Investment Summary

Although this winter is "not too cold", the sales growth of branded down apparel under Bosideng has accelerated since last December. The management team has raised its whole-year revenue growth guidance of branded down apparel business under Bosideng from 20%-30% to over 35%, other business still maintains, i.e. OEM management business is more than 20%, ladieswear business is medium to high, diversified apparels business will continue to shrink as its new strategic principle is focusing on principal business and key brands while implementing de-diversification.

During the first nine months of FY2018/19, the accumulated retail sales of down apparel products under the core brand-Bosideng increased by more than 30% y.o.y. which is higher than 24.1% in 1H. This means that the growth rate in Q3 has accelerated. According to the management team, the weather was still warm during October to November, thus this business recorded an increase of only 20 to 30%. However, the weather began to turn cold in December, with an increase of more than 50%. It is expected to continue to maintain rapid growth before the coming Luna New Year.

The business showed both prices and sales recorded growth in Q3, and management expects the trend will continue in 2019. The business is currently being transformed from the mass market to the mid-to-high end. The current ASP of the products is about RMB1,200-1,500, which is still quite far from its overseas competitors such as Canada Goose of Canada. The management team's goal is to raise the ASP of 20 to 30% per year in the coming three to five years.

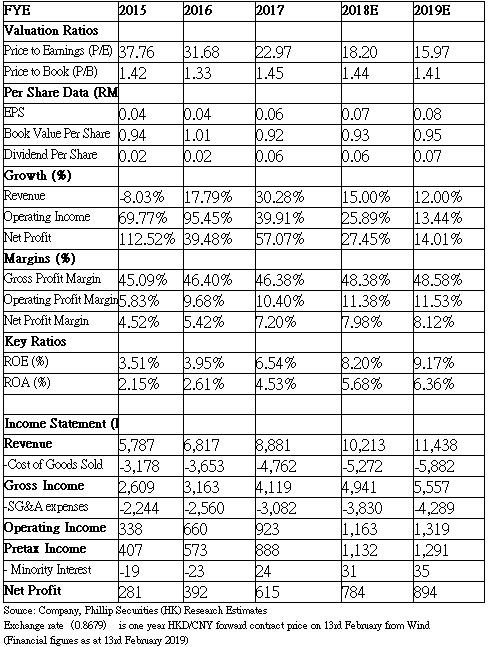

We are optimistic about the company's ability to raise ASP in the medium and long term. The improvement of its product design, branding and channels will be the drivers of sales volume. We expect the overall revenue to maintain a high-speed growth momentum, and GPM will also have room to improve further. We give accumulate rating, target price-earnings ratio 20 times, with target price HKD1.7. (current price as of February 13, 2019)

Business Overview

2018 financial year interim results review

Interim revenue as of the end of September 2018 increased by 16.4% y.o.y. to RMB3.444 billion. The brand down apparel business which shared 51.5% of the total revenue, its revenue increased by 19.5% y.o.y. Brand Bosideng, which accounted for 84.6% of the down apparel business, got the strongest performance, with revenue growth of 24.1%. Revenues of brand Snow Flying and Bengen were up 17.5% and down 2.9% respectively. These two brands as the defensive business for the company, has been close to the inventory clearance in 1H of 2018.

During the period, GPM increased by 2.2 ppt y.o.y. to 42.3%, mainly driven by a sharp increase of 7.9 ppt to 50.6% of GMP for the down apparel business.

The reasons for the increase included the proportion of new products in the down apparel business product mix increasing significantly, that driving up the ASP. In terms of raw material costs, the company locks the purchase price with the upstream suppliers in advance, accounting for 50 to 60% of the total purchase of raw materials. The remaining 30 to 40% will be procured according to the current market price to maintain the stability of the overall raw material procurement cost.

The OEM business was affected by the wage and cost pressures in the Mainland, and GMP of the business fell slightly to 17.7%.

During the period, distribution expenses increased by 18.4% y.o.y. accounted for 22.9% of the total revenue, representing an increase of 0.3ppt y.o.y. The increase was mainly due to the company's effort in brand building and channel optimization for the branded down apparel business. The increase of advertising expenses is expected to continue in 2H.

We expect that the growth rate of brand down apparel business in 2H will grow faster than 1H, and the improvement of GPM for the whole year will be further expanded to offset the impact of the increase in distribution expenses on operation profit margin.

