Investment Summary

Travelsky Technology is the largest provider of the aviation information systems in China, which developed systems, such as flight control, air ticket distribution, check-in, boarding and load planning, accounting, settlement and clearing system, and aviation logistic. Based on DCF valuation, we derived a target price of HK$27.18, implied a P/E of 27.6x and 24.4x in 2018/19F. We initiate a “accumulate” rating with a 17.7% potential upside. (Closing price at 6 Mar 2019)

With a steady growth in transport volume and number of airports, there was still room for aviation information system to grow

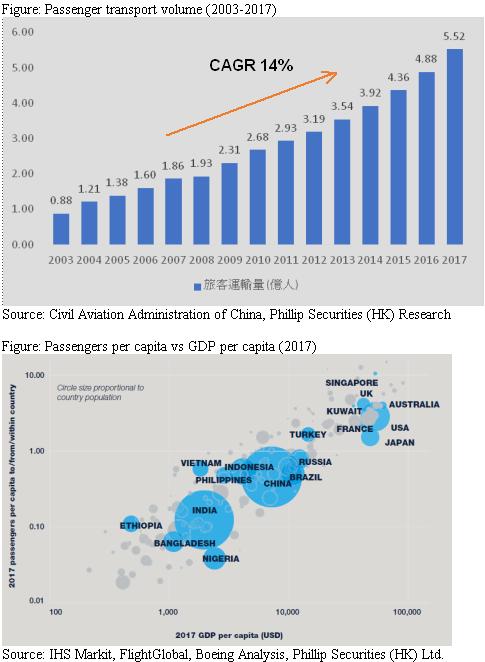

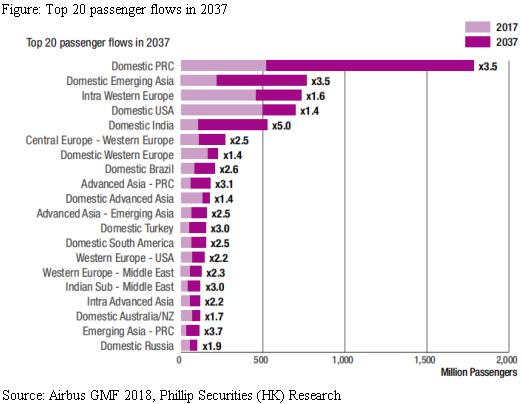

The traffic volume of civil aviation has been increasing steadily since 2003. According to Civil Aviation Administration of China, the transport turnover of civil aviation has been growing at a CAGR of 14%, reaching 10.83 billion km in 2017. As for the demand from tourism, growing steadily since 2003, the passenger transport volume has increased from 88 million in 2003 to 552 million in 2017, representing a CAGR of 14%. The Airbus forecasts that the flight per capita in China will be up from 0.41 in 2017 to 1.40 in 2037, implying a CAGR of 6.3% for the next 20 years. Moreover, the number of passenger for the domestic flight in China in 2037 will be 3.5 times that in 2017, which will also be the region with the largest number of passengers in the next 20 years, meaning a CAGR of 6.4% for the next 20 years.

Meanwhile, according to the forecast from Boeing, the CAGR from 2018 to 2037 on air cargo in domestic China will be 6.3%, which is the fastest growing region. Besides, according to “Outline of the 13th Five-Year Plan for the Development of Civil Aviation”, Chinese government targets the transport volume, the passenger transport volume and the freight transport volume to reach 142 billion, 720 million, and 8.5 million ton respectively, representing a growth of 10.8%, 10.4% and 6.2%.

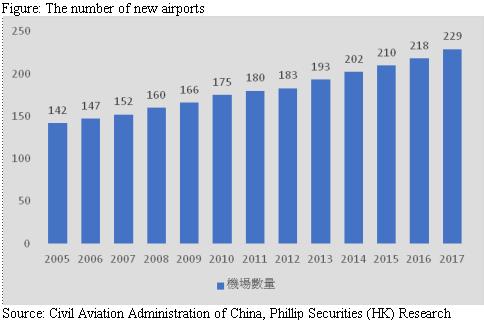

Apart from the target, it also mentions the number of civil transport airports to be around 260 in 2020, implying 10.3 new airports from the next three years, higher than the average of the past 12 years.

