Investment Summary

Travelsky Technology is the largest provider of the aviation information systems in China, which developed systems, such as flight control, air ticket distribution, check-in, boarding and load planning, accounting, settlement and clearing system, and aviation logistic. Based on DCF valuation, we derived a TP of HK$25.47, implied a P/E of 25.2x and 22.4x in 2018/19F. We update to a “Buy” rating with a potential upside of 29.3%. (Closing price at 4 Apr 2019)

Operating profit significantly below forecasts due to the surge in costs

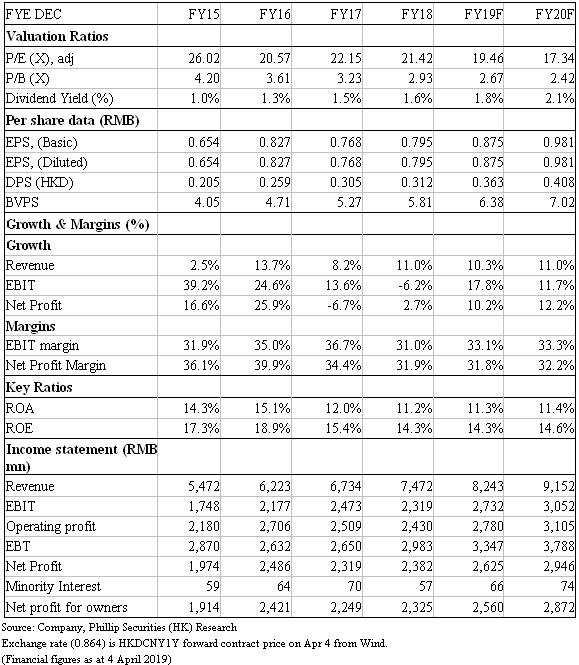

The Group announced its 2018 annual results, where the revenue grew by 11% to RMB 7.47 billion, generally in line with our estimates, just 0.79% below. In terms of segments, Aviation information technology services, Accounting, settlement and clearing services and Data network and others in 2018 was below our forecasts by 3.2%, 5.8% and 2.8% respectively, whereas System integration services was far above by 21.2%.

The operating profit dropped by 6.2% to RMB 2.32 billion, way below our forecasts, around 12.6%. The difference in operating profit is mainly attributed to the larger increase in cost than expected, such as technical support and maintenance fees, commission and promotion expenses as well as other operating expenses.

The management explained that the rise in commission and promotion expenses is due to the increase in commission rebate to airports and its third-party payment subsidiary as well as promotion expenses in the oversea distribution market. In relation to the rebate to airport and third-party payment subsidiary, as the rebate will grow corresponding to the volume, and there would be an increase in discount as the volume scales up. Regarding promotion expenses, since the oversea distribution market is open for competition, the Group will require to maintain its competitiveness by providing more promotions.

Besides, the rise in other operating expenses was caused by the relocation to new operating centre. It is believed the other operating expenses will remain at the current level, as there are additional expenses after moving into the operating centre, such as security expenses, water and electricity expenses and the property related cost, and the management team claimed the proportion of one-off expenses for the relocation was not that high.

In light of this, we expect to see commissions and promotion expenses as percentage of revenue increase in the future. As the distribution market of foreign airlines is opened for competitions and the flights of China Airlines further expand overseas, the Group will need to increase its investment in overseas distribution markets. On the contrary, we expect that other operating cost percentage of revenue will gradually decline in the future, because the operating costs of the operation centers are relatively fixed. As the revenue rises, it is believed that the proportion will also fall. As a result, we estimate that the decrease in the proportion of other operating costs is greater than the increase in that of commission and promotion expenses, we believe that operating profit margin will gradually improve.

Satisfactory operation data in January and February

The bookings on Chinese Commercial Airlines in January and February grew by 13.6% and 10.5% YoY respectively, and the aggregate growth was 12% YoY. The bookings on on Foreign & Regional Commercial Airlines dropped by 9.6% YoY in January, but rebound in February by 34.5% YoY, and the aggregate growth reached 7.4% YoY. The operation data shows that the growth of bookings on Chinese Commercial Airlines and Foreign Commercial Airlines remains strong.

Valuation

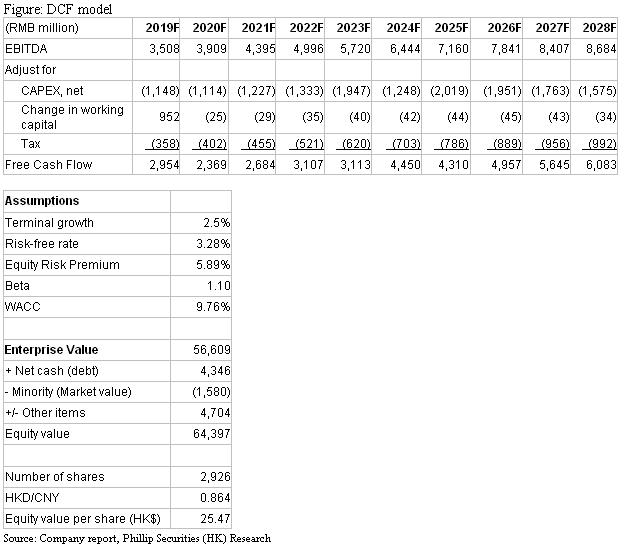

We adopted the DCF model for valuation, where we assume the discount rate to be 9.76%, and terminal growth to be 2.5%, with FCFF forecast to 2028F. We derived a TP of HK$25.47, implied a P/E of 25.2x and 22.4x in 2019/20F, 6.3% lower than our previous TP. In view of the plunge in stock price, we update to a “Buy” rating with a potential upside of 29.3%. (HKD/CNY=0.864)

Risk

1. Economic downturn

2. Aviation system market opening up

3. Airlines develop their own systems

Financials

Click Here for PDF format...