Investment Summary

Q4 Results Basically Stay Flat

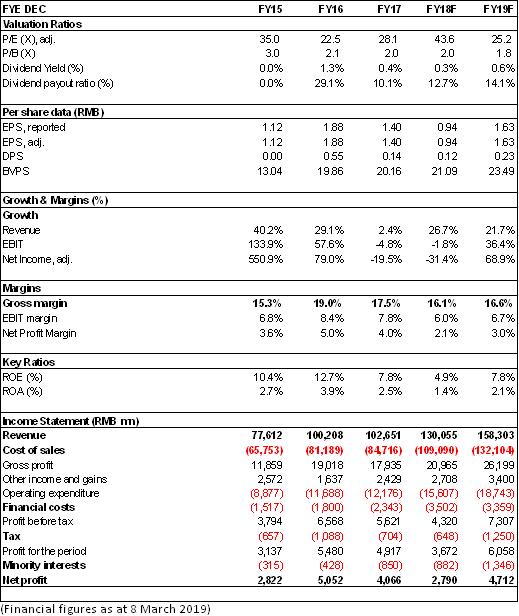

Recently, BYD released its 2018 preliminary report: in 2018, the company recorded a revenue of RMB130.055 billion, up by 22.8% yoy, and a net profit attributable to shareholders of RMB2.79 billion, down by 31.4% yoy. Among them, the net profit attributable to shareholders of the fourth quarter was RMB1.26 billion, which was at the bottom of the RMB1.2-1.6 billion of Q3 report. It is basically flat yoy (down slightly by 1.18%), lower than our expectation.

New energy vehicles grow rapidly, only fuel vehicles and mobile phone business are dragged down

The company's quarterly net profit attribute to shareholders was RMB102 million, RMB377 million, RMB1.048 billion and RMB1.26 billion, down by83%,66%,1.9%, and 1.2% you, respectively. The trend of quarterly improvement was mainly driven by the high growth rate of the company's new energy vehicles and the quarterly increase in sales volume (the growth rate of the company's new energy passenger cars increases by -34%, 52%, 51% and 42% qoq, respectively).

On the other hand, the fierce competition brought about by the decline of the domestic fuel vehicle industry has affected the profitability of the fuel vehicle business to a certain extent, although the sales volume is stable, the profitability is under pressure. In terms of mobile phone components and assembly business, due to the weak demand in the industry and the intensified market competition, both orders and profits are under great pressure. Affected by policy changes and impairment, the loss of photovoltaic business increased during the year. In addition, the increase of financial costs caused by the rising cost of financing has also affected the overall profitability of the company to a certain extent..

New energy vehicles business is getting better

In 2018, the company's sales of new energy vehicles achieved high growth, and it continued to hold the post as the sales championship of new energy vehicles for four consecutive years in the world. The leading position in the industry was further consolidated, but the overall sales of fuel vehicles remained stable. BYD's total auto sales in 2018 reached 520,687 vehicles, up by 45.16% yoy. Among them, 247,811 new energy vehicles were sold, up by 118% yoy, and 272,876 fuel vehicles were sold yoy, up by 11.35% yoy. Among new energy vehicles, 103,000 pure electric passenger cars, 124,000 plug-in hybrid passenger cars and 20,000 new energy commercial vehicles were sold.

In December 2018, sales volume of new energy vehicles and fuel vehicles were 46,650 and 22,987, respectively, up by 118% yoy and down by 34% yoy, while in January 2019, sales volume of new energy vehicles and fuel vehicles were 28,668 and 15,252, respectively, up by 292% yoy and down by 56% yoy, respectively. The strong momentum of new energy vehicles and the destocking of fuel vehicles continued.

In 2019, the company will launch a new generation of pure electric version of Tang EV600 and hybrid power of Song Max, as well as a new generation of Song, whose front face will continue to be the family style, but its appearance, interior and bottom pan will adopt a new design. In addition to the dynasty series, the e-series models including e1 and S2 will also be launched. In addition, in order to cope with the subsidy retreat, the company launched Yuan EV535, whose endurance mileage is increased to 420 km. The price has also increased, and part of the price is transferred to the cost of subsidy retreat.

It is worth mentioning that Dragon's front face has contributed a lot to the promotion of the overall image of the company's products, and the company has not stopped introducing high-end talents in the world. Recently, it announced the introduction of Lopez, former Ferrari exterior design director, and Paganetti, former Mercedes-Benz interior design director, to reserve talents for further improving the brand image of the Dynasty series.

Investment Thesis

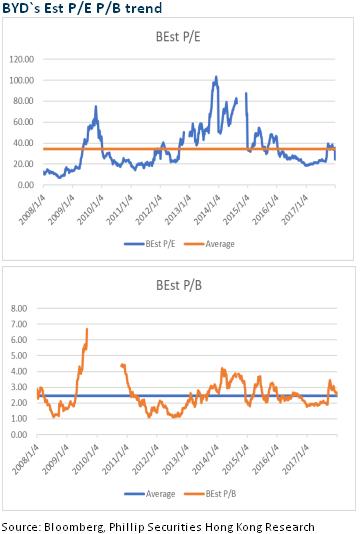

Although the results of BYD in 2018 are below our expectation, the technological improvement, transformation and implementation of BYD in recent years have activated its overall competitiveness again. The Company will fulfill its results. We believe that the Company has made forward-looking preparation for all kinds of challenges and its leading position will be enhanced. We are optimistic about the more stable and sustainable growth of the Company in the future. As the latest estimates, we revise the target price to HKD56.3, which corresponded to 2.3/2.1x P/B ratio for 2018/2019. We give the rating of “Accumulate”. (Closing price as at 8 March 2019)

Risk

Sales of new energy vehicles is not as good as expected

Cloud Rail business risk

Slow-down of Hand-set components business

Financials

Click Here for PDF format...