|

CR ASIA(831)

Analysis:

For the year ended 31 December 2018, Convenience Retail Asia (831) recorded turnover of HK$5.32 billion, representing a 4.4% increase compared to the same period in 2017. Profit attributable to shareholders increased 21.9% to HK$183 million while the gross profit margin increased 1.2 percentage points to 38.1%, mainly attributable to the Group`s effective eCRM programmes---especially "OK Stamp It"---strong sales momentum for Cirkle K`s packaged drinks and ice cream and the developing business Zoff. As at 31 December 2018, the Group had a net cash balance of HK$508 million and no bank borrowings. The Board of Directors has resolved to declare a final dividend of 17 HK cents per share. Full year dividend amounted to 22 HK cents per share, representing a pay-out ratio of 91.5% and dividend yield of 5.6%. (I do not hold the above stock)

Strategy:

Buy-in Price: $3.87, Target Price: $4.40, Cut Loss Price: $3.70

|

QINGLING MOTORS(1122)

Analysis:

The Group is principally engaged in the production and sale of Isuzu light, medium and heavy-duty trucks, pick-up trucks, multi-purpose vehicles and diesel and petrol engines. The Group announced its 2018 annual result, where the revenue grew by 3.5% to RMB 5.25 billion; the net profit attributable to shareholders dropped by 8.7% to RMB 450 million, due mainly to a RMB 80 million of provision for litigation. The dividend of the Group is stable, and its yield reached above 8% based on current price. Besides, the balance sheet of the Group is quite solid, in which there was around RMB 5.7 billion of cash and deposits with no interest-bearing debts. It will be helpful for a stable dividend payout, even if the business turns bad due to the economic cycle. Moreover, the price-to-book ratio was just 0.62x. As most of the assets were cash, the Group could pay out the cash in order to enhance the valuation.

Strategy:

Buy-in Price: $2.20, Target Price: $2.60, Cut Loss Price: $2.00

KOBE BUSSAN CO., LTD. ( 3038.JT )

Founded in 1985, KOBE BUSSAN CO., LTD. is a supermarket franchise store operator which mainly deals in foods stuffs. The Company also has direct-run stores. Besides, it operates Chinese and Western restaurant catering including “Kobe Cook World Buffet” & “Green's K”, and Renewable Energy Business. For its earnings report of first quarter of 2019 fiscal year announced on 14th March, 2019, the year over year growth of revenue, operating income & net income of KOBE BUSSAN CO., LTD. were 5.1% (¥70.64 billion), 11.1% (¥4.23 billion), and 3.3% (¥2.7 billion) respectively. For major business segment, the number of `Business Supermarket` store increased by 6 to 819. KOBE BUSSAN CO., LTD. actively engages in new PB product development and relocation of aging shops. For its full-year earning guidance, the revenue, operating income & net income of KOBE BUSSAN CO., LTD. are expected to rise 5.5% to ¥281.9 billion, 4.9% to ¥16.5 billion and 4.2% to ¥10.8 billion year over year respectively. The expansion of the “Business Supermarket` is planned to open additional 25 stores to reach 838 stores in total. KOBE BUSSAN CO., LTD. can enjoy huge economies of scale from vertical integration of food production & retail, and the expansion of store network. Recommend to buy at market price, target price ¥4321, cut loss if drop below ¥3975.