Monopolized industry with price restriction

The Group was the only aviation information system provider in China. The domestic airlines in China have all adopted the ICS, CRS and APP of the Group, except Spring Airline and 9 Air. Although there are no clear-cut policies stating that the Group was the only aviation information system provider, the domestic airlines are prohibited to use the foreign GDS, leading to the monopoly in the industry.

The maximum guidance price of “flight control system services” and “electronic travel distribution system services” are progressive per segment, ranging from RMB 4.5 to RMB 6.5 for domestic flights and RMB 6.5 to RMB 7 for international flights.

Owned by different airline clients

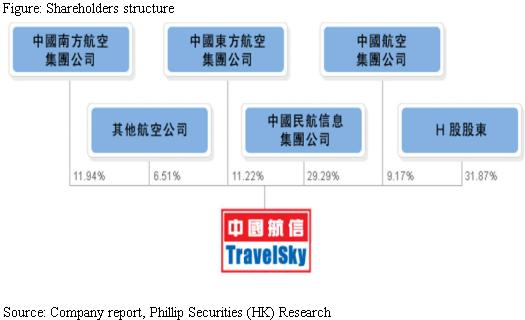

Air China, China Eastern and China Southern held 9.17%, 11.22% and 11.94% of the shares respectively, for a total of 32.33%, while other airlines also held 6.51% of the shares. Being the shareholder of the Group, the interest of the airlines is bonded with the Group, which reduces their incentive for breaking the Group's monopoly, but also forces the Group to provide better services.

Business Overview

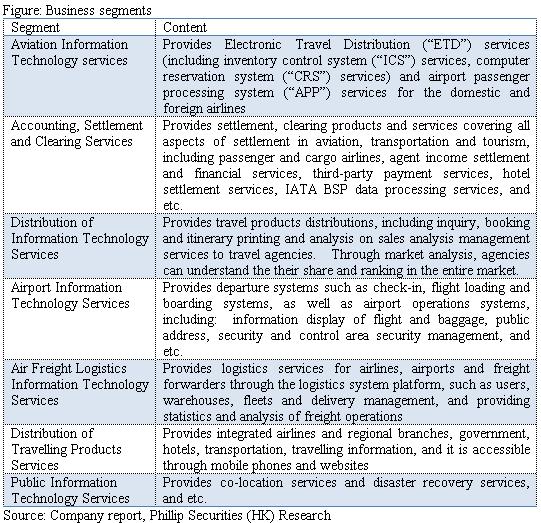

The Group is the largest provider of the aviation information systems in China, which developed systems, such as flight control, air ticket distribution, check-in, boarding and load planning, accounting, settlement and clearing system, and aviation logistic. And, Clients include airlines, airports, travel suppliers, travel agencies, freight forwarders, IATA and other large international organizations and governments. The business of the Group is classified as seven segments: 1. Aviation Information Technology services, 2. Accounting, Settlement and Clearing Services, 3. Distribution of Information Technology Services, 4. Airport Information Technology Services, 5. Air Freight Logistics Information Technology Services, 6. Public Information Technology Services, and 7. Infrastructure.

The revenue is instead classified as four segments, 1. Aviation Information Technology Service, 2. Accounting, Settlement and Clearing Services, 3. System Integration Service and 4. Data Network Revenue and Other.

1. Aviation Information Technology Service

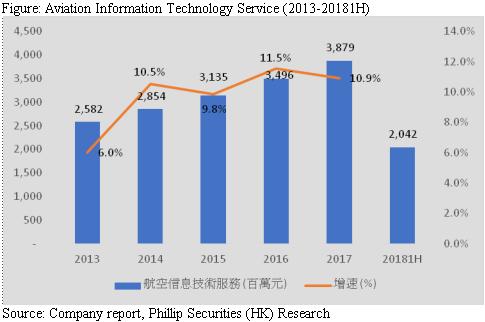

This segment accounted for 58% of the total revenue in 2017, reaching RMB 3.88 billion, increased by 10.9% YoY. In the first half of 2018, the revenue from this segment was RMB 2.04 billion, up 7.5% YoY. The revenue segment mainly corresponds to Aviation Information Technology services in the above business segment. Whenever the ticket is generated, distributed and used through the Inventory Control System, Computer Reservation System and Airport Passenger Processing System (APP) of the Group, the airline will be charged system processing fee based on the amount of processed volume. For domestic airlines, the fee will be provided a volume discount based on the usage, so this revenue growth rate will be slightly lower than the system processed volume growth rate.

