Investment Summary

Sales in December has increased by 6.5% Y-o-Y

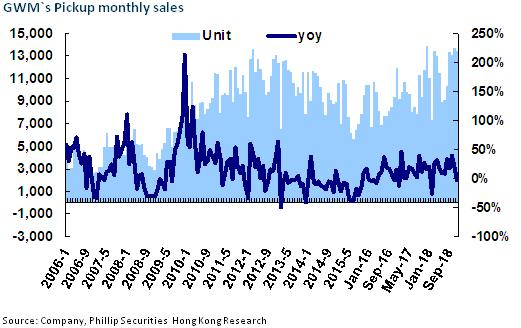

December sales report of Great Wall Motor (GWM) showed that the total sales of vehicles in December recorded a Y-o-Y increase of 6.5% to 134,000, with SUV up by 8.32% to 119,000, accounting for 89.2%. The sales volume of pickup reached 13,435, a Y-o-Y decrease of 2.9%; while the sales volume of sedan reached 1,055, representing a decrease of 34% Y-o-Y. Since November, the company's monthly sales growth ratio has gradually stabilized from the Y-o-Y decline in the third quarter, and the growth rate expanded in December, reflecting that the company's transformation strategy is paying off.

In terms of vehicle types, HAVAL H6, the main force, maintained a stable sales volume of over 50,000 units, down 8.75% Y-o-Y; sales volume of older H2/H7 (11,772/2,649 units) slowly ceded to newer M6/F5 (15,042/10,133 units), while sales of the newest F7 grew quickly, with sales volume over 10,000 units in the second month, reaching 11,042. WEY had little sales impact. The sales volume of VV5/VV6/VV7/P8 was 3,681/5,402/2,328/315 units, respectively.

The total annual sales in 2018 exceeded 1 million, representing a slight decrease of 1.6%

Accumulated sales data for the whole year: Total sales volume in 2018 recorded 1,053,000, representing a slight Y-o-Y decrease of 1.6%. Although it failed to meet the target of 1.16 million units at the beginning of the year, the decline was less than the average decline of 4% in passenger car industry and 2.52% in SUV sub-industry. From details, sales volume of pickup/SUV/sedan of recorded a Y-o-Y increase of 15%/-3.5%/-21%, respectively, to 138,000/905,500/9,491 units. In addition, export sales volume showed a Y-o-Y increase of about 20% to 46,995 units. The company's inventory control is better than that of its counterparts. The inventory coefficient of its brand dealers has dropped from over 2.0 in June/July/August to below 2.0 and down to 1.5, basically reaching the target.

FY2018Q3 below expectations

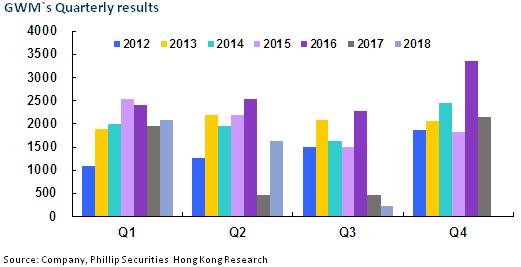

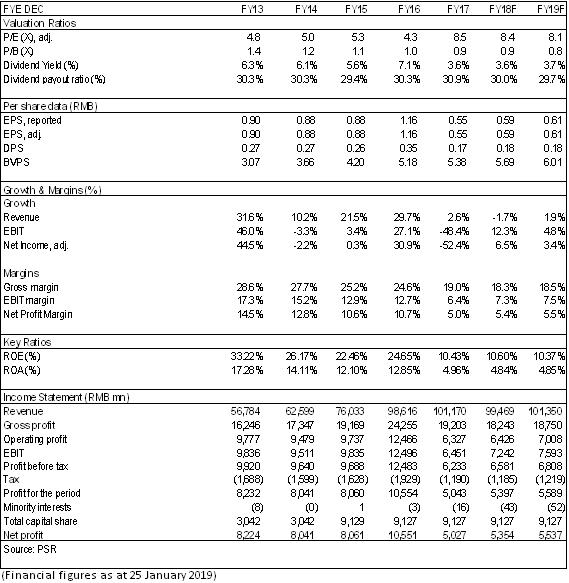

During the first three quarters of 2018, recorded operating revenue of RMB66,645 million, up slightly by 5.1% Y-o-Y, and a net profit attributable to shareholders of RMB3,927 million, up by 36.36% Y-o-Y. Quarterly, due to the downturn of the domestic automobile market and the fierce competition in SUV market, the company's revenue in the first, second and third quarters showed a downward trend quarter by quarter, which was RMB26.57 billion, 22.11 billion and 17,966 million, respectively, representing a Y-o-Y increase of 14%, 23% and a Y-o-Y decrease of 19%. The net attributable profit declined more sharply each quarter, recording RMB2,081 million, 1,615 million and 231 million, respectively, representing a Y-o-Y increase of 65%, 24.7% and a Y-o-Y decrease of 49.8%.

Under the weakening domestic automobile market, especially the increasingly fierce competition in SUV market in its sub-industry, ` promotional activities to expand its sales base have resulted in the loss of profitability of its products. The gross margin in the three quarters was 20.44%,19.24% and 13.65%, respectively. The cumulative gross margin in the first three quarters was 18.23% and the net profit margin was 6.04%, which were basically stable over the same period of last year.

New model F7 is a bright spot in the short term, and the road of medium-term transformation is still tortuous

In the second half of the year, the F-series SUV models of HAVAL with differentiated product orientation came on the market one after another. The appearance, configuration and performance of F5 and F7 are better than those of the old models, and some innovative attempts have been made in marketing and promotion. Especially, the market response of F7 after its launch in November is good. We expect that F7 will further promote the product structure of the company. In the medium term, the company's new energy strategy is still in progress, and new energy versions of its own brand ORA, joint-venture brand Spotlight Automobile and existing models will be launched one after another. We believe that, under the background of the gradual decline of new energy vehicle subsidy policy in China and the increasingly fierce competition, the success of the company's transformation still needs time to test.

Investment Thesis

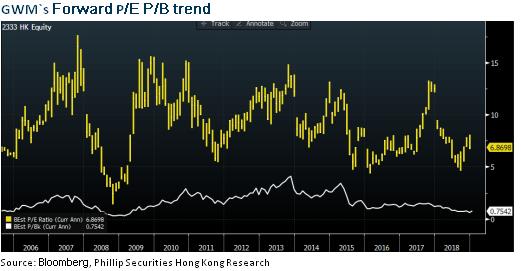

In terms of valuation, we adjust our target price to HK$6.1, equivalent to 9.2/8.9 P/E and 1.0/0.9 P/B ratio in 2018/2019. We maintain the rating of “Accumulate”. (Closing price as at 25 January 2019)

Risk

New vehicle sales fall short of expectations

The SUV market dramatically worsens

The progress of new energy vehicle project is poorer than expectations

�Financials

Click Here for PDF format...