Both Hong Kong and Mainland stock markets turn bear in 2018

Looking back on 2018, both the mainland stock market and Hong Kong stock market experienced considerable declines, and the market entered a "bear market". The SSE Composite Index fell from its peak of 3587 in January 2018 to its lowest of 2440 in January 2019, with a decline of 45% and a P/E ratio of 15 times to 11 times, a new low since 2015. The Hang Seng Index fell from its high of 33484 in January 2018 to 24540 in November 2018, down by 36%, and is now valued at around 9.5 times. The Hang Seng China Enterprises Index fell by 43% from 13962 to 9761, and its current valuation is about 8.5 times. In terms of sectors, in 2018, the IT industry declined the most, down by 23.4%, followed by the financial industry and industry, down by 22.66% and 20.17%, respectively.

The US economy is moderate and the recovery is sustained, but the growth rate is slowing

On the US side, the market is concerned about whether the Federal Reserve will slow down the increase in interest rate. There is little inflationary pressure in the US at present, and there are signs that fundamentals are beginning to be threatened, including the expected slowdown in global economic growth and the partial upside-down of the fructus curve of US national debt. Powell, the FED Chair, has softened his tone recently, saying that he has not seen the risk of recession increase. Based on the current low level of inflation, the Federal Reserve can be patient and flexible on interest rates.

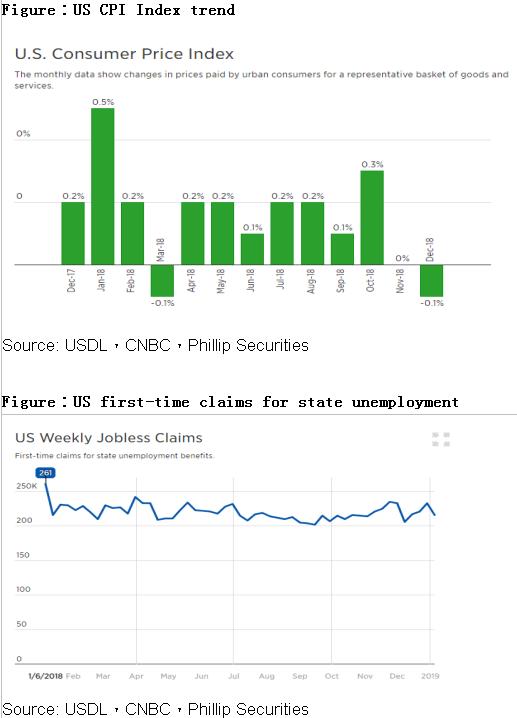

Affected by the drop-in oil prices, the US consumer price index (CPI) fell 0.1% on a monthly basis last month, the first and worst performance since March last year. It was worse than the flat performance in November. It rises by 1.9% annually, less than the 2.2% rise in November. While according to the economic data, the economy remained stable. As at the week of January 5, the number of first-time claims for unemployment benefits in the United States fell to 216,000, better than market expectations, which was below 300,000 for the 201st consecutive week, the longest recorded period since 1970, reflecting the continued stability of the labour market.

The market is concerned about whether the US will impose tariffs on commodities exported from China as soon as the 90-day deadline (March 1) for Sino-US trade war negotiations arrives, which may have a major impact on financial markets. We believe that trade frictions can be alleviated in the short term from recent comments by senior leaders of China and the United States, including Trump. However, there are still major differences on intellectual property rights and technology transfer. It is expected that major agreements on these issues will be difficult to reach before the 90-day deadline (March 1) and these issues will continue to influence the market for some time to come.

