Investment Summary

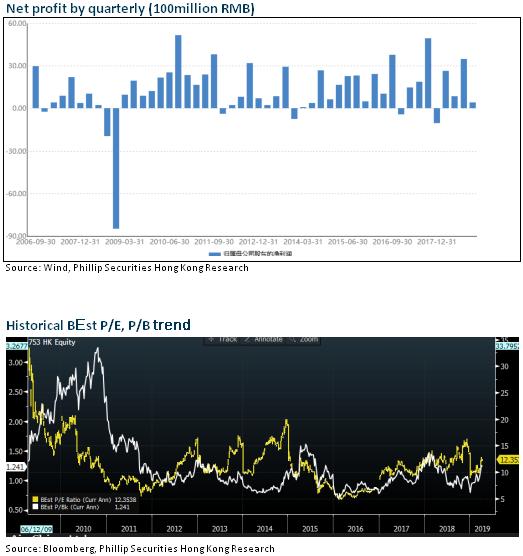

The 18Q4 Result Turns from Loss and the Year-round Net Profit Is Basically Flat Which Is Better than Expected

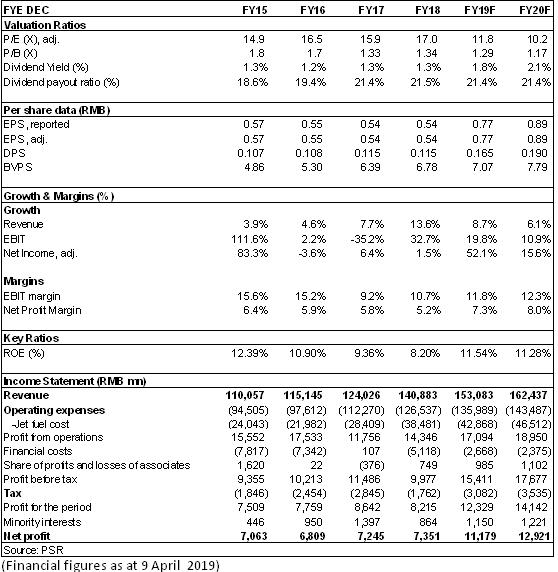

Air China reported revenues of RMB136.77 billion in 2018, up by 12.7% yoy. The net profit attributable to parent company was RMB7.34 billion, up by 1.3% yoy. Its EPS was RMB0.53 basically, down by 1.85% yoy due to the dilution of A share's private placement. Dividend per share was RMB0.1033, with the dividend rate of 19.5%.

The result of Air China in the 2018Q4 was better than expected, turning from a loss of RMB1.04 billion in the same period last year to a profit of RMB399 million. It was the main force to stop the downs and maintain the flat in the whole year (the net profit of the company in the first three quarters fell 16% yoy). We believe the main reason making the fourth-quarter result better than expected are:

1) Revenue: due to the market-oriented increase in ticket prices for key routes and the company's optimization strategy for capacity allocation, the Air China's RPK increased by 6% in the fourth quarter yoy, while its revenue rose largely by 14.6%.

2) Cost: although the fuel cost price increased by 35% yoy, the financial expense increased RMB767 million due to the devaluation of RMB. The operating costs increased by 13.1% yoy due to the good cost control, which was less than revenue growth.

3) The results of affiliated business turned well, which increased the investing revenue by RMB450 million, and other revenue and non-operating revenue increased by RMB655 million annually.

The 2018FY Result Is Under Pressure of the Rising Oil Prices and the Exchange Losses

The result of Air China's cost was still significantly depressed due to the oil prices and exchange in the whole 2018. The fuel cost increased by 35.5% (or RMB10.07 billion) yoy. The exchange loss recorded RMB2.38 billion, while it recorded a profit of RMB2.94 billion in the same period last year. Fortunately, the market-oriented increase in ticket prices, the structure optimization of aircraft allocation under the control of transport capacity, cost control and other measures improved the company's profitability of its main business. The revenue of RPK and unit freight per ATK increased by 2.9% and 5.4% to RMB0.5461 and RMB1.4312, respectively.

In addition, because the result of Cathay Pacific turned from loss to profit. The Company recognized the investing incoming of RMB202 million, and the losses in the same period of last year was RMB986 million.

At the end of the period, the Company's asset-liability ratio decreased by 1 ppts to 58.75%. The cash and cash equivalents reached RMB6.76 billion, accounting for 28% of current assets. The proportion of dollar liability in interest-bearing debts continued to decline from 41% on the end 2017 to 30%.

The Trend of Tight Balance between Supply and Demand Is More Obvious and The External Conditions Are Generally Positive in 2019

From the perspective of transport capacity in the industry, in order to ensure the punctuality rate of flights and the safety of aviation, the regulatory authorities still maintained strict control over the time limits of civil aviation resources. However, the grounding of Boeing 737MAX aggravated the trend of further contraction of industry supply. The May Day holiday and Beijing International Horticultural Exposition this year will have a positive pulling effect on aviation demand. Under the circumstance of tight balance between supply and demand, the prosperity of the industry is expected to continue to rise.

At present, the international oil price has fallen sharply compared with the same period, and the pressure of fuel cost of aviation enterprises has been greatly alleviated. The trend of rapid depreciation of RMB has been curbed. And Air China's dollar liabilities have fallen to 30%, and flexibility of exchange rate has continued to drop.

Valuation & Investment thesis

According to the latest hypothesis of the oil cost and exchange rate, we revised our estimate 2019/2020 net profit of AC to be 11.18/12.92 billion RMB. The target price is adjusted to HKD11, estimates 12.7/11x P/E and 1.38/1.26x P/B in 2019/2020. “Accumulate” rating is given. (Closing price as at 9 April 2019)

Risk

Traffic demand languished for the deterioration of macro-economy;

The depreciation of the RMB against USD would bring exchange loss;

Oil prices rose exceeded forecast.

War, terrorist attacks, SARS and other emergencies;

Highspeed railway diversion

Financials

Click Here for PDF format...