Sectors:

Air, Automobiles (ZhangJing)

Healthcare & TMT (Eurus Zhou)

TMT& Education (Terry Li)

Retail & Property (Tracy Ku)

Automobile & Air (ZhangJing)

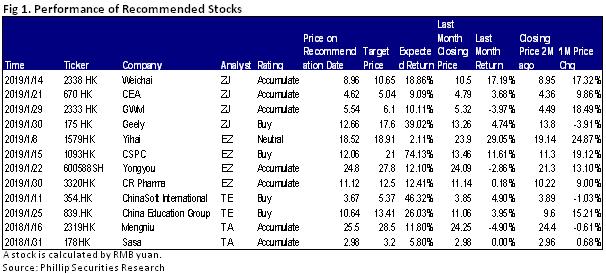

This month I released 4 updated reports of Weichai (2338.HK), China Eastern Airline (670.HK), Great Wall Motor (2333.HK) and Geely (175.HK), which got success by their unique Competitive edge. We prefer Weichai and Geely first.

Weichai's heavy-duty engine has been in a stronger position in heavy truck market, five-ton loader market and the market of passenger vehicles above 11 meters. We expect that the future heavy truck engine business of the Company will continue to benefit from the upward trend in the sales structure resulting from upgrading consumption in heavy truck industry. The Company's "power + hydraulic" strategic framework is clear, which helps smooth the original business affected by periodic fluctuations of heavy truck industry, and the business structure is more balanced. The chairman of the Company also serves as the chairman of Sinotruk, and it is expected that Sinotruk will increase engine purchasing volume of the company in the future.

The sales target for 2019 set by the management of Geely is 1.51 million vehicles, remaining unchanged compared with that of 2018. While the company's efforts to promote new models remain unchanged in 2019. In addition to the upgraded versions of existing models such as new Bo Yue/Emgrand and PHEV versions of existing models, Geely will launch 5-6 types of brand-new models, including two MPV models Jia Ji and VF12, coupe FY11, EV GE11, a brand-new medium SUV "SX12" from BMA platform, and a new model of LYNK&CO. We expect that although the growth rate of car sales of the company is unlikely to repeat the high growth rate of 40-50% in previous years, it is promising that the company enters a new stage of development in terms of model structure, selling price of single vehicles and gross profit growth of single vehicles after this adjustment.

Healthcare & TMT (Eurus Zhou)

This month I released 4 equity reports, including Charmacy (1579HK), CSPC (1093HK), Yongyou (600588HK), and CR Pharma (3320HK). We tend to highly recommend CSPC (1093HK) and CR Pharma (3320HK). CSPC now drops to an attractively low price. Yesterday, the management stated that in 2019E the group's earnings would increase by 20% to 30%, and the sales of NBP products (恩必普產品) would increase by 25% to 30%. Though some drugs still have potential price-cut risks in future GPO, its strong distribution network and technical strengths still support solid growth. For CR Pharma, currently its chemical products are affected by the centralized procurement policy, but this part accounts for a relatively low proportion in the company's topline, thus it is expected to have limited impact. In addition, the company actively acquires new drug distribution rights to underpin future growth. Besides it is going to enhance R&D strength and product reserve in the field of biological medicines. Meanwhile, it cooperates with banks to improve the financial services of its B2B platform, and the revenue of this platform is expected to exceed RMB10bn in 2018. We expect that the business will keep steady growth.

TMT& Education (Terry Li)

I released two reports on ChinaSoft International (354.HK) and China EducationGroup (839.HK). We highly recommend China Education Group. The schools ofthe Group are highly recognized by many institutes, e.g. nseac.com and iResearchChina Alumni Association Network. In the "Chinese University Evaluation ResearchReport in 2019", Jiangxi University of Technology was rated as 6 stars and China's top private universities; Guangdong Baiyun University was also rated as a 3-star and regional first-class private university. Besides, the cost control of the Group also performed well in comparison to the peers. From 2015 to the first half of 2018, the Group's operating profit margin increased steadily, at an average of 40.7%, ranking third, only lower than China Chunlai(1969.HK) and China Xinhua Education (2779.HK). As for the source of funds, In the short term, the Group held cash of RMB 1.907 billion. In the medium term, the Group can raise RMB 2.6-3.2 billion through debt financing in the future. In the long run, the Group will make use of China Education Fund jointly with Value Partners for acquisitions. Thanks to the clear plan on the source of funds, it enhance the certainty of the acquisition in the future. In addition, the management teams are so experienced, where the co-chairs of the Group, Mr. Yu Guo and Mr. Xie Ketao, have been working in the education industry for 24 and 28 years respectively. Jiangxi School and two Guangdong schools have become well-known schools in the region under their leadership. Thus, we believe the Group is able to enhance the value of the acquired schools

Retail & Consuming (Tracy Ku)

This month I released the first coverage report of Mengniu(2319) and Sasa(178).

On 23rd December, China Shengmu Organic Milk (1432) announced to sell to Inner Mongolia Mengniu 26.67% interest in the Target Company, and Shengmu High-tech agreed to sell to Inner Mongolia Mengniu 24.33% interest in the Target Company. Upon the completion of the share purchase agreement, Inner Mongolia Mengniu will hold 51% interest in the Target Company, and is expected to be recognized as a subsidiary of Inner Mongolia Mengniu in its consolidated financial statements.

Shengmu is the largest organic dairy company in China with the largest herd of organic dairy cows nationwide. It is the only vertically integrated organic dairy company in China that meets E.U. organic standards. It is the only dairy company in China that offers branded organic dairy products that are 100% processed from raw milk produced by self-owned certified organic dairy farms.

The target company recorded losses before taxation of RMB68.44 million and RMB1194.92million respectively in 2016 and 2017, and losses after taxation of RMB76.99million and RMB1185.44million. Shengmu has announced profit warning expecting to record a loss for the year ending 31 December 2018. Because of the impairment provisions made for trade receivables and other receivables, its total profit for the year ending 31 December 2018 is expected to be decreased by approximately RMB1.06 billion. However, if we only look at the liquid milk product business, the revenue in 1H of last year was RMB480 million, which accounted for only 1.4% of Mengniu's revenue in the same period.

We believe that the acquisition may bring slight pressure on Mengniu's short-term performance. In the medium and long term, it will not only provide Mengniu with a stable supply of raw milk, especially the organic raw milk supply, it will also enrich Mengniu's product categories in the end market, that can provide growth drivers for revenue.

Click Here for PDF format...