2. Accounting, Settlement and Clearing Services

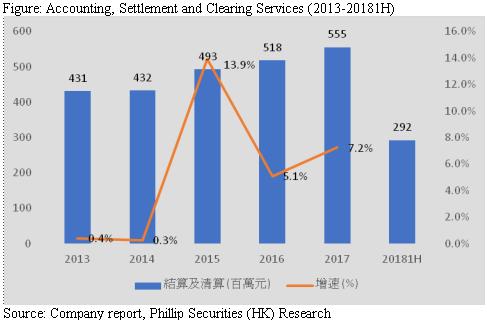

Accounted for 8% of the total revenue, the revenue from this segment was RMB 560 million in 2017, increased by 7.2% YoY. The revenue reached RMB 290 million, up 7.4% YoY. This segment mainly corresponds to Accounting, Settlement and Clearing Services in the above business content, where its revenue is related to the amount and number of the ticket including not only passenger, but also air cargo and mail. The Group will receive a portion of the amount of the ticket as the fee. Unless the amount of the ticket fluctuates, the revenue from the segment will generally follow the growth of the system processed volume. In addition, there is part of the revenue generated from system upgrade, so the revenue from this segment will be a bit volatile.

1. System Integration Service

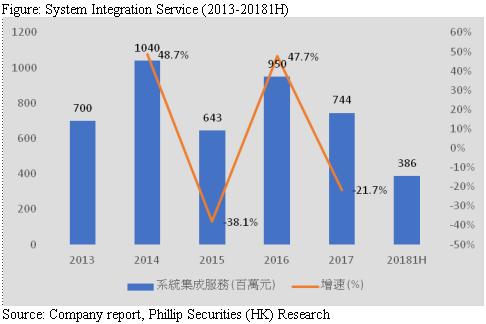

Dropped by 21.7% YoY, its revenue was RMB 740 million in 2017, accounted for 11% of the total revenue. The revenue increased by 67.4% YoY in the first half of 2018, reaching RMB 390 million. This revenue comes from hardware, software and data integration services provided by the Group to airports, commercial airlines and other institutional clients. Since the revenue is determined by the number of projects the group has held, it is highly volatile. In addition, revenue recognition is based on the progress of the construction period.

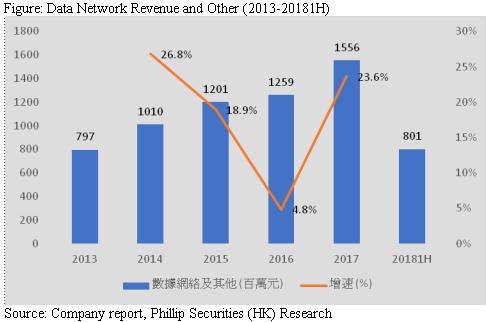

2. Data Network Revenue and Other

This revenue was RMB 1.56 billion in 2017, accounted for 23% of total revenue, up approximately 23.6% YoY. In the first half of 2018, the revenue was approximately RMB 800 million, a YoY increase of 11.1%. It is mainly from the distribution of information technology services to travel agencies, the distribution of travelling products services to travel suppliers, the air freight logistics information technology services to airlines, airports and freight forwarders, the airport information technology services as well as the public information technology services. Once the travel agent purchase air ticket and travelling products that are distributed by the Group, they have to purchase through the group's distribution system terminals. Therefore, the income is mainly driven the growth rate of the travel agencies. There are two types of charges, which are first based on account or traffic charges.

