Investment Summary

The interim revenue of FY2018 increased by 11.4% y.o.y. mainly due to the price hikes of some of its products, and the sales volume of mid- to high-end products also increased. The ASP during the period has increased by 13%, while the sales volume was slightly affected by the mark-up, decreased by only 1.5% . During the period, GPM increased significantly by 2.5 ppt to 36%. According to the management team, the overall business performance including indicators like sales volume and GPM of 2H was worse than that in 1H, which was due to the weak macro economy and the company's strategy of not joining the price war of the industry. The total sales volume of FY2018 was worse than the market (0.8% decline for industry sales), and the market share has also fallen from 27% in 2017, but still in the leading position. The company's FY2019 sales target is to keep constant of that of in FY2018. There will be fewer chance of another round of price hikes. But as it will continue to develop mid- to high-end business, ASP is expected to have a low single-digit growth every year In the next three to five years.

China's beer industry is processing towards premiumization, while the low-end market is shrinking. Therefore, we believe that it is difficult to assess the progress of individual companies` transition to mid- to high-end and capacity optimization based on market share alone, and this progress will benefit future revenues growth and the expansion of profit margins. According to the management team, sales of high-end products has continued to grow even in 2H. The company's mid-to-high-end products i.e. selling price more than RMB5, accounted for 39% of the total revenue in FY2017, and increase to 43% in 2018.

The company has announced the acquisition of Heineken China(including HK) last year. We expect that with the acquisition, the share of mid- to high- end business will further increase, with the possibility of increasing to over 50% between 2020 and 2021. In addition, it will also help to expand GPM of CRB. Heineken's global business GPM is as high as around 40%. As the China market is dominated by high-end products, we suppose GPM of Heineken China is higher than this level. The high-end beer market in the 1st-tier cities is currently dominated by foreign brands like Budweiser and AB InBev, while in other regions, there is still much room for development. The management team plans to further develop the 1st- and 2-nd tier regions with Heineken, and to launch new lines under Snow Beer in each price segments of more than RMB10with Heineken , e.g. RMB10-12, RMB12-15. As the two brands are different in market positioning, the management team does not worry about direct competition.

The acquisition is currently still awaiting approval from the Ministry of Commerce. The management team expects it to be approved in 1H of 2019 and Heineken China will be included in CRB's financial report in 2H. It is expected that 2019 will be a period of adjustment for the two and the situation will be gradually improve. The team is optimistic about the performance of 2020. The target companies recorded a total after-tax loss of RMB66.8 million in 2017. In our points of views, the impact on the financial statements of CRB is minor i.e. CRB recorded net profit in 2017 of RMB1.175billion. In 2017, Heiken China's loss was mainly due to the increase in marketing expenses as lacks the channels to digest or effectively reach the end market. With the cooperation of CRB, we believe this can be improved.

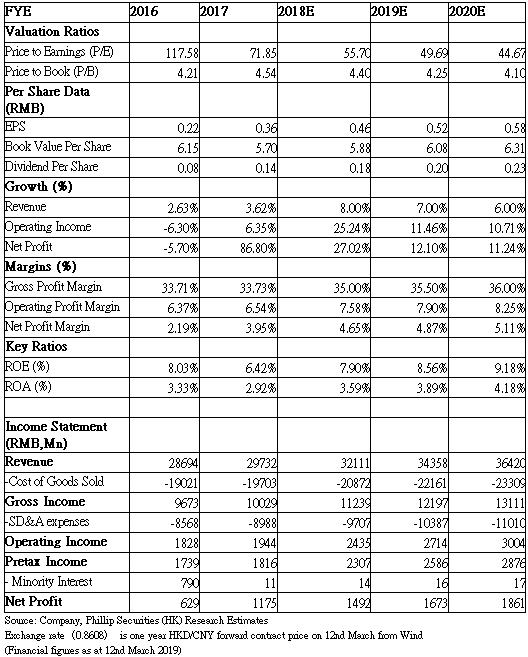

According to the management team, it will continue pay attention to suitable M&A projects. The target is popular foreign brand and non-largar manufacturers, while lager business will be mainly developed with Heineken China. We expect EPS of FY2019 will be RMB0.52, with target price HKD30.3,and target price-earnings ratio 50.2 times . (current price as of March 12, 2019)

