Investment Summary

In 2018, the total external contracts signed increased by 12.4% yoy. Railway orders with high profit margin increased significantly, which is expected to improve overall profitability. With the rising domestic capital investment and municipal bond issuance, the infrastructure industry is facing a favorable policy environment. We maintain our target price of HK$7.1, Accumulate rating. (Closing price at 12 Feb 2019)

Company Business

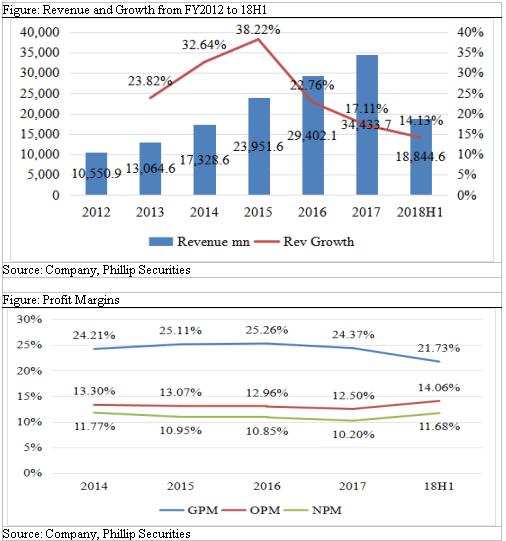

In 2018, the total external contracts signed increased notably. Totally external contracts of RMB68.29bn has been signed, an increase of 12.4% compared with that in 2017. In terms of segments, railway orders amounted to RMB25.08bn, rising by 44.8% yoy. Urban transit contracts amounted to RMB11.61bn, climbing by 6.4% yoy, among which the amount of metro contracts newly signed was 11.6bn, an increase of 20.2% yoy. Overseas orders reached RMB0.95bn, declining by 64.8% yoy. General construction contracting and other business contributed to contract sales of RMB29.85bn, a yoy increase of 0.3%.

Optimizing business structure and improving profit margins. Although the growth of external contracts signed in 2018 (12.4%) is lower than that in 2017 (22.7%), the structure of business has been improved dramatically. Railway orders with high gross profit margin has increased significantly, while the general construction contracting business with low GPM has remained stable with contracting proportion. The optimized business structure will help to improve overall profitability.

Accelerated national infrastructure investment and municipal bond issuance. In 2018, the national railway fixed asset investment reached RMB802.8bn, 9.7% higher than the target of RMB732bn at the beginning of 2018. It is expected that the railway investment will reach RMB850bn in 2019E. Besides, according to Wind, just in Jan 2019, China's newly issued municipal bond reached RMB417.96bn, exceeding the total amount in 18Q4. Funds will be used in material industries including infrastructure. Meanwhile, we see that the market share of CRSC's railway business has always maintained above 60%, and that of urban transit business has remained around 40%, keeping a leading position in industry. CRSC is expected to achieve good performance in a favorable external environment.

Valuation and Risks

We give target price of HK$7.10. We forecast revenue growth of 15.54%/ 18.46% and EPS of RMB0.42/0.57 in 2018E/19E. Giving a target price-earnings ratio of 11 times, we get the target price of HK$7.10 for 2019E. Risks include: Growth of railway investment fail expectations; Fierce competition in urban rail market leads to bidding failure; Profitability level fail expectations.

Financials

Click Here for PDF format...