Industry Overview

Business model

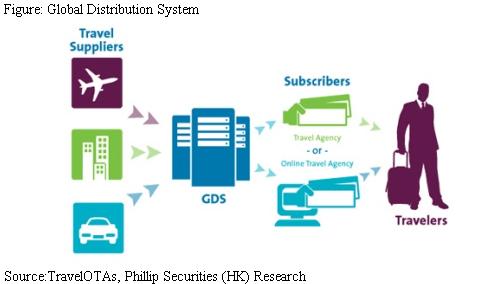

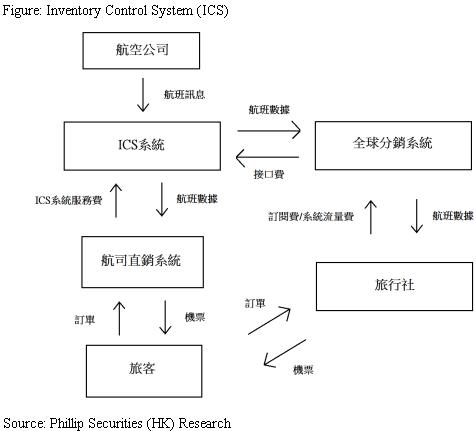

The main business of the Group is to operate and promote its Global Distribution System (GDS). GDS is a system that connects different travel suppliers and travel agencies. Through the system, travel agencies are able to inquiry, reserve and issue the travelling products, providing a full set of travelling products and services.

Industry outlook

As the demand for aviation information systems is mainly driven by the development of the civil aviation industry, we understand the demand of the aviation information system industry by analyzing the civil aviation industry.

Civil aviation industry in China has been steadily developing since 2003. The transport volume of civil aviation is generally measured by the amount of transport turnover, which is obtained by multiplying the transport volume by the average transport distance, also taking both the cargo turnover and the passenger turnover into account. According to the Civil Aviation Administration of China, the transport turnover of civil aviation has been growing at a CAGR of 14%, reaching 10.83 billion km in 2017. It even recorded a positive growth in 2008, showing that the civil aviation industry is quite stable.

Since the demand of civil aviation comes from both tourism and freight, we will analyze these two aspects separately. In terms of demand from tourism, the passenger transport volume has been increasing steadily, increased from 88 million in 2003 to 552 million in 2017, representing a CAGR of 14%.

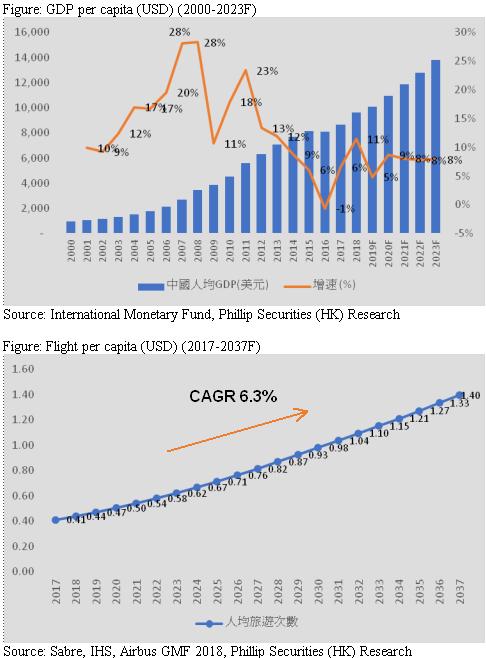

For future demand, according to Boeing research, the flight per capita is positively related to the GDP per capita. In other words, when the citizens of a country become richer, the flight per capita will also increase. International Monetary Fund predicted the 2019-2023 CAGR of GDP per capita in China to be 7.4%, and to reach USD 13,780. And, according to Airbus analysis, the flight per capita in China will increase from 0.41 in 2017 to 1.40 in 2037, with a CAGR of 6.3% in 20 years. Moreover, the number of passenger for the domestic flight in China in 2037 will be 3.5 times that in 2017, which will also be the region with the largest number of passengers in the next 20 years, meaning a CAGR of 6.4% for the next 20 years.

For demand from freight, the freight transport volume also showed an upward trend, reaching 7.06 million tons in 2017, with a CAGR of 8.7%, which is lower than the growth rate of passenger. However, compared with the demand from tourism, that from freight is relatively volatile, and recorded a negative growth in 2011 and 2012.

Boeing forecasts the CAGR from 2018 to 2037 on air cargo in domestic China will be 6.3%, which is the fastest growing region. The rapid growth is attributed to the robust growth of the economy in China and the rise of the middle class. However, the recent conflict between US and China may impose an uncertainty to the freight in short term.

Besides, according to “Outline of the 13th Five-Year Plan for the Development of Civil Aviation”, Chinese government targets the transport volume, the passenger transport volume and the freight transport volume to reach 142 billion, 720 million, and 8.5 million ton respectively, representing a growth of 10.8%, 10.4% and 6.2%.

Generally, as the economy in China is boosting, we believe that the demand from tourism and freight will continue to grow, which will create a stable demand to aviation information systems.

Apart from the demand from civil aviation, the number of new airports has also created new demand to aviation information systems, as a new airports need to install different systems, such as departure system, light and baggage information systems, public broadcasting systems and security control zone systems and so on. As of 2017, there were 229 certified airports, increased 87 within 12 years, representing an with average of 7.25 new airports per year. The outline mentioned the number of civil transport airports to be around 260 in 2020, implying 10.3 new airports from the next three years, higher than the average of the past 12 years.

In conclusion, we believe that there is still room for aviation information systems to grow as transport volume and number of airports continue to rise.

Industry characteristic

1. Long development cycle with large expenditures

Due to the complexity of the aviation information systems which need to support multiple functions, such as flight control, ticket distribution, check-in, loading, settlement and clearing, the development cycle is relatively long with high expenditure is high. There are four procedures for setting up a system. First, you need to define the system, for example, consider what functions the system needs to provide and how feasibility the functions are. Then, you need to develop the system and consider how to implement the required functions. The system needs to be designed and implemented through programming. System implementation will then be carried out, including setup, system installation and system migration and personnel training. Finally, the system will be run and maintained. When the system starts operations, it needs to be maintained and evaluated frequently to see if the system needs to be modified.

In addition to the long development cycle, expenditure for system development is also high. The construction of information systems is a highly intellectual and labor-intensive work. The proportion of easy work is very small, so the expenditure is relatively high.

Due to the long development cycle and high expenditure, the entry barrier of the industry is also high.

2. High switching cost

The operation of airlines relies heavily on the aviation information system, so their migration risk is relatively higher than other industries. In addition, employees are already familiar with the original system operation, and the cost of retraining is also high. For example, the instructions of Global Distribution System (GDS) in the aviation information system is made up of its own language. If the system is replaced, employees need to relearn the new language, which may reduce operational efficiency, so the most of the airlines have a higher switching cost.

3. Low marginal cost amplifies the advantages from scale

For distribution systems like GDS, their marginal cost is low, because the cost of new services for each additional user is low. Users only need to install GDS in their terminal in order to enjoy the services. Low marginal cost makes the advantages from economies of scales more prominent, so it favors the current leader the most, making the industry more inclined to monopoly.

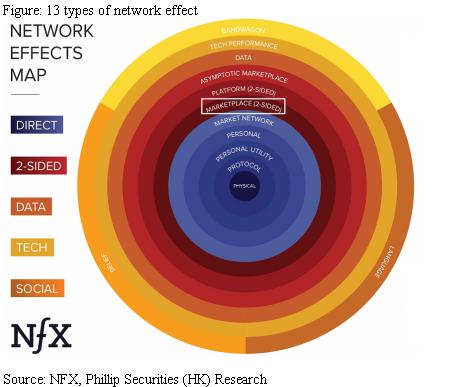

4. Network effect

The network effect means that the value of the product increases with the increase in the number of consumers who purchase the product and its compatible products. This is the characteristic of GDS in the aviation information system. A foreign venture capital fund has divides the network effect into 13 categories, and GDS was classified as a 2-sided marketplace. This type of network effect is characterized by two different types of users: the supply side and the demand side users, and provide each other with value. Each new supply-side user in the this network can directly increase the value of the demand-side user, and vice versa, and form a virtuous circle. Take GDS as an example, when the number of airline, hotel or car rental company (supply-side users) increase, the number of travel products that the tourist agents (demand-side users) can choose will rise, and thus enhancing the value. This helps attract more tourist agents to adopt the GDS, and then bring more value to airline, hotel or car rental company, and finally form a virtuous circle.

