Sectors:

Air, Automobiles (ZhangJing)

Healthcare, TMT (Eurus Zhou)

TMT, Education, Finance (Terry Li)

Retail, Property (Tracy Ku)

Automobile & Air (ZhangJing)

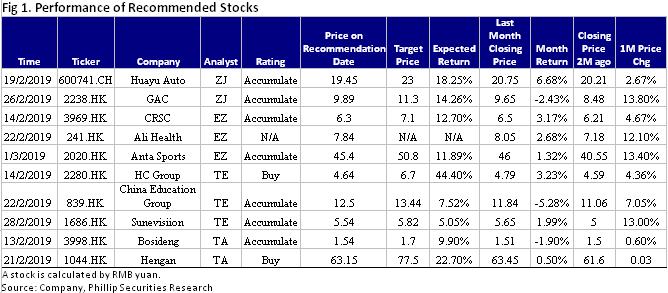

This month I released updated reports of Huayu Auto (600741.HK) and GAC (2338.HK), which got success by their unique Competitive edge. HASCO is the pioneer of China's auto component industry. We believe that to attract customers, auto manufacturers will tend to apply more high-end and high-technology auto parts and components in their automobiles. This trend will certainly benefit top-tier auto parts manufacturers such as HASCO. In the first three quarters, the Company recorded a revenue of RMB11,879,9 million, up by 14.51% Y-o-Y, a net profit attributable to parent company of RMB636,4 million, up by 32.13% Y-o-Y. The company also actively grasps the trend of electric vehicle, network connection, intelligence and sharing of the automotive industry. We reaffirm "accumulate" rating.

In the first month of 2019, the total sales of GAC reached 210,000 units, a slight decrease of 0.21% yoy. Among them, the seals of joint venture brand GAC Honda were 74,000 units, a decrease of 2% yoy; sales of GAC Toyota were 80,000 vehicles, an increase of 75% yoy. With the powerful new product matrix and the marketing strategies in recent years, GAC Toyota's monthly sales volume have increased against the trend, and the growth momentum is rapid. It is expected that the Company will maintain steady growth in the future under the strong product cycle of the Japanese-brand JV. We revised the Company's 2018/2019 earnings forecast. We reaffirm the "Accumulate" rating with the target price to HKD 11.3, equivalent to 8.1/7.4x P/E ratio in2018/2019.

Healthcare & TMT (Eurus Zhou)

This month I released three equity reports, including CRSC (3969HK), Ali Health (241HK) and Anta Sports (2020HK). We tend to recommend CRSC and Anta. In 2018, CRSC's external contracts signed increased by 12.4% yoy, amounting to RMB68.29bn. Railway orders with high gross profit margin has increased significantly, while the general construction contracting business with low GPM has remained stable with contracting proportion. The optimized business structure will help to improve overall profitability. Besides, we also recommend to follow Ali Health. Its adjusted net profit (excluding share option expenses) reached RMB10.49 million, v.s. a loss of RMB34.4 million last year, mainly due to the rapid growth of e-commerce business, and the new profit contribution from the consumer healthcare business, as well as declining SG&A and research expenses. We highlight that its great amount of online users and offline network (involving medical institutions and pharmacies) are expected to form effective synergy in Internet healthcare era.

TMT, Education & Finance (Terry Li)

I released three reports on HC Group (2280.HK), China Education Group (839.HK) and Sunevision (1686.HK). We highly recommend China Education Group. On Feb 13 this year, the State Council of PRC published “Implementation Plan of Reforms on National Vocational Education” (Plan), proposing number of reforms, targets and concrete indicators. Among them, the article 13 and 16 are positive to the long term development of the Group. The article 13 clearly expresses its support for the social capital to enter vocational education, where the Plan supports and monitors the social parties to establish vocational education and encourages the development of vocational colleges and vocational training institutions which adopt shareholding system or mixed ownership system. The stance of this article is in line with the Law on the Promotion of Private Education that published previously, in which both of them supports the presence of the private higher education colleges. The valuation could revive thanks to the clear supportive stance for higher education of the Plan which alleviates the concern from the market. This article provides the guidance on the education funding. It should be tilted to on the central and western regions, poverty-stricken areas and ethnic areas. We believe the local government will launch more and more favourable policies, such as tax exemption or low land transaction fee. It is possible that there will be new acquisition target in central and western regions for the Group.

Retail, Property (Tracy Ku)

This month I released the first coverage report of Bosideng(3998) and Hengan(1044). I highly recommend Bosideng. Although this winter is "not too cold", the sales growth of branded down apparel under Bosideng has accelerated since last December. The management team has raised its whole-year revenue growth guidance of branded down apparel business under Bosideng from 20%-30% to over 35%, other business still maintains, i.e. OEM management business is more than 20%, ladieswear business is medium to high, diversified apparels business will continue to shrink as its new strategic principle is focusing on principal business and key brands while implementing de-diversification.

During the first nine months of FY2018/19, the accumulated retail sales of down apparel products under the core brand-Bosideng increased by more than 30% y.o.y. which is higher than 24.1% in 1H. This means that the growth rate in Q3 has accelerated. According to the management team, the weather was still warm during October to November, thus this business recorded an increase of only 20 to 30%. However, the weather began to turn cold in December, with an increase of more than 50%. It is expected to continue to maintain rapid growth before the coming Luna New Year.

The business showed both prices and sales recorded growth in Q3, and management expects the trend will continue in 2019. The business is currently being transformed from the mass market to the mid-to-high end. The current ASP of the products is about RMB1,200-1,500, which is still quite far from its overseas competitors such as Canada Goose of Canada. The management team's goal is to raise the ASP of 20 to 30% per year in the coming three to five years.

We are optimistic about the company's ability to raise ASP in the medium and long term. The improvement of its product design, branding and channels will be the drivers of sales volume. We expect the overall revenue to maintain a high-speed growth momentum, and GPM will also have room to improve further.

Click Here for PDF format...