Investment Summary

Sasa's retail and wholesale turnover decreased by 2.8% during Q3 in HK and Macau markets, while same store sales dropped by 3.7%, compared to the increase of 9.6% and 7.1% respectively in Q2. Negative growth was recorded in both retail sales and same store sales in the region in November and December. The total turnover of Sasa during the period recorded a 2.2% decrease, while 9 months ended 31st December 2018 recorded an increase of 9.2%, but missing the whole-year growth target of double digit.

Consumer sentiment in HK and Macau markets remained sluggish due to the weaknesses in RMB exchange rate and stock market under the continued shadow of the Sino-US trade war. In addition, the new E-commerce Law passed by the Chinese government in August 2018 came into force early this year and made Daigou traders more cautious in running their businesses. These all contributed to the sluggish sales performance of Q3. Sasa's sales performance in Q3 underperformed its peers, mainly due to the slowdown in sales of low-margin trendy products due. At the same time, the sales of traditional high-end brands had been ignored. According to the statistics released by the Census and Statistics Department, retail sales in last November recorded only 1.4% increase. The growth rate of medicine and cosmetics category slowed down from 15.2% in October, but still reached 10.1% and continued to outperform other categories.

In HK and Macau markets, Sasa's average sales per transaction of local consumers and mainland tourists decreased by 0.2% and 6.1% y.o.y. respectively which resulted in a 2.6% decline in total. The transaction volume of mainland tourists increased by 5.8% while that of local customers decreased by 5.2%, leading to a slight growth of 0.4% in the overall transaction volume. The decrease of average sales per transaction was reflected on GPM. GPM was continued facing pressure in January and is expected to be below the 40% target for the full year.

Sasa has recently adjusted the commission system and the display of goods, hoping to accelerate the sales of traditional high-end brands. In addition, it will also trengthen promotional efforts to gain more brick-and-mortar customers to partially offset the short-term impact from Daigou reduction. It will also optimise product offerings and launch new products on a timely basis to cater for rapidly changing consumer preferences. According to the information provided by the management team, the sales performance in the first week of January has stabilized. By the end of the month, the overall sales is flat y.o.y. It hopes the sales growth in the next two years to remain in the range of 3 to 10%.

We are still optimistic about Sasa's medium and long-term business development and performance, but expected it will face challenges in the short-term, mainly due to the continued weak market sentiment and the higher base in the fourth quarter of last year . However, the series of cost control measures that it is implementing, including the control of rental costs, is believed to help offset some of the impact on operating profit due to the pressure on GPM.

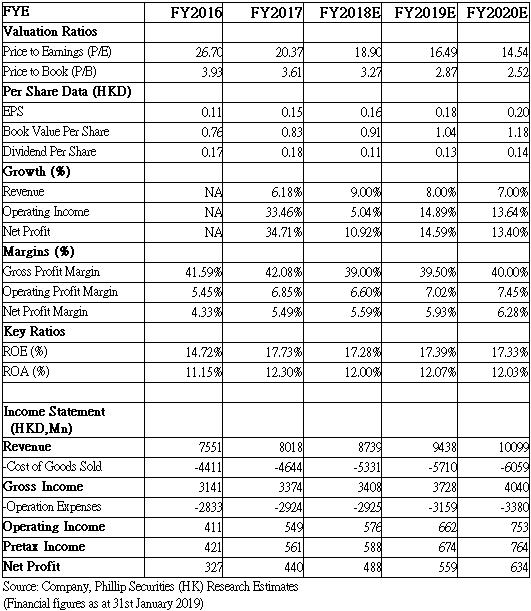

According to the management team, there is still upward pressure on rental rates of shopping malls, but not for shops on streets. If the street shops that have recently renewed their contracts do not have a 10-20% reduction, it will not sign. In addition, it will speed up sales and save storage costs through inventory management and product display, and enhance digitalization and development of information technology to improve operational efficiency and shopping experience. We lower the target price of Sasa to 3.2, the target price-earnings ratio is 20 times(Closing price at 31 January 2019)

Business Overview

Mainland business has found development direction E-commerce platform promotes integration with offline business

Since the launch of the HK Section of the Express Railway Link, Sasa's stores located in the HK West Kowloon station and the neighbouring Tsim Sha Tsui district have been reporting satisfactory sales performance. In contrast, the management team noted that the increased influx of Mainland tourists via the Hong Kong-Zhuhai-Macau Bridge were mainly sightseeing trippers with limited purchasing power and barely contributed to Sasa's overall sales in Hong Kong market. Nevertheless, the team believes the two mega infrastructure projects will attract more mainland travellers with higher consumption when they are gradually consummated.

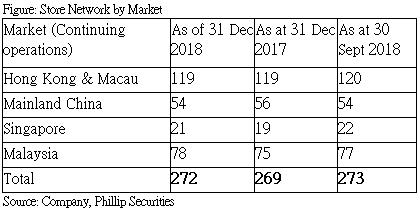

The team remains optimistic towards the outlook of HK and Macau markets in the middle to long run under the favourable development of the Greater Bay Area. It still plans to increase the number of retail outlets in the Greater Bay Area to 180. However, considering the current market conditions, it is cautious of expanding. As of the end of December 2018, it operated a total of 119 retail stores in HK and Macau, 54 in Mainland China, and 272 in total including Singapore and Malaysia.

Sasa's retail and wholesale turnover in other markets outside HK and Macau (including Mainland China, Singapore, Malaysia and E-commerce) increased by 1.3% in Q3. For Mainland business, the management team stated that the current adjustment of the shops and staff is near completion. Compared with the strategy of diversified products in HK, there will be more products targeting mass market. As for the e-commerce business, 90% of the customers are form Mainland. The company will continue to promote the integration of online and offline businesses.

Valuation and Risk

We give Sasa Accumulate rating, the target price-earnings ratio is 20 times, and the target price is lowered to HKD3.2. Potential risks include huge market or currency rate fluctuations that heavily hit consumer sentiments of Chinese tourists and visitors, huge drop of the number Chinese tourists and visitors, and local consumption not as strong as expected. (Closing price at 31 January 2019)

Financials

Click Here for PDF format...