|

IRC(1029)

Analysis:

IRC (1029) recorded a drop of 39.8% in net profit to US$68.2 million for the year ended 31 December 2018. However, EBITDA of the Group increased 42% to US$28.5 million, mainly attributable to the 39% increase in revenue to US$151.5 million. The production capacity of its K&S mine has reached about 86% currently and is expected to be operating at a full capacity of 3.2 million tonnes per annum soon, and to capitalize on economies of scale, the mine has the potential to further expand its annual capacity by 40% to 4.5 million tonnes. Further improvement in production costs will render it to be one of the lowest-cost mines for the production of 65% Fe. (I do not hold the above stock)

Strategy:

Buy-in Price: $0.14, Target Price: $0.165, Cut Loss Price: $0.125

|

NATURAL FOOD IH(1837)

Analysis:

The Group is the second largest natural health food company in China. The products can be categorized into four types, namely, (i) formula-based mixed grain powders, (ii) mix & match powdered grains, (iii) grains-mates and (iv) other natural health food and products. Thanks to the growing aging population and increasing health awareness, Frost & Sullivan predicts the CAGR of retail sales value of natural health food market in China will be 12.3% in the next five years, higher that of revenue of food industry (6.8), implying that the growth of the Group is tremendous. The Group announced its annual result, where the revenue grew by 15.4% to RMB 1.82 billion; the adjusted net profit was up by 13% to 210 million. Besides, the gross profit margin remained on 76%. The online distribution has become a new growth driver of the Group, where the revenue from online sales has reached RMB 340 million, up by 63%, accounted for 18.7% of the total revenue. Besides, the Group commenced construction of the first phase of our Nansha Manufacturing Facility and expect the construction to be completed toward the end of 2019, expecting a 20,000 tons increase in production capacity.

Strategy:

Buy-in Price: $1.60, Target Price: $1.90, Cut Loss Price: $1.30

ARK Innovation ETF (ARKK)

ARK Innovation ETF is an actively-managed thematic ETF incorporated in the USA, with market cap of approximately USD 1.34 billion and expense ratio of 0.75%. The investment theme of ARKK is “disruptive innovation”. ARKK mainly focus on investing in companies introducing technologically advanced products or services which potentially changes the way the world works. The issuer of ARKK, ARK identifies 36 innovative companies from four themes: “Genomic Revolution”, “Industrial Innovation”, “Next Generation Internet” and “Fintech Innovation”. For “Genomic Revolution”, the fund invests in healthcare companies based on R&D of DNA technologies including gene therapy and Molecular Diagnostics. For “Industrial Innovation”, the fund puts the emphasis on areas of autonomous vehicles, 3D printing and Robotics. For “Next Generation Internet”, the fund targets in companies from digital media, social platform, cloud computing, Internet of things and E-commerce. For “Fintech Innovation”, the fund offers exposure on technology which makes financial services more efficient such as big data& machine learning, Blockchain and P2P. Compared to mutual funds with true active management, ARKK is more cost effective, which offers investors exposure to innovation across sectors. Recommend to buy at $44, target price $59, cut loss if drop below $42.