Uncertainty may arise in the European economy

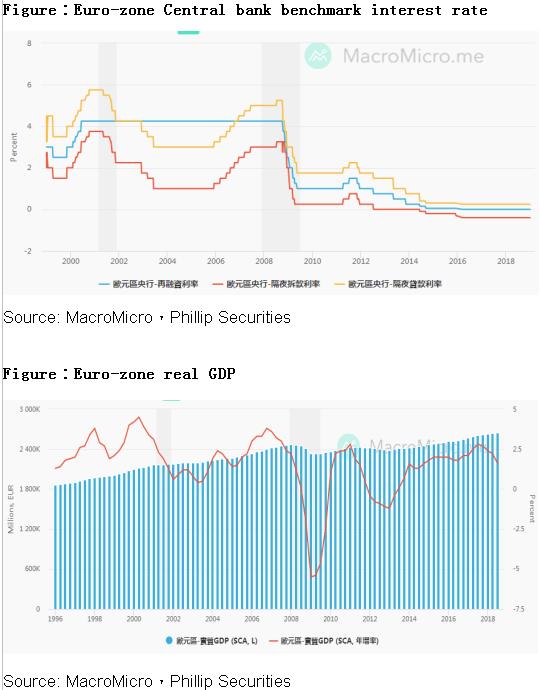

In terms of the European economy, although the European Central Bank (ECB) stated at its monetary policy meeting in December 2018 that it would end QE by the end of 2018 and maintain its current asset-liability scale to show its determination to promote the normalization of monetary policy. However, the wording has been changed from "continuous reinvestment after the end of QE" to "continuous reinvestment after the first interest rate increase". This reflects the ECB's more conservative economic outlook. Meanwhile, the World Bank also downgraded its forecast for real GDP growth in the euro area in 2019 to 1.6%, down by 0.1% from earlier forecasts. In terms of the pace of interest rate increase, the ECB indicated that it would maintain its current interest rate level until the summer of 2019 to ensure that core inflation in the euro area would be close to but below 2% in the medium term.

In terms of Brexit, the Brexit agreement made by Theresa May, the Prime Minister of the UK, was not accepted, so there was voice in support of a second referendum or temporary non-exit. The failure to implement the Brexit agreement has caused uncertainties to Britain. If the agreement can’t be concluded till the exit day in 2019, Britain will probably exit from European Union without an agreement. This will undoubtedly have an impact on the British economy and even the world.

China's economy is facing the challenge of deceleration, and it is difficult for the underpinning policy to hedge completely in a short term

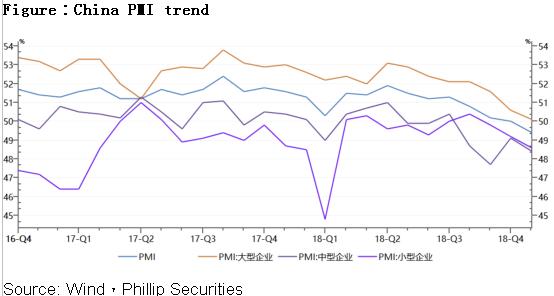

Since the second half of 2018, China's macroeconomic momentum has continued to weaken, with GDP growth accelerating from 6.8% in the first quarter and 6.7% in the second quarter, to 6.5% in the third quarter, a new low after the subprime crisis, ranking only second to the 6.4% in the second quarter of 2009. Macroeconomic data, such as industrial added value above scale, PMI, growth of social consumer goods, growth of real estate sales, growth of import and export, and CPI/PPI, shows an accelerated downward trend.

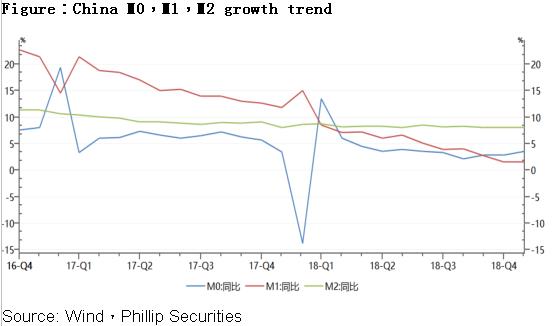

In terms of monetary environment, due to the influence of financial deleveraging policy, the yield of one-year treasury bonds continues to decline, but the proportion of medium-term and long-term loans to new social financing continues to shrink, reflecting the difficulty of financing in the real sector. What is equivalent to it is the decline of production index. In December, the PMI of manufacturing industry was 49.4%, down by 0.6 ppts from last month, breaking through the 50% threshold for the first time in nearly two years.

In order to cope with the financing difficulties of the real sector under the circumstance of financial deleveraging, the Central Bank of China has dramatically reduced the reserve requirement ratio four times since 2018. According to some data at the end of the year, it has shown a certain underpinning effect. However, we believe that it is still difficult to hedge the bad news of economic downturn in a short term due to the lag of policy effectiveness and the constraints of uncertain prospect of Sino-US trade negotiations.

2019 Hongkong stock market outlook

We believe that the future trend in Hong Kong stocks is constrained by the "race between fundamentals and underpinning policies".

1. In terms of the fundamentals, we expect that in 2019, especially in the first half of the year, the downward pressure of the economy will remain high, and the drag of exports on the economy will be particularly obvious in the first half of 2019. The annual GDP growth rate will drop to 6.2-6.3%.