However, such network effects can also cause negative same-side network effects. The same-side network effect refers to the change in the value of the same-side user as the number of users on the same side increases. For GDS, whenever an additional airline is added to the GDS, the number of competitors will increase for the existing airlines on the platform, so the value of airlines will be affected.

5. Benefited from the long term growth in aviation, while free from the traditional factors in the industry

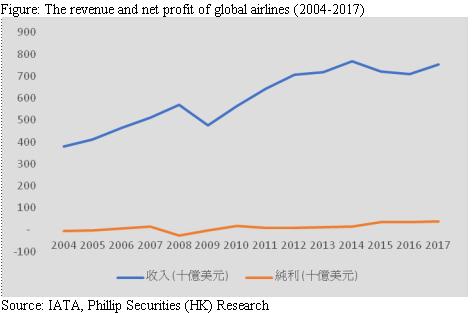

As mentioned by our industry outlook, the aviation industry has been steadily rising. However, the profitability of airlines is very volatile. According to IATA statistics, global airlines have recorded a net losses in 2004, 2005, 2008 and 2009, even if revenues increased. The net profit of airlines is affected by the trend of oil prices. At the same time, due to the high standardization of aviation products, price competition is common in the industry. In addition, The cost of aircraft operation and maintenance are high. These factors have made the net profit of airlines not being in line with the growth of the industry.

However, the aviation information system will not be affected by such traditional factors, but at the same time it can benefit from the development of the aviation industry.

Competitive landscape

Currently, the Group was the only aviation information system provider in China. The domestic airlines in China have all adopted the ICS, CRS and APP of the Group, except Spring Airline and 9 Air Airline. Although there are no clear-cut policies stating that the Group was the only aviation information system provider, the domestic airlines are prohibited to use the foreign GDS, leading to the monopoly in the industry. We believe the reason why the Chinese government has not opened the market is mainly because of its concern on the safety of the aviation data. Thus, they only allow the group which is owned by State-owned Assets Supervision and Administration Commission of the State Council (SASAC) to operate such businesses in effort to protect the data.

However, after China joining to the WTO, the monopoly in Chinese GDS market has been criticized, and foreign GDS companies have asked the Chinese government for opening the domestic market. Therefore, in 2014, the Civil Aviation Administration of China promulgated “Interim Provisions on the Administration of Licenses for Sales Agencies Designated by Foreign Air Transport Enterprises within the Territory of China to Directly Enter and Use Foreign Computer Reservation Systems”, allowing foreign GDS to enter a part of the market in China, such as Abacus and Amadeus. However, it is limited to international flights of foreign airlines or code sharing flights with domestic airlines, while domestic airlines and domestic routes are still not under prohibition.

Although the Civil Aviation Administration has protected the aviation system provider in China, they also impose a price restriction. The maximum guidance price of “flight control system services” and “electronic travel distribution system services” are progressive per segment, ranging from RMB 4.5 to RMB 6.5 for domestic flights and RMB 6.5 to RMB 7 for international flights. That of the “airport passenger processing system services” are RMB 4 per segment for domestic flights and RMB 7 per segment for international and regional flights as well as RMB 500 per aircraft for load planning services.

Conclusion

We believe that aviation information industry in China is worthwhile for long-term investment. First, as passenger and freight transport volume in China rises, aviation information industry will grow steadily. Although the industry is related to the aviation industry, it will not be affected by traditional aviation industry factors, so its profitability is stronger than that of traditional airlines. In addition, thanks to the own characteristics of industry, the entry barriers and the advantages of the leader become more obvious, such as low marginal cost and network effects. Moreover, owing to the policies, the industry is currently monopolized by the group, leading to less fierce competition. Even though the government have open up part of market to the foreign GDS companies, the domestic market is still monopolized by the Group. But, as the Civil Aviation Administration imposed price restrictions, it weakened the advantage from the monopoly.

