Investment Summary

Amazing Result in 2018

Joyson recently released its result forecast for 2018. It is estimated that the net profit attributable to shareholders will be RMB1.25 billion to RMB1.45 billion in the whole year of 2018, up by about 216%-266% annually, and the EPS is about RMB1.36-1.58. The net profit attributable to shareholders except non-recurring profit and loss will be RMB900 million to RMB1.05 billion, up by about 2,100%-2,433% annually, and the main business income is expected to be about RMB53.8 billion. According to this calculation, the Company's quarterly attributable net profit is RMB31 million, RMB790 million, RMB237 million and RMB290 million (median), respectively, down by 85%, up by 94%, down by 13% and up by 159% annually.

The Acquisition of Takata Asset and the Integration Effect Enhance the Result

The Company's result in 2018 ushered in a turning point, especially in the second and fourth quarters, which was better than our expectations. The main reason is that in 2018, the Company completed the acquisition of high-quality assets of Takata Company, and the benefits of the release of production capacity corresponding to related assets enhanced the result of listed companies. After the acquisition of high-quality assets of Takata Company, the Company improved operational cost and efficiency of automotive security by steadily integrating regions. The estimated impact of non-recurring profit and loss such as takeover of Takata's global assets and global business integration after the acquisition on the Company's result is RMB350 million to RMB400 million. In addition, the company's automotive electronics and automotive functional parts business has maintained a sustained and stable growth in 2018 with the continuous increase of customer orders..

BMS Business of New Energy Vehicle Gains Big Order, Opening up the Space for Performance Growth in the Future

Recently, the company disclosed through its official website that its subsidiaries have successively gained nearly RMB10 billion in new energy vehicle battery management system BMS related business orders from customers such as Volkswagen, Benz, Nissan, Ford and SGM-Wuling. The above orders will be put into mass production from the end of 2019.

Joyson has been focusing on R&D investment, which accounts for more than 8% of the annual R&D expenditure. Prospective global merger and acquisition layout and sustained large-scale R&D investment ensure the company's competitiveness and leadership in the subdivision industry. At present, Joyson has more than 5,000 technical patents in reserve. Its patents cover all fields of active and passive safety, intelligent driving, vehicle networking and power management of new energy vehicles.

The company's Joyson Preh has been the exclusive contractor of BMS systems for BMW's new energy vehicles since 2008. It has supplied more than 150,000 BMS systems for BMW, including i3/i8/ existing EV and PHEV models of 3, 5 and 7 series cars. It also started to develop 48V-BMS system with Mercedes-Benz in 2017. In addition, the company began to supply Tesla in 2014.Domestic automobile companies, including Geely, Chery and other independent brand automobile companies, have begun to use Joyson's BMS products since 2016.

We anticipate that the company will gain more new orders in the new energy vehicle market with the competitive advantage in technology and market.

Investment Thesis

The company completed its share repurchase plan of RMB1.8 billion in November 2018, and the capital stock repurchase is 7.58%, which demonstrated the management's confidence in the company's future development. 2017 is an important year in the history of company's mergers and acquisitions, and 2018 is the year of integration. Integration not only makes the company's leading position more stable, but also opens up more space for long-term sustainable development.We revised the target price of RMB 31.5 equivalent to 23/21x of 2018/2019's estimated EPS, and assign Accumulate ratings. (Closing price as at 15 March 2019)

Risk

Operating collision in Joyson's M&A

Worse-than-expected downstream demand

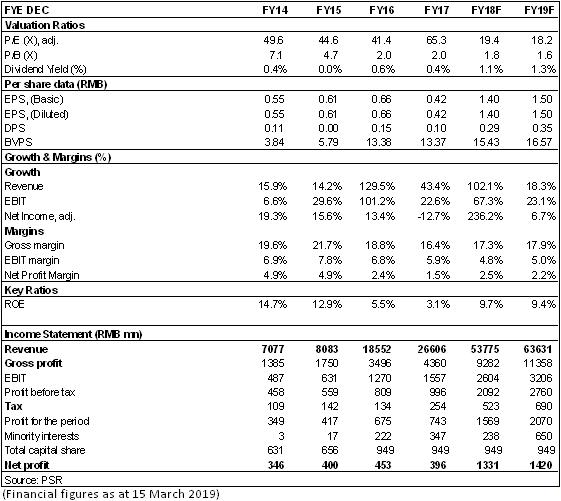

Financials

Click Here for PDF format...