|

O-NET TECH GP(877)

Analysis:

According the announcement of O-Net Technologies (877), the unaudited revenue for the three months ended 31 March 2019 was approximately HK$642 million, an increase of 20.1% compared with the same period in 2018. The revenue in the first quarter was driven by strong demand from early adopters of 5G in Korea and Japan where the Group has entered into multi-year strategic agreements. Demand for optical networking components appeared to have bottomed in the first half of 2018, with a notable uptick in the second half of the year. Major telecommunication operators are expected to begin significant investments in 5G infrastructure as early as 2019. Unlike the 4G cycle, the 5G cycle is likely to happen more gradually and over a longer period of time, which may improve the Group's visibility into future demand. Due to the hardware requirements of 5G, infrastructure density will likely increase, creating opportunities for optical component manufacturers to boost volumes. (I do not hold the above stock)

Strategy:

Buy-in Price: $4.40, Target Price: $4.80, Cut Loss Price: $4.20

|

HOPEWELL INFR(737)

Analysis:

The group operates two expressway in the Guangdong Province; GS Superhighway which connects Guangzhou, Shenzhen and Hong Kong, and Western Delta Route, connecting Guangzhou, Zhuhai and Macau. Both traffic volume and toll revenue of the GS Superhighway recorded a lower single-digit decline due to short-term diversion impacts caused by newly opened highways in the adjacent areas; whereas the traffic volume and toll revenue of the Western Delta Route recorded a double-digit growth benefitting from the truck restrictions imposed on Foshan Ring Road. In addition, following the opening of the HZM Bridge in October 2018, passenger and cargo transportation has picked up on the Western Delta Route. Moving forward, with further economic integration between cities in the Greater Bay Area, Hopewell Infrastructure will stand to benefit from the increased in traffic volume, as both the GS Superhighway and Western Delta Route provide essential connectivity to major economic hubs in the area. The stock is currently trading with an attractive yield of 7.75% (excluding special dividend), the house believe investors would benefit from both the stable dividend cash flow and the potential to ride on the upside propel by rising traffic volume in the Greater Bay Area.

Strategy:

Buy-in Price: $4.10, Target Price: $4.60, Cut Loss Price: $3.90

The iShares Evolved U.S. Media and Entertainment ETF ( IEME )

The iShares Evolved U.S. Media and Entertainment ETF is an actively-managed, thematic ETF, with market cap of approximately USD 5.54 million and expense ratio of 0.18%. The fund offers exposure to U.S. companies with media and entertainment including various content providers to streaming-video service providers. More traditional media giants have planned to engage into the streaming-video market. Disney, AT&T and Apple will join Amazon and Netflix with services featuring original content. The success of market leader, Netflix can be greatly attributed to its popularity of original content library. In order to drive subscribers` growth in growing crowded market, it is necessary for Disney, AT&T, Apple and other streaming-video providers to create content library through M&A. According to a 2018 report from Park Associates, 36% of U.S households with broadband have two or more OTT subscriptions. It is believed that the streaming market won`t be a zero-sum game because consumers likely subscribe multiple services. Therefore, investors can capitalize the growth of streaming-video market via IEME. Recommend to buy at $27, target price $30.97, cut loss if drop below $26.46.

|

|

|

China Education Group (839.HK) - Acquisition of the remaining equity interest of Quancheng University; the issuance of a HK$2,355 million convertible bond

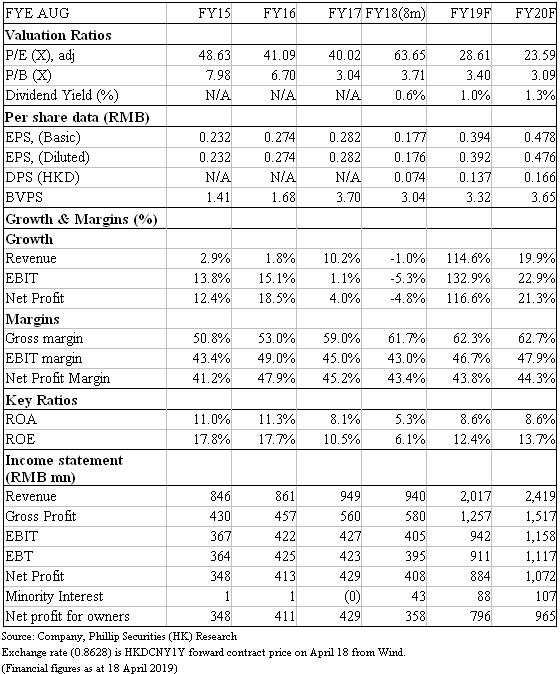

Investment SummaryChina Education Group has engaged in higher and vocational education. Under the management of the Group which are experienced in operating schools, we believe the potential improvement will be huge for the new acquired schools. Besides, the low cost financing has ensured the acquisition in the future, so the growth from acquisition should remain strong. Based on the net profit attributable to owners in 2020, we assume a P/E ratio of 28x (the average of the past), deriving a TP of HK$15.50 and maintain an “Accumulate” rating, with a potential upside of 18.68%.(Closing price at 18 Apr 2019) Business UpdateOn Mar 20, the Group has announced to acquire the remaining 49.09% equity interest of Quancheng University at a total consideration of RMB 223 million. In 2018, the net profit after tax was RMB 0.4 million, with total assets of 778 million and net assets of 377 million. Quancheng University is located in Penglai city, Shandong province, and the Independent college of Jinan University. Currently, there were 38 Bachelor degree programs, 9 Junior College programs, covering a wide range of disciplines including Economics, Management, Literature, Science, Engineering and Arts. The student enrollment in 2018 were 8,529, in which about 6,900 were Bachelor-degree students. The tuition of the bachelor-degree program and junior college program were RMB 11,000 per year and RMB 8,000 per year respectively. Among those independent colleges in Shandong, the admission marks for bachelor-degree in 2018 (science track) were the highest, 454. Besides, the tuition of the bachelor-degree program was only RMB 11,000, lower than the average of private universities and independent colleges in Shangdong (RMB 13,500), meaning there will still be room to grow. Finally, the utilization of the school was just 86%, and the remaining space available can further accommodate about 1,400 students. The maximum capacity of the campus is approximately 23,000 students more after the renovation and building new dormitories. Thanks to the potential increase in tuition and student enrollment, we believe it is a satisfactory acquisition target. On Mar 21, the Group announced the issuance of a HK$2,355 million five-year convertible bond with an annual interest rate of 2% and a conversion price of HK$14.69 per share, representing a premium of 30% based on the closing price of the share price at the end of the trading period on March 21, 2019 (HK$11.30). We think the bond issuance manifested the advantages of organized schools-running activities. Although the higher education industry are stable with an abundant cash flows, it is also capital-intensive. Therefore, they usually developed relying on debt financing. But, the interest rate was very high for those schools which are relatively weak in terms of balance sheet. This issues has reflected the advantages of organized schools-running activities, which could reduce geographical risk by running schools in different region. Moreover, it could enjoy a economies of scales thanks to its large scale, leading to the reduction in operating cost. As a result, they usually enjoy a lower financing rate. Besides, the the conversion price with high premium also reflects the optimistic views in stock price for the lