated the "Opinions of the Central Committee of the Communist Party of China on the Deepening Reform and Standardization of Pre-school Education". What cause the largest impact on the capital market is Article 24, where it states "The private kindergarten are not allowed to be listed by either alone or as a part of the assets packaged. Listed companies shall not invest in for-profit kindergartens through the secondary market financing, and shall not purchase for-profit kindergarten assets by issuing shares or paying cash." Market Concerns that even though the government allows kindergartens to choose for-profit, it still introduces policies prohibiting the business is listed and financed in the secondary market, and these policies may be also implemented in the higher education industry in the future. However, we believe that it is not possible to introduce such policies in the higher education sector because higher education is rapidly increasing the gross enrollment rate, and the funding from the secondary market is important for expanding the size of the industry. On the contrary, the gross enrollment rate of pre-school education is already at a high level, and the capital demand from government for the secondary market is not as high as that of higher education. That is why it tried to prohibit the for-profit kindergarten listed in the secondary market in attempt to resolve the problem of high tuition fees in kindergartens.

In fact, there are also some policies that benefits higher education in the People's Promotion Law. Article 7 of the "Regulations on the Implementation of the Private Education Promotion Law of the People's Republic of China (Revised Draft) (Draft for Review)" promulgated in August 2018 states that "public schools may not hold or participate in the establishment of for-profit private schools. If public schools hold or participate in a non-profit private school, it shall be approved by the competent department, and shall not use the state's fiscal funds, and shall not affect the teaching activities of public schools, and may not obtain income through brand output." This means that some domestic independent colleges that set up by relying on the brand of public university need to be separated. There are currently about 260 independent colleges, which has led to a surge in potential acquisition targets for higher education groups. In addition, Article 53 (Private schools enjoy the preferential tax policies stipulated by the State. Non-profit private schools apply to the taxation policies issued by the financial department and taxation department of the State Council on public schools, and the corresponding tax burdens are reduced or exempted; The relevant industrial policies encouraged by the state to enjoy the corresponding tax incentives shall be formulated by the financial department and the taxation department of the State Council in conjunction with the relevant administrative departments of the State Council. The price policy of electricity, water, gas, and heat are the same for both public and private schools.) also shows that the government provide subsidies to for-profit schools.

To sum up, higher education industry in China has entered a period of low growth, and it is common to see company to grow through acquisition. However, as the role of private higher education institutions has become more prominent, it has gives momentum to this sector, making the growth rate generally higher than the overall. At the same time, we believe that the policy risk of higher education is the smallest among all kinds of education and therefore is worthwhile for long-term investment.

Competitive advantages

Excellent education qualities in schools

The quality of education in schools determines the competitiveness of schools for enrollment. This ability is especially important during a decline in the number of student. In theory, when the number of students declines, the first to be affected is the schools that are in poor quality of education. Students prefer to choose schools with better quality. This makes the schools with poor quality of education are inferior in student enrollment. Therefore, we consider the quality of good education helps schools to face the declining number of students.

Based on nseac.com, Jiangxi University of Technology has ranked first in terms of overall competitive strengths in the Private University and College Ranking of China for nine consecutive years since 2009, ranking third in the latest rankings. According to the "Chinese University Evaluation Research Report in 2019" by iResearch China Alumni Association Network, Jiangxi University of Technology is ranked 21st, and rated as 6 stars and China's top private universities. At the same time, the school was one of the first batch of private undergraduate colleges approved by the Ministry of Education in Jiangxi Province.

Guangdong Baiyun College was ranked first in terms of overall competitive strengths among top 10 private universities and colleges in Guangdong province by Guangdong Provincial Academy of Social Sciences and Guangdong and General Survey and Research Centre from 2005 to 2014 (this award has terminated after 2014). Based on the ranking of overall competitive strengths in the Private University and College Ranking of China from 2018 to 2019, the school ranked 33rd and rated 3 stars. In the "Chinese University Evaluation Research Report in 2019" of the iResearch China Alumni Association Network, Baiyun College ranked 72, and was rated as a 3-star and regional first-class private university. The school is also one of the first batch of private undergraduate colleges established in Guangdong Province.

From 2008 to 2014, Baiyun Technician College was ranked first in terms of educational competitive strengths among technical schools in Guangdong province by Guangdong Provincial Academy of Social Sciences, Guangdong General Survey and Research Centre (this award has terminated after 2014).

The newly acquired Zhengzhou City Rail Transit School was recognized as an outstanding private school by Henan Provincial Education Department in 2016; Xi`an Railway College was awarded Outstanding Specialized Private University and College in China by China Private Education Association Higher Education Specialized Committee in 2012; Songtian University was awarded Top Ten famous Chinese Private College Brands by China Educators Association, China Private Educators Association.

From the awards of the schools, we believe that the quality of the education of the Group is relatively good compared to other private schools, which will help enhance the competitiveness of the Group.

Good cost control

Apart from the excellent quality of education, the cost control of the Group also performed well in comparison to the peers. In order to accurately measure the profit margin of the operating business, we subtract the gross profit by the general sales and administrative costs, and divide by the income to measure the profit margin of each company's operating business. From 2015 to the first half of 2018, the Group's operating profit margin increased steadily, at an average of 40.7%, ranking third, only lower than China Chunlai(1969.HK) and China Xinhua Education (2779.HK).

Abundant cash on hand with a clear plan on short, medium and long-term development

For education companies, acquisitions are a common way of growth. It is especially important for higher education. It takes many years to establish a bachelor's degree programme, because all new schools must start with a junior college programme and it require to have at lease three years of graduates to apply for a bachelor degree, which takes 12-13 year for setting up a bachelor's degree programme. In view of this, higher education companies tend to acquire existing higher education institutions with bachelor's degree programmes. However, it means that the group needs sufficient funds to make acquisitions. Thus, we believe that the cash on hand and future funding source are one of the crucial considerations.

In the short term, as of August 31, 2018, the Group held cash of RMB 1.907 billion, assuming that the acquisition of each new school would require approximately RMB 600-700 million, representing cash on hand to the acquisition of approximately three new schools.

In the medium term, the Group can raise funds through borrowing. As of August 31, 2018, the Group's debt to equity ratio was only 3.7%. The Group expect that the future target of the ratio will reach 40-50%. With net assets of RMB 6.4 billion currently, the group can raise about RMB 2.6-3.2 billion, assuming that each new school costs about RMB 600-700 million. It is enough for the group to acquire 4-5 schools. Thanks to the stable cash flow in the education business, we believe that even if the debt to equity ratio of the Group rises sharply in the short term, it will not bring serious liquidity problems to the Group.

In the long run, the Group will take advantage of the China Education Fund with Value Partners for acquisitions, where the AUM of the fund is RMB 5 billion. The Group provides management services to the schools under the fund and receives management fees from them. The Group and Value Partners both share a shareholding in the fund, so the group needs to share the 2% management fee (1% per person)with them. The fund is still in the stage of fund raising, with the first phase contributing about 1.5 billion and expect that the whole amount will be collected around April and May of next year.

The Group has a clear plan on funding sources for short, medium and long-term. Especially long-term plan, only Minsheng Education (1569.HK) currently has the similar plan. A clear financing plan undoubtedly ensures the Group's future growth momentum.

Experienced management who is capable to improve the operation of the acquired schools

The Group's growth is mainly due to the acquisition of new schools, and the targets are mostly schools with poor management but potential for improvement. Therefore, whether the management of the Group has sufficient capacity to improve the target operation is the key to the success of the acquisition.

Mr. Yu Guo, the co-chairman of the group, has been working in the education industry for 24 years. In 1994, he founded Jiangxi Advanced Vocational School (predecessor of Jiangxi University of Technology). The school was promoted from a vocational school to one of the largest private universities in the country, showing the remarkable ability and experience in school operations from him. In addition, Mr. Yu has also held various public positions, such as: representatives of the Ninth to Eleventh National People's Congress, vice chairman of the Jiangxi Provincial Federation of Industry and Commerce, vice president of the China Civilian Education Association, member of the Standing Committee of the 12th Jiangxi Provincial People's Congress and Jiangxi Province Honorary President of the Youth Federation. The contribution and achievements in private education from Mr.Yu are reflected by the number of public positions.

Mr. Xie Ketao, co-chairman of the group, has been engaging in the education industry for 28 years and founded Guangdong Baiyun College and Baiyun Technician College in 1989. The total number of students in these schools is about 40,000, and according to the "Chinese University Evaluation Research Report in 2019", Guangdong Baiyun University ranked second among the private university in Guangdong, only behind Guangzhou Business School, showing the 28-year achievements of running a school from Mr. Xie. In addition, Mr. Xie has served in various public positions, such as: members of the 9th and 10th Guangdong Provincial People's Political Consultative Conference Committee, vice president of the Guangzhou Vocational Skills Teaching Research Association, honorary chairman of the Guangzhou Young Entrepreneurs Association, and vice chairman of the China Civilian Education Association. President and representatives of the 12th People's Congress of Guangdong Province.

Judging from the experience of the two co-chairmans, we believe that they will be able to improve the operation of the acquisition target and inculcate the existing successful operation model to enhance the value of the school, thanks to their expertise in education. For example, since Xi`an Railway College is a boarding school, there is no student-teacher ratio limit. Before the acquisition, it was 1:60, but unlike the liberal arts, the requirements on technique subjects for student-teacher ratio were stricter, so that the quality of teaching could be guaranteed. Therefore, the group reduces it to 1:30 (the current level of Baiyun technicians college).

Earnings forecast

Revenue

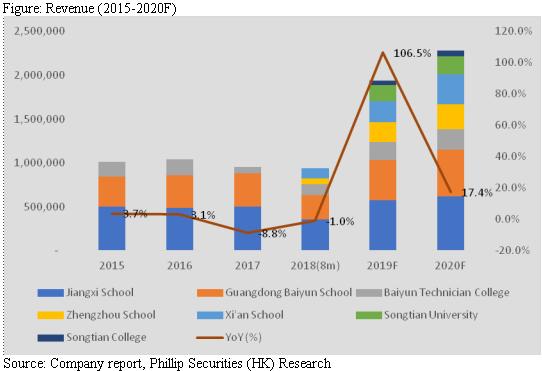

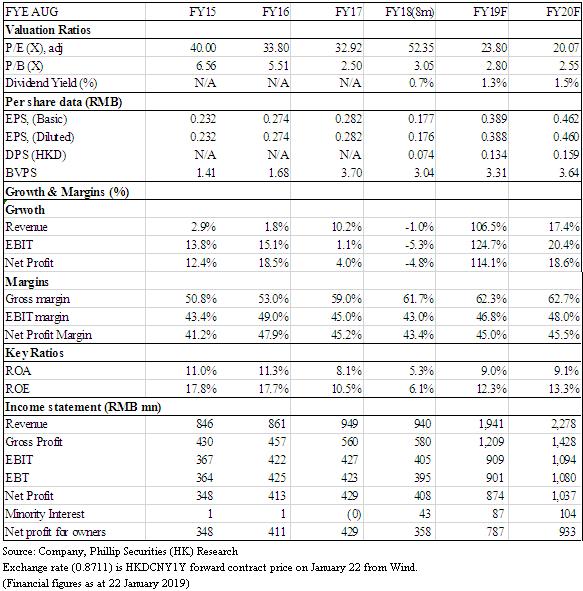

We expect revenue to increase by 106.5/17.4% in 2019F/20F. The strong growth in 2019 was mainly due to the fact that the group changed its reporting period in 2018, so only 8 months of operating data was recorded in 2018. Besides, we expect Songtian University and Songtian College to be consolidated in 2019, so revenues in 2019 recorded a significant increase.

Student enrollment

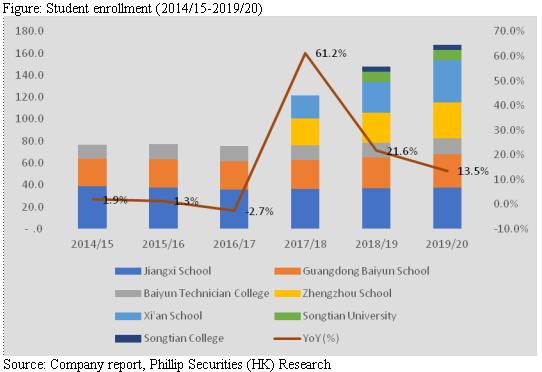

We expect the number of students to rise by 21.6/13.5% in the 18/19 and 19/20 academic years. The growth in 18/19 was partly from the acquisition of Songtian University and Songtian College. However, we believe that their growth rate should take a few year to see a significant increase because the number of their new enrollment was relatively higher, making the number of graduates in these years more. Furthermore, their enrollment quotas have been reduced due to a heavy debts, leading to fewer enrollments in these years. But the number of enrollment quotas has rebounded since the group took over the school. Therefore, they need time to absorb the number of graduates in the early years and increase the number of enrollment students before a significant increase in the number of students. And we expect Jiangxi University of Technology to be saturated, remaining its number of students. In Guangdong Baiyun University and Baiyun Technician College, Baiyun University is expanding, where the first phase of the new campus will be completed in March 2019, and will recruit in 2019 with about 8,000 capacity; the second phase will be 2019 or 2020. Construction began in 2021, with an additional capacity of approximately 18,000, adding a total of 26,000 new capacity, and the old campus will be transfer to Baiyun Technician College.

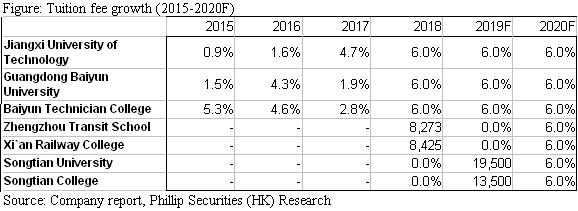

Tuition fee growth

We expect tuition fees for schools in Jiangxi and Guangdong school to increase by 6% in 2019F/20F. Since Jiangxi and Guangdong do not require government approval for tuition fees, but Zhengzhou and Xi`an do, Zhengzhou and Xi`an will not increase tuition fees every year, but every two to three years. Therefore, we estimate that Zhengzhou and Xi`an schools will only increase tuition fees in 2020F.

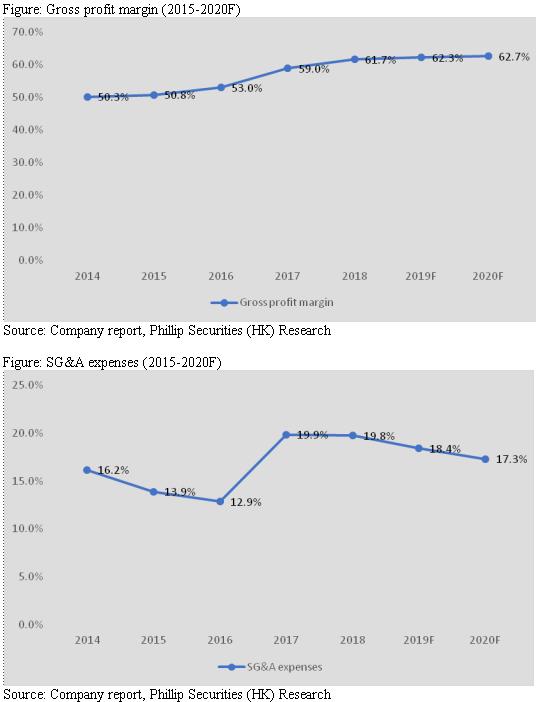

Gross profit margin and SG&A expenses

We expect gross profit margin and SG&A expenses for the 2019/20F to be 62.3%/62.7% and 18.4%/17.3%, respectively, mainly due to the larger operation scale, leading to economies of scales.

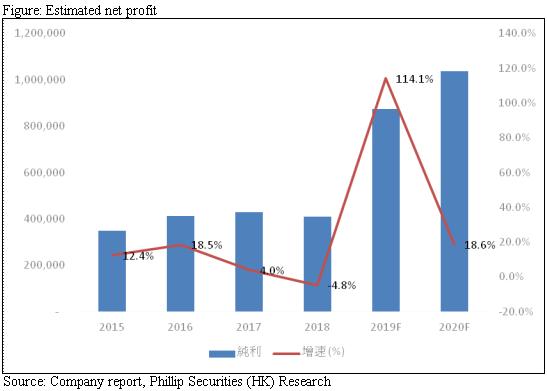

Net profit

We expect net profit growth in 2019/20F to be 114.1%/18.6%. The sharp increase in 2019F was mainly due to the fact that the group changed its reporting period in 2018, so only 8 months of operating data has been recorded in 2018 and Songtian University and Songtian College will be consolidated in 2019.

Valuation

The Group are good in the quality of education and cost control, with a clear plan on short, medium and long-term development and expertise in school operation. We believe that the Group will be one of the leaders in higher education. Based on the net profit attributable to owners in 2019, we assume a P/E ratio of 30 (the average of the past), deriving a target price of HK$13.41. We initiate a “Buy” rating with a potential upside of 26.0%. (HKD/CNY=0.8711)

Risk

1. A plunge in birth rate in China

2. A sharp change in policies to education sector

3. The Group fails to improve the operation of the acquired schools

Financials

Click Here for PDF format...