2. In terms of monetary environment, the correction of supply-side reform, accompanied by moderate easing of monetary policy, will slow down financial deleveraging, and the proportion of direct financing is expected to expand. Given moderate inflation, it is expected that the Central Bank will still make cuts to interest rates and required reserve ratios in 2019.

3. In terms of fiscal policy, the growth rate of infrastructure will rise again. Underpinning policies such as tax cuts for individuals and enterprises, SMEs' support, and consumption incentives will be formulated one after another, which may be intensified under the premise of insufficient external economic momentum.

4. After the interim statements of enterprises, the profit growth of Hong Kong stocks bottomed out and raised again, the underpinning policy gradually exerted its effect, the fundamentals of enterprises improved structurally, and the valuation pressure risk fully released. All these are expected to bring some valuation repair opportunities for Hong Kong stocks. Generally speaking, the overall trend in Hong Kong stocks is weak in the first half of the year and unstable in the second half of the year. Hong Kong stocks fluctuate between 24,000 and 30,000 points.

Sector outlook and stock recommendation

Automobile:

Driven by the withdrawal of the preferential policy of purchase tax for passenger car and the drag of macroeconomic decline, China's automotive industry as a whole was under pressure in 2018, with sales falling by 2.8% Y-o-Y. The performance of sub-industries is different, SUV's growth turns downward, and new energy vehicles are rising rapidly. There are obvious differences among automobile enterprises. Growth of Japanese-brand vehicles is strong, part of the independent brand inventory is rising, industry competition is intensifying, and car companies have difficulty in getting profits. We believe that the differentiation of the car market will continue in 2019. Japanese and German car companies are expected to continue to develop steadily by virtue of the reduction of price and strong cycle. Leading enterprises of independent brands will continue to seize the market by virtue of upgrading their product ability, and their market share will be more concentrated. We suggest paying attention to GAC (2238 HK), BYD (1211 HK), Great Wall Motor (2333 HK), and Geely Auto (175 HK).

Pharmaceutical sector:

The introduction of the centralized procurement policy in 2018 has put pressure on many drugs to reduce prices, causing market concern and the decline of pharmaceutical stocks in general, but the decline also means opportunities. We emphasize that the long-term competitiveness of pharmaceutical enterprises lies in their innovation ability. Companies with strong research strength and rich R&D reserves will be in a favourable position in the competition. Although price reduction and cost control are a trend, the increase of sales volume brought by price reduction is still conducive to the increase of enterprise revenue. In addition, the new policy of Hong Kong Stock Exchange allows non-profit biotechnology enterprises to be listed, which changes the situation that biotechnology enterprises in the initial stage are difficult to be listed, and is conducive to supplementing capital and enhancing competitiveness of such enterprises. In the long run, innovative pharmaceutical enterprises are one of the most potential segments in the future pharmaceutical sector. We suggest that attention should be paid to CSPC (1093 HK) and Sino Biopharm (1177 HK).

TMT sector:

In March last year, the central government issued the Plan for Deepening the Reform of the Party and State Institutions, saying that the reform of the institutions has suspended the approval of the edition number. Since the end of March, regulators have not issued new game licenses, which has prevented domestic game developers from commercializing games. However, at last year's annual meeting of the Chinese game industry, Feng Shixin, deputy director of the Publishing Bureau of the Publicity Department of the Central Committee of the CPC, said at the meeting that the "first batch of submitted games" had been audited and the edition number was being approved and issued. After this remark, the State Administration of Press, Publication, Radio, Film and Television announced that 80 games were approved, and then another 84 games would be approved. The approval of the game edition number means that the game can be commercialized, which will help improve the profit forecast for 2019. We recommend that attention should be paid to developers and distributors of mobile games, such as Tencent (700.HK). Although there are no Tencent games in the first two rounds of game approvals, we believe that the re-approval of the game edition number indicates that the game policy in 2019 will be normalized.

Consumption sector:

The impact of the Sino-US trade war on China's economy has emerged, and the consumer market has also been hit in tandem, leading to the saying of "consumption degradation" among the public. We believe that Chinese government has or is preparing to launch the achievements of the easing policy, but it still needs time to be observed. Therefore, in the retail sector, we recommend consumer goods and dairy stocks, such as Hengan International (1044) and Mengniu (2319), which are less affected by the economy.

Click Here for PDF format...