Investment Summary

ChinaSoft International is one of the leading software and information services companies in China. Revenue growth in line with our expectations, while net profit surpassed it. And, emerging business became the new growth driver. Based on 2019 net profit, we assume a P/E ratio of 16.5x (average over the past three years), deriving a TP of HK$6.57, 22.3% higher than previous TP, we reiterate a “Buy” rating with a potential return of approximately 41.0%. (Closing price at 27 Mar 2019)

Annual result update

Revenue growth in line with our expectations, while net profit surpassed it

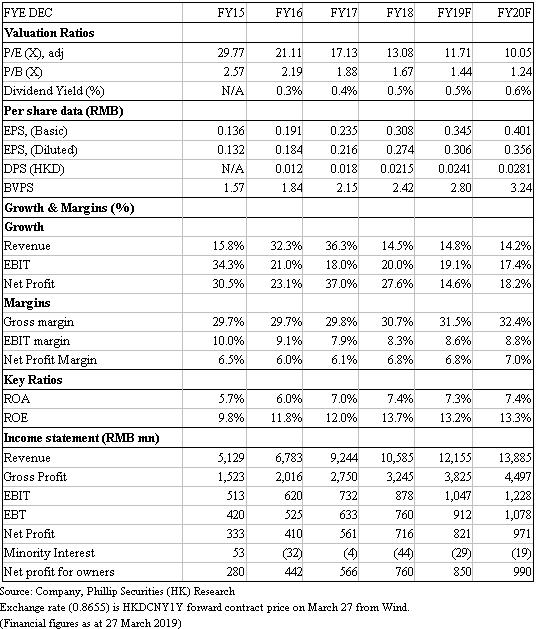

The total revenue in 2018 reached RMB 10.6 billion, increased by 14.5% YoY; the net profit attributable to the shareholders was RMB 715.8 million, up by 26.6% YoY. The gross profit margin improved from 29.8% to 30.7%, thanks the increasing portion of emerging business that has higher gross profit margin.

The revenue was generally in line with our expectation, just 0.9% lower, but the gross profit margin was slightly lower than expected, 0.3%. The net profit was above our estimate, about 7%, thanks to the lower administration cost and tax expenses that are deducted on certain research and development expenses.

Demand from Large-sized customers remains strong, but that from small and medium-sized customers became stagnant

The revenue from Technology Professional Services Group (TPG) grew by 16.7% to RMB 9.2 billion, thanks to the strong demand from large-sized customers. The revenue from the largest customers (Huawei) increased by 15.3% to RMB 5.6 billion, accounted for 53.1% of the total revenue. Meanwhile, the revenue growth from HSBC and Ping An were around 47% and 40% respectively. We believe it shows the fact that the large-sized customers are less sensitive to the economic cycle, which will remain the main driver of the Group during the economic downturn.

However, the revenue from Internet IT Services Group (IIG) just grew by 1.8%. The tiny growth was attributed to the pessimistic outlook of the economy, leading to a reduction in IT expenditure from small and medium-sized customers.

Fast-growing emerging business became an new growth driver

The revenue from Cloud, Big date and Jointforce has reached around RMB 1.6 billion, up by 60% YoY, becoming the new growth driver for the Group. For Cloud Software Park, it is covering 15 cities in 11 provinces, including Jiangsu, Shandong, Hubei, Anhui and so on. For Cloud Integration Platform, the registration from government units exceeded 3,000 with 263 number of projects and the amount was above RMB 137 million. For Jointforce, the number of clients placing packages in the platform has grown by 83% to around 55,000. Since the emerging business has a higher gross margin and create a strong switching cost, we believe the valuation will be enhanced as the proportion of those businesses goes up.

Valuation

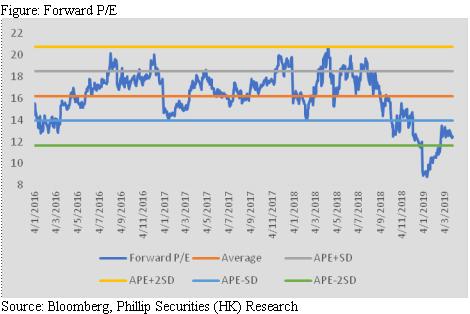

We expect the revenue growth of TPG to be 16.5% in 2019, in line with last year, while that of IIG will revive to 4%. Meanwhile, emerging business will remain fast-growing, about 50%. Based on 2019 net profit, we assume a P/E ratio of 16.5x (average over the past three years), deriving a TP of HK$6.57, 22.3% higher than previous TP, we reiterate a “Buy” rating with a potential return of approximately 41.0%. (HKD/CNY=0.8655)

Risk

1. Slower-than-expected growth in SaaS market

2. Suddenly loss on major customers

3. Slower-than-expected growth in emerging business

4. New products replace the company's existing products

Financials

Click Here for PDF format...