|

|

|

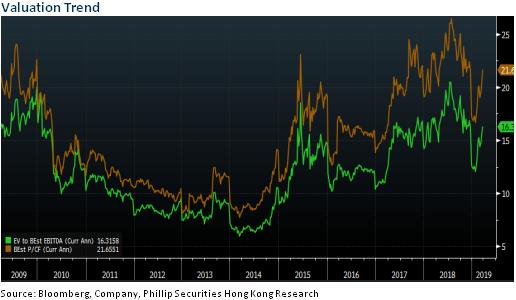

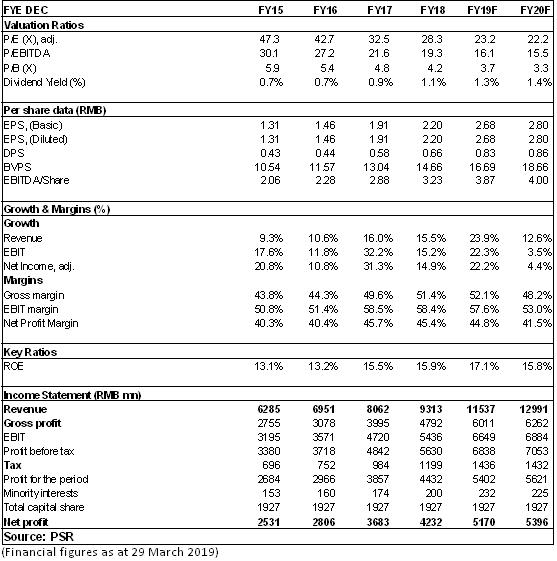

SIA (600009.CH) - Sustained Rapid Growth of Non-aeronautical Business

Rapid Growth of Results Shanghai International Airport (SIA) achieved a revenue of RMB9.313 billion in 2018, up by 15.5% yoy, and a net profit attributable to parent of RMB4.23 billion, up by 14.5% yoy, with a basic EPS of RMB2.2, slightly lower that our expectation by 7.7%. Its DPS was RMB0.66, with a dividend payout ratio maintained at 30%. Its weighted ROE rose to 15.85%, up by 0.32ppts. Steady Growth of Aeronautical Business In 2018, the traffic in SIA was controlled, with a recorded increase of less than 5% in aeronautical business (+3.6% for takeoffs and landings and +5.6% for passenger throughput). However, thanks to the price raising effect of the internal routes by domestic airliners and the scaling-up of international routes and wide-bodied aircrafts, the revenue from aeronautical business grew faster than the traffic, up to RMB3.969 billion, with an increase of 6.58% yoy, maintaining a steady growth on the whole. Sustained Rapid Growth of Non-aeronautical Business Unlike the restricted aeronautical business, the Company's non-aeronautical business recorded a sustained rapid growth up to RMB5.34 billion, with a surge of 23.2% yoy. Wherein, the commercial rental revenue increased by 33% yoy, up to RMB3.986 million, mainly benefiting from the increased proportion of international tourists with stronger consumption intention and the Company's sustained management, site optimization and adjustment of commercial retail brands. Of the commercial rental, over RMB3.5 million are from duty-free stores, the total volume and per customer transaction (RMB300/per customer) of which both recorded a rapid growth, with a growth rate of around 40% and 20% yoy, respectively, reflecting that duty-free stores in Pudong Airport were becoming a shopping hotspot for international routes passengers. Cost Growth Within A Stable Range Except its running cost, the Company's other costs were well controlled. Its total cost stood at RMB4.57 billion, up by 9% yoy. Wherein, the running cost grew rapidly to 1.91 billion, up by 28.6% yoy, and the labor cost increased by 7.5%, while other operating costs dropped by 14.1% yoy, mainly due to the expiration of depreciation period of fixed assets and the non-bond interest expense of the current period. The raise of entrusted management fee due to the scaling-up of duty-free store business and the increase of one-off maintenance expense contributed to the growth of operating costs. Settlement of Duty-free Bidding Allowing the Growth of Non-aeronautical Business In September, 2018, SIA entered into a new tax-free contract with Sunrise Duty Free, in which its minimum guaranteed commission will be RMB41 billion during the seven years from 2019 to 2025, deduction rate will be 42.5%, and its duty-free area will increase from 6,600km2 to 16,915km2, with a substantial increase of 156%. We believe that, under the tide of consumption upgrading driven by outbound tourism, the tax-free business will allow the Company's non-aeronautical business to grow, which will not only provide a solid foundation for the Company's next round of development, but also, hopefully, launch a new business operation pattern that will fully release the valuation premium of the Company as a leading hub airport. Investment ThesisConsidering the Company riding on the new round of stable growth period, we revise the Company's EBITDA per share in 2019 and introduce 2020E EBITDA per share. The target price is increased to RMB 67, with the estimation of a 17.3/16.8x multiple respectively during the two years, and the "Accumulate" rating is maintained.

�Financials

Click Here for PDF format...

| Recommendation on 2-4-2019 | | Recommendation | Accumulate | | Price on Recommendation Date | $ 62.150 | | Suggested purchase price | N/A | | Target Price | $ 67.000 |

| |

|

|

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the “Group”) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products’ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

版權所有, 翻印必究。

Copyright(C) 2019 Phillip Securities (HK) Ltd. All Rights Reserved.

|