Business Overview

About the company

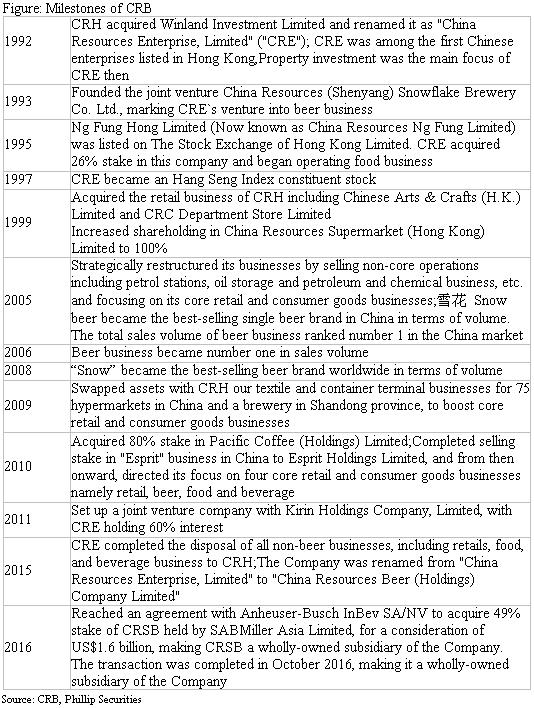

China Resources Beer , listed on The Stock Exchange of Hong Kong Limited under the stock code 291.HK, is a beer listed subsidiary company of China Resources Holdings. It focuses on the manufacturing, sales and distribution of beer products.

In 2015, it successfully completed its business restructuring and transformed itself into a beer-focused enterprise, and was renamed from China Resources Enterprise to China Resources Beer. In October 2016, it completed the acquisition of 49% stake of China Resources Snow Breweries , which became a wholly-owned subsidiary of the company.

It has been in the beer business in China since 1994. Its total sales volume ranked number 1 in the China market since 2006. The flagship brand “ Snow” has become the largest beer brand by volume worldwide.

1H of FY2018 Results Review 2019 Continues to Drive Capacity Optimization

During 1H, beer consumption benefited from economic development and weather conditions. The overall beer market volume increased compared with the same period last year. The beer market continue to enjoy a consumption upgrade, with growth in the proportion of mid-to high-end beer sales volume, which further enhanced the product mix upgrade. Turnover and profit attributable to the company's shareholders during the period were RMB17.565 billion and RMB1580 million, representing an increased of 11.4% and 28.9%, respectively.

In terms of GPM, the management team expects that GPM of 2H and the whole financial year to be lower than 1H. The cost of raw materials like barley has increased while wrapping paper has decreased, thus the overall cost is controllable. Assuming that the overall raw material costs are stable, and the company continues to develop high-end business, GPM is expected to continue to improve in the coming years.

In terms of operation expenses, the company plans to control it through continuing its precise advertising and branding strategies. Taking “Brave the World Super Ex” as an example, there is no large-scale advertisement in traditional channels such as CCTV in1H of 2018, but launching interactive activities for emerging customers such as iQiyi online TV platform targeting young people aged 18 to 25.

In 1H of FY18, the company continued to promote the optimization of production capacity and increase capacity utilization. There was one brewery ceased operation. As at the end of June 2018, there were 90 breweries in operation in total. According to the management team, there were 5 to 10 brewery ceasing operation, another 5 to 10 breweries will be closed in 2019, plusing 2 in 2016 and 5 in 2017, the ultimate goal of 2020 is to close 20 to 30 breweries. In the future, it may continue to close more breweries.

Investment Thesis & Valuation

We expect EPS of FY2019 will be RMB0.52, with target price HKD30.3,and target price-earnings ratio 50.2 times . Potential investment risks include revenue growth or channel expansion missing expectation, market competition deteriorates,huge fluctuations of raw material costs . (current price as of 12 March, 2019)

Financials

Click Here for PDF format...