|

|

|

*Advertisement* |

|

|

|

|

|

7 Mar, 2019 (Thursday) |

CEB GREENTECH(1257)

Analysis:

China Everbright Greentech (1257) is principally engaged in the businesses of integrated biomass utilization, hazardous and solid waste treatment, solar energy and wind power. In 2018, the Group further broadened the scope of its business by tapping the environmental remediation business. For the year ended 31 December 2018, the Group recorded revenue of HK$7 billion, representing an increase of 53% as compared to the same period in 2017. Profit attributable to shareholders increased by 39% to HK$1.32 billion. During the year under review, a record-high number of new projects were launched, as the Group secured 24 new projects and entered into 2 share transfer agreements for the acquisition of 2 environmental protection companies. (I do not hold the above stock)

Strategy:

Buy-in Price: $6.50, Target Price: $7.30, Cut Loss Price: $6.10

|

|

SUNEVISION(1686)

Analysis:

The Group announced its interim results on February 22, and its revenue reached HK$760 million during the period, up 18.5% YoY. However, the gross profit margin decreased from 59.3% to 57.2%, due mainly to the increase in depreciation expenses and the upfront expenses of new customers entering MEGA Plus and MEGA Two. In addition, operating costs as % of revenue also increased, with selling expenses accounting for 1.86%, up 0.05% YoY; administrative expenses as % of revenue was 4.5%, increased by 0.2% YoY. The increase was mainly used to promote new capacity in data centers. The Group announced on December 12 that it had successfully acquired the Tseung Kwan O Data Center site for HK$5.46 billion and stated that the Tseung Kwan O project will be funded from internal and external resources. In this interim results, the group updated that it has obtained two loans from Sun Hung Kai Properties Group and banks, respectively, amounting to HK$3.8 billion and HK$2.18 billion, totaling HK$5.98 billion.

Strategy:

Buy-in Price: $5.80, Target Price: $6.80, Cut Loss Price: $4.50

|

| |

|

Anta Sports (2020.HK) - FY18 Results Beyond Market Expectations; Conservatively Optimistic Guidance for FY19

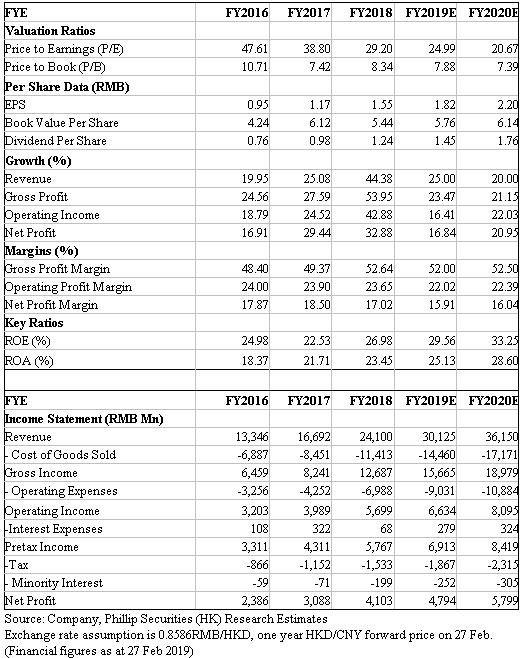

Investment SummaryAnta reported 2018 operating results beating market expectation. Anta brand realized mid-teens growth and non-Anta brand delivered yoy growth between 80% to 85%. Benefiting from rising same store sales and operation efficiency, we expect the turnover to stably grow in future. In 2019, it targets to deliver over 20% topline growth. We estimate 19E/20E EPS to be RMB1.82/2.20 respectively, and raise TP to HKD50.8, Accumulating rating. (Closing price at 27 Feb 2019) Company Business2018 results beating expectations. Anta's revenue rose by 44% to RMB24.1bn. GPM rose by 3.3ppts reaching 52.6%, but OPM declined by 0.2ppts to 23.7%, due to climbing selling expenses. Net profit attributable reaching RMB4.1bn, up by 33%. Net operating cash flow grew by 40% to RMB4.44bn. Dividend pay-out ratio dropped from 70% in 2017 to 45% in 2018.

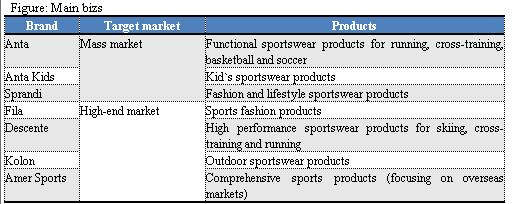

Improving store sales and efficiency. As up to the end of 2018, the amount of Anta/ non-Anta stores reached 10,057/1,652 respectively, exceeding previous guidance ( Anta 9700-9800, Fila 14000-15000). Meanwhile, we see that same stores sales growth served as one main driver, given Anta/ Anta Kids delivering monthly sales of RMB220k/ 130k per single store (by 10% yoy), and Fila /Fila Kids recording sales of RMB700k/ 300k (up by 40%/ 50% yoy). Currently inventory level is getting better, with inventory days of key biz Anta maintained at around 4.2 months, and Fila's inventory days dropping from 150 days to 130 days. Improving efficiency is expected to go on to contribute to steady sales growth. 2019 guidance. The company aims to realize sales growth of 20% in 2019E, with Anta and Fila respectively growing by min-teens and 30%. As up tp 2020, the total turnover CAGR is targeted to be 15%~20%. For other bizs, Descent is going to actively explore and strive for turning profit in 2019E. While other new brands like Amer Sports and Kolon still contribute little to sales and profit.

Acquisition progress smoothly. The company announced that the acquisition of Amer Sports have been approved in related national regulations globally. The trade will be sellted in March. We highlight this transaction is an important step in Anta's exploration in overseas market. Valuation & RisksWe raise target price to HKD50.8: Future momentum comes from rising store efficiency, rapid growth of Kids` product and further exploration of Fila and its subsidy bizs. Projected EPS is RMB1.82/2.20 in 19E/ 20E and target price is raised to HKD50.8. Risks include: Rising selling and R&D expenses; Sluggish retail market; Inefficiency resulting from so many brands under operation.

Financials

Click Here for PDF format...

| Recommendation on 7-3-2019 | | Recommendation | Accumulate | | Price on Recommendation Date | $ 45.400 | | Suggested purchase price | N/A | | Target Price | $ 50.800 |

| |

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the “Group”) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products’ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

版權所有, 翻印必究。

Copyright(C) 2019 Phillip Securities (HK) Ltd. All Rights Reserved.

|