Promote business reforms Down apparel business to high-end fashion

2018 was Bosideng's reforming year. During the year, the company cooperated with many internationally renowned designers in launching crossover down apparel collections that feature trendsetting designs and functionality. It also joined New York Fashion Week in last September. There were also innovations in product design, such as puff collection, which is made of high fill power large-size goose down cluster with 90% down content to make it lighter and warmer. The high-end outdoor collection uses GORE-TEX, which is waterproof, windproof and breathable.

According to the management, the total budget for branding in FY2018 is RMB500 million. It plans to further increase the budget in 2019 with further expansion of the designer team to attract more high-end designers. It also plans to continue its branding campaign like participating in international fashion show, promotion on social networking platforms, and hiring A-list stars as brand representatives.

In terms of channels, the company's involvement in channels such as shopping malls and department stores has increased significantly, while the terminal efficiency has greatly enhance through a number of flexible measures including shutting down underperforming stores, renovation of point of sales terminals.

During 1H of FY2018, its self-operated retail outlets (net) increased by 146 to 1569, and the retail outlets operated by third party distributors (net) decreased by 53 to 2990.

In terms of regional market development, the company intends to further expand in the eastern China and central China regions where with stronger consumption power. As of the end of September 2018, it had 1,687 retail outlets in eastern China, a significant increase of 88 from the end of March. The retail outlets in central China also increased by 33 to 1040, while in northeast China, northwest China and southwest China where with weak consumption power, the number of retail outlets have all decreased.

New OEM business capacity in Southeast Asia

OEM management business is the company's second largest business. With an increase of 63.5% in 1H of FY18, it accounts for 32.1% of the total revenue. According to the management, entering 2H, the growth trend has started slowing down. The guidance of the whole-year growth is more than 20%, and same for FY2019. In the future, it will continue to find suitable new capacity in Southeast Asia.

The management also mentioned that the brand Bosideng is a Chinese national brand and will still adhere to “Made in China” and leave its production capacity in China. It plans to build a large-scale down jacket production base in Henan. The factory will contain artificial intelligence elements. Currently, many of its products require high-end materials and processes, so the production cost in China is comparable that of overseas.

Ladieswear business is the company's third largest business, its revenue in 1H grew by 6.6% y.o.y. The reform of the business began in April and August last year. The related cost has mostly reflected in the financial performance of 1H. According to the management team, this business is less sensitive to the macroeconomic environment, and the ASP of winter products is higher than that of summer. It expect that the whole-year revenue growth will be higher than 1H.

The company has no further M&A plan for this business. It will rather focus on the development of current brands, i.e. Jessie, Buou Buou, Koreano and Klova to enhance the synergy effects. It expect the work will need to take about 2 to 3 years to complete.

Increase in the proportion of e-commerce business 2019 add new design team

Interim revenue of diversified apparels business decreased significantly by 91.1% y.o.y, leading to a decrease as a percentage of the company's total revenue to 0.8%. According to the management team, only the school uniform business will be fully retained. Children's wear business has undergone a major contraction in 1H. In 2H, the company has start agent business through e-commerce business. But it still needs time to see the results. Bosideng Man business has also shrunk significantly. The company is currently clear its inventory.

Due to the significant decrease in diversified apparels business, revenue of online sales business decreased by 12.6% y.o.y. to RMB178.3 million. Among which, revenue from the online sales of branded down apparel business and ladieswear business increased 73.4% and 21.8%, accounting for 7.8% and 6.2% of the respective business. We expect that as online business maintains a high growth rate, the percentage share will also increase further.

According to the management, the strategy of online sales in 2018 is that same product with same price as offline channels. In 2019, there will be a design team that specifically design products for online channels. On 11th November 2018, the company ranked the second in the Tmall platform's full-category brand ranking. On 12th December 2018, its revenue of branded down apparel business on Tmall platform increased significantly by 165%, on all channels increased by 145%.

Investment Thesis & Valuation

We give accumulate rating, target price-earnings ratio 20 times, with target price HKD1.7. Potential investment risks include revenue growth or channel expansion missing expectation, raw material cost with huge volatility. (current price as of February 13, 2019)

�Financials

Click Here for PDF format...