Investment Summary

The growth of Cloud services regained its momentum and beats our expectation, but that of traditional ERP just fell below our expectation. We believe the most critical part of the short selling report is about the transaction with related parties on Cloudhub, but the Group currently failed to provide further information on it. However, we expect there will be a further disclosure in the future. We give a target of $9.21, 5.4%, higher than previous, maintaining an “Neutral” recommendation, with 0.44% potential upside. (Closing price at 20 Mar 2019)

Annual result update

The growth of Cloud services regained its momentum and beats our expectation, while that of traditional ERP just fell below

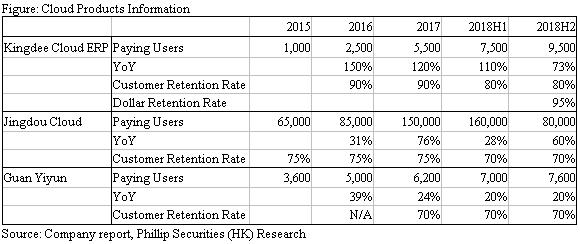

The Group announced its annual report, in which the total revenue has grown by 21.9%, reaching RMB 2.81 billion; the net profit to equity holders grew by 32.9% to RMB 412 million; the operating cash flow was up by 9.9% to RMB 906 million. The revenue growth of traditional ERP and Cloud services were 12.9% and 49.5% respectively. For traditional ERP, both of KIS and EAS grew, about 6% and 19% YoY respectively, but the K/3 dropped by 12% due to the cloud migration of medium enterprises. The implementation and maintenance were both up by 26% and 14% YoY because of the strong demand from EAS. For cloud services, the revenue growth of Kingdee cloud reached 54% YoY and the other clould services such as Jingdou Cloud, Guanyi E-Commerce and Cloudhub was 40% YoY. For Kingdee Cloud, the retention rate in terms of customer and dollar were 80% and 95%.

The growth on cloud services has beaten our expectation (49.5% vs 45%) and regained its momentum in the second half of 2018, which increased by 73.3%, after a disappointed result in first half. The Kingdee Clould Cosmic, targeted the large-sized enterprises, has already acquired 15 customers, including WENS and Huawei. However, the growth on traditional ERP was below our estimates (12.9% vs 17%), due mainly to the decline in K/3 as the cloud migration of medium enterprises. The gross profit margin was 0.7% higher than our estimate, and the operating profit excluding fair value gains on investment properties was slightly below our forecast, just 2.4%.

Recent events

There was a report released on 18 March, accusing the Group of booking additional profit from transactions with related parties and relying on sector-specific tax benefit, government grants and property investment gains.

As for the sector-specific tax benefit and government grants, it is common for a software company to enjoy such tax benefit in China, since software industry was generally categorized as one of the industries that the Chinese government supports. Therefore, we tend to believe such tax benefits would not be altered in short term. Moreover, the management explained that the government grants were the reward from the Group involving into the R&D projects from the governments, implying it is not out of thin air.

As for property investment gains, we believe the public has been well aware of the property investment gains, as the segment has long been disclosed to the public clearly, even though the Group has not clearly mentioned the detail of the rental, which it is understandable because it is not the major business of the Group. Like our report, we usually exclude the fair value gains from investment properties, we think the property investment gains were not a big concern.

What we believe it is most critical part is about the transactions with related parties on Cloudhub, where the Group sold on July 2016 and bought back on March 2019. The report criticized the Group absorbed losses of its main products by Cloudhub when it is off the balance sheet of the Group. And, the report actually stated that it is only an “inference”, so it means we just could not come to a strong conclusion based on the current information available. However, we did see the point of that report, and believe the shift and back of Cloudhub is worth for further investigation. Unfortunately, during the conference call with the management team, the Group failed to disclose the detail of the transaction and the financial detail of Cloudhub, but we expect there will be a further disclosure of the transaction in the near future. Until now, the Group has disclosed that the amount of loans to Cloudhub was RMB 29 million as of the end of 2018. And, the massive increase in loans to related parties was mainly to Qingdao Xinrun Real Estate Limited as land payments for Qingdao Kingdee Software Park. It alleviates the concern on whether the Group has provided a huge capital to Cloudhub, but still there is no explanation on whether Cloudhub absorbed losses of the Group. If the Group failed to address such issues properly, it will no doubt jeopardize investors` confidence on the corporate governance of the Group, leading to a slump on valuation.

The report also criticized that the Group just barely makes a core operating profit by a set of calculation. However, we think it is not appropriate to analyse by just looking at the aggregate core operating profit. As the cloud services are still losses making, it will underestimate the value of cloud services (which are the most valuable part of the Group) if we just look at the aggregate.

Valuation

We adopted sum of the parts valuation by dividing the business into three parts: 1) Traditional ERP business (P/E), 2) Cloud business (P/S), and 3) Investment real estate business (book valuation). We forecast the earnings per share of the traditional ERP business in 2019F to be RMB 0.115, 8.7% lower than the previous estimate, with target PE ratio 15x as we expect the growth will drop to single digit; the revenue of cloud services per share in 2018 would be RMB 0.386, 3% higher than the previous estimate. We maintain the target PS ratio to be 13x; for the investment real estate business, the book valuation is used, and the valuation per share is RMB 0.55. Finally, a net cash is RMB 0.46 per share in 2018. A target price of HK$9.21 was obtained, 5.4% higher than previous target price, and we remain “Neutral” recommendation, with 0.44% potential upside. (HKD/RMB: 0.8626)

Risk

1. Slower-than-expected growth in cloud products

2. The economy of China slows down

3. Cloud ERP may take away the existing customers of traditional ERP, particularly SME

4. The Group fails to address the issues properly, because there is no further disclosure on information

Financials

Click Here for PDF format...