Competitive advantages

The only provider of ICS for domestic airlines

Except Spring Airlines and 9 Air, the ICS of other domestic airlines are provided and controlled by the Group. The reason why ICS is so important is because no matter through direct channel (Airline's website) or indirect channel (Travel agency), the sales must be handled by ICS. Generally, ICS will charge system service fee and linkage fee, but the Group charged based on the volume of the package of passenger reservations, distribution and departure. Besides, the linkage of the Group's ICS and CRS perform better than linking with other CRS, allowing the advantage in ICS to move into CRS. Furthermore, due to the long development cycle and high expenditure of ICS, most domestic airlines tend to adopt the Group's ICS, while foreign ICS is restricted by the government to enter China, so the group's ICS not only monopolizes the market, but also has fewer substitutions.

Owned by different airline clients and SASAC

The Group have a close relationship with many domestic airlines. Air China, China Eastern and China Southern held 9.17%, 11.22% and 11.94% of the shares respectively, for a total of 32.33%, while other airlines also held 6.51% of the shares. Being the shareholder of the Group, the interest of the airlines is bonded with the Group, which reduces their incentive for breaking the Group's monopoly, but also forces the Group to provide better services.

Besides. the Group is also owned by SASAC. The Chinese government is concerned of the aviation data, so they did not open up the market until 2014. After joining to WTO, the Civil Aviation Administration decided to open the distribution system market to foreign GDS in respond to the requests. However, it did not change the situation of monopolized market, because the foreign GDS still requires to link up with the Group's ICS for reservation. From the reform, the Chinese government is still not comfortable with opening up the whole market. Owned by SASAC, the Group will be in the prefect place to operate this business. As long as the Chinese government remains its protection to aviation system industry, the Group is probably able to monopolize the market.

More competitive pricing than foreign GDS

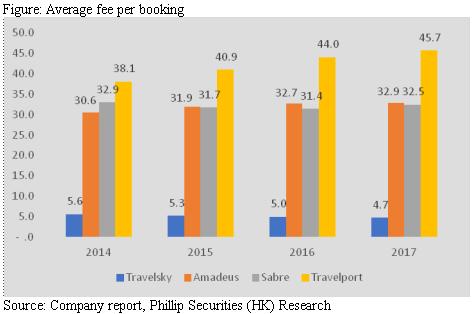

The average fee per booking of the Group is cheaper than that of foreign GDS. In 2017, the fee of the Group was RMB 4.7, while Amadeus, Sabre and Travelport were RMB 32.9, RMB 32.5 and RMB 45.7 respectively. If there was further market opening-up, the competitive pricing will empower the Group, even if the performance level of the Group is still far behind the foreign GDS.