|

|

|

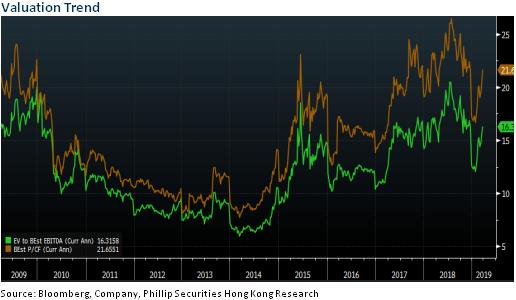

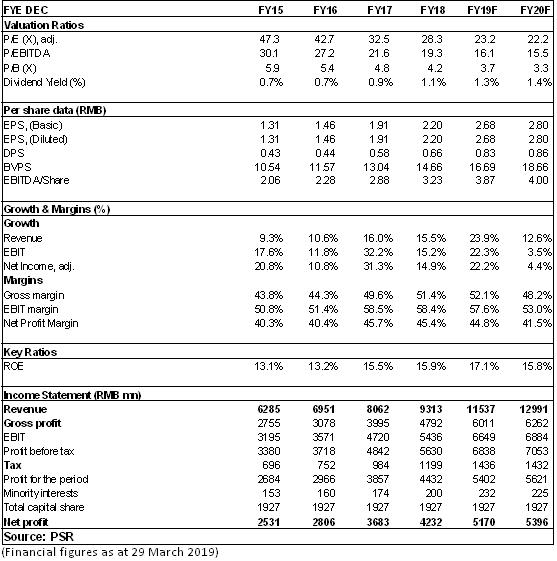

SIA (600009.CH) - Sustained Rapid Growth of Non-aeronautical Business

Rapid Growth of Results Shanghai International Airport (SIA) achieved a revenue of RMB9.313 billion in 2018, up by 15.5% yoy, and a net profit attributable to parent of RMB4.23 billion, up by 14.5% yoy, with a basic EPS of RMB2.2, slightly lower that our expectation by 7.7%. Its DPS was RMB0.66, with a dividend payout ratio maintained at 30%. Its weighted ROE rose to 15.85%, up by 0.32ppts. Steady Growth of Aeronautical Business In 2018, the traffic in SIA was controlled, with a recorded increase of less than 5% in aeronautical business (+3.6% for takeoffs and landings and +5.6% for passenger throughput). However, thanks to the price raising effect of the internal routes by domestic airliners and the scaling-up of international routes and wide-bodied aircrafts, the revenue from aeronautical business grew faster than the traffic, up to RMB3.969 billion, with an increase of 6.58% yoy, maintaining a steady growth on the whole. Sustained Rapid Growth of Non-aeronautical Business Unlike the restricted aeronautical business, the Company's non-aeronautical business recorded a sustained rapid growth up to RMB5.34 billion, with a surge of 23.2% yoy. Wherein, the commercial rental revenue increased by 33% yoy, up to RMB3.986 million, mainly benefiting from the increased proportion of international tourists with stronger consumption intention and the Company's sustained management, site optimization and adjustment of commercial retail brands. Of the commercial rental, over RMB3.5 million are from duty-free stores, the total volume and per customer transaction (RMB300/per customer) of which both recorded a rapid growth, with a growth rate of around 40% and 20% yoy, respectively, reflecting that duty-free stores in Pudong Airport were becoming a shopping hotspot for international routes passengers. Cost Growth Within A Stable Range Except its running cost, the Company's other costs were well controlled. Its total cost stood at RMB4.57 billion, up by 9% yoy. Wherein, the running cost grew rapidly to 1.91 billion, up by 28.6% yoy, and the labor cost increased by 7.5%, while other operating costs dropped by 14.1% yoy, mainly due to the expiration of depreciation period of fixed assets and the non-bond interest expense of the current period. The raise of entrusted management fee due to the scaling-up of duty-free store business and the increase of one-off maintenance expense contributed to the growth of operating costs. Settlement of Duty-free Bidding Allowing the Growth of Non-aeronautical Business In September, 2018, SIA entered into a new tax-free contract with Sunrise Duty Free, in which its minimum guaranteed commission will be RMB41 billion during the seven years from 2019 to 2025, deduction rate will be 42.5%, and its duty-free area will increase from 6,600km2 to 16,915km2, with a substantial increase of 156%. We believe that, under the tide of consumption upgrading driven by outbound tourism, the tax-free business will allow the Company's non-aeronautical business to grow, which will not only provide a solid foundation for the Company's next round of development, but also, hopefully, launch a new business operation pattern that will fully release the valuation premium of the Company as a leading hub airport. Investment ThesisConsidering the Company riding on the new round of stable growth period, we revise the Company's EBITDA per share in 2019 and introduce 2020E EBITDA per share. The target price is increased to RMB 67, with the estimation of a 17.3/16.8x multiple respectively during the two years, and the "Accumulate" rating is maintained.

�Financials

Click Here for PDF format...

| Recommendation on 3-4-2019 | | Recommendation | Accumulate | | Price on Recommendation Date | $ 62.150 | | Suggested purchase price | N/A | | Target Price | $ 67.000 |

| |

|

|

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the “Group”) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products’ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

版權所有, 翻印必究。

Copyright(C) 2019 Phillip Securities (HK) Ltd. All Rights Reserved.

|