GAC Toyota Surge 75% YOY in the First Month, Surpassing GAC Honda

According to data released by GAC recently, in the first month of 2019, the total sales of GAC reached 210,000 units, a slight decrease of 0.21% yoy. Among them, the seals of joint venture brand GAC Honda were 74,000 units, a decrease of 2% yoy; sales of GAC Toyota were 80,000 vehicles, an increase of 75% yoy; GAC Toyota's monthly sales volume exceed GAC Honda's, showing its strength matching its global ranking.

The sales volume of other brands is less. The sales volume of GAC Fiat was 9,000 units, a decrease of 32% yoy; and the sales volume of GAC Mitsubishi was 12,000 units, a decrease of 23% yoy. The sales volume of Trumpchi, a self-owned brand, was 34,000 units, a decrease of 45% yoy.

In the whole year of 2018, GAC realized sales of 2,147,900 units, an increase of 7.3% yoy. The sales volume of GAC Honda, GAC Toyota, GAC Fiat, GAC Mitsubishi and GAC self-owned brands were 741,400, 580,000, 125,000, 144,000 and 535,000 units, respectively, with an increase of 5.2%, 31%, -39%, 23% and 5.2% yoy, respectively.

Huge Matthew Effect

With the powerful new product matrix and the marketing strategies in recent years, GAC Toyota's monthly sales volume have increased against the trend, and the growth momentum is rapid: in 2018, the annual sales volume of the eighth generation of Camry, Levin and YARiS L increased 97%, 21% and 12% to 158,800, 202,700 and 67,000 units, respectively. The sales volume of Highlander exceeds 100,000 units. The market share of medium and large-sized SUVs ranks first. In the first month of 2019, Camry, Levin and YARiS L of the eighth generation set new monthly sales records, reaching 19,700, 26,700 and 15,000 units, respectively, with the increase of 70%, 90% and 58%, respectively. In addition, the sales volume of brand-new Highlander was about 10,500 units, of which the sales volume of vehicles with a price of RMB300,000 account for 80%.

GAC Honda has achieved remarkable performance with three blockbuster models: the 10th Generation Accord, the New Generation Crider, and the Fit. In the first month of 2019, the terminal sales volume of the 10th generation Accord (ACCORD) was 23,649 units, with an increase of 24.9% yoy and 16% yoy on shipment. The terminal sales volume of the new generation Crider is 14,688, with an increase of 46% yoy and 31.1% yoy on shipment. The terminal sales volume of FITis 11,545 vehicles, with an increase of 44.1% yoy 66.5% yoy on shipment.

In 2019, GAC Toyota and GAC Honda have their own popular models to be launched. In addition to the new energy version of existing models and vertical replacement models, the same model of CRV of GAC Honda expected by people and RAV4 of GAC Toyota will also be launched.

GAC Has Been Reducing Stock of Self-owned Brands and the Sales of GAC Fiat Are Still Weak

In 2018, affected by the product line's over-concentration on SUV and product iteration, the growth rate of the sales of GAC's self-owned brand Trumpchi dropped from double digits to single digit. In order to alleviate the inventory pressure of distributors, the company took the initiative to reduce the wholesale sales of Trumpchi in the first month of 2019, resulting in a 45% decline in wholesale sales, and the actual terminal sales volume still increased by 45% yoy to 56,000 units. However, channel inventory pressure has not been eased. Trumpchi's sales growth in the coming months will still be under pressure. In terms of new models, in addition to GM6, which was launched in January 2019, Trumpchi will launch news models such as a new generation of GS4 and GA6, mid-term modified GS8, and new energy vehicles such as AionS.

In 2018, with the addition of new medium-sized SUV with 7 seats, there are 4 domestic models of GAC FCA Jeep, covering the mainstream price range of RMB130,000-400,000, but the slowdown in the SUV market has affected sales performance. According to the original five-year plan, Jeep will launch four plug-in hybrid electric models, four pure electric models and eight new traditional fuel vehicles in 2022. The subsequent launch of new models is still worthy of attention..

Investment Thesis

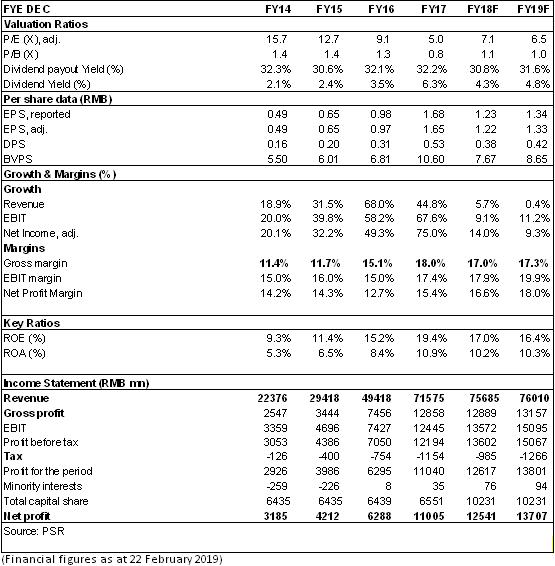

It is expected that the Company will maintain steady growth in the future under the strong product cycle of the Japanese-brand JV. We revised the Company's 2018/2019 earnings forecast. We reaffirm the "Accumulate" rating with the target price to HKD 11.3, equivalent to 8.1/7.4x P/E ratio in2018/2019. (Closing price as at 22 Feb 2019)

Financials

Click Here for PDF format...