Earnings forecast

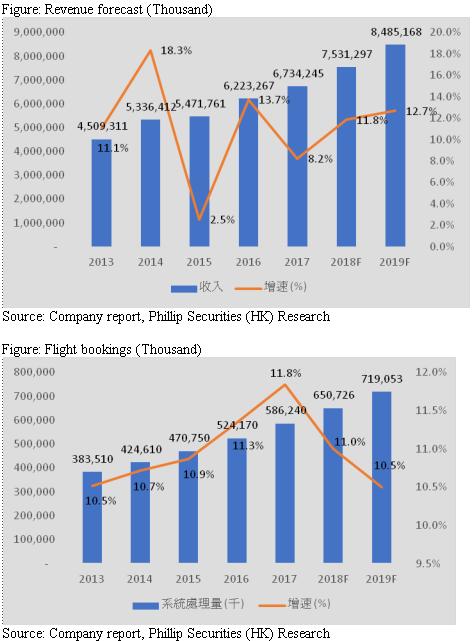

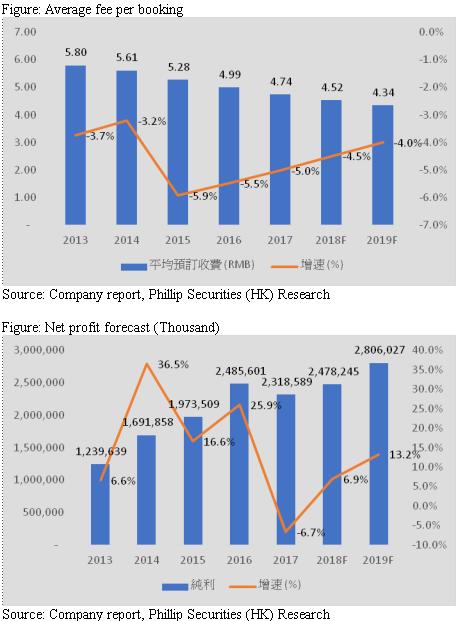

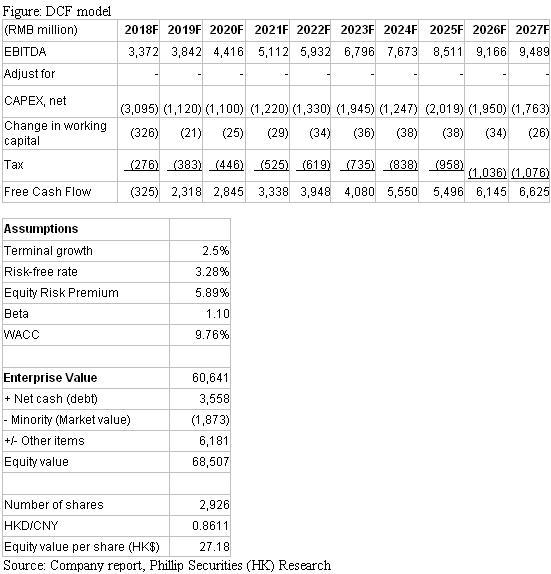

Thanks to the steady increase in the tourist from China, we expect the revenue growth in 2018/19F to be 11%/11.5%, while the flight bookings to grow at 11%/10.5% in 2018/19F. Besides, we predict the average fee to be RMB 4.52/4.34 in 2018/19F, representing a negative growth of 4.5%/4%. We should see a down trend in average fee per bookings as the larger the volume is, the greater the discount will be. However, as the growth of flight bookings slows down, the drop in average fee will also reduce. Finally, we expect the net profit growth in 2018/19F to be 6.9%/13.2%.

Valuation

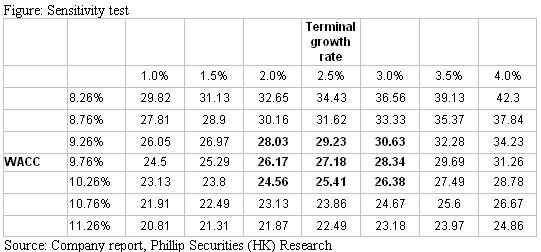

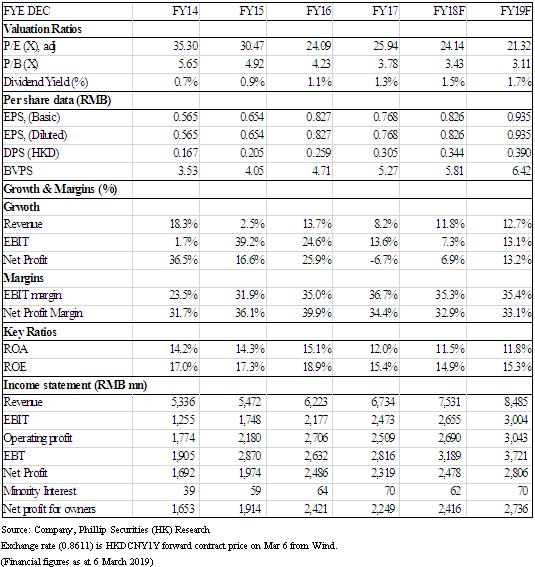

We adopted the DCF model for valuation, where we assume the discount rate to be 9.76%, and terminal growth to be 2.5%, with FCFF forecast to 2027F. We derived a target price of HK$27.18, implied a P/E of 27.6x and 24.4x in 2018/19F. We initiate an “accumulate” rating with a potential upside of 17.7%. (HKD/CNY=0.8611)

Risk

1. Economic downturn

2. Aviation system market opening up

3. Airlines develop their own systems

Financials

Click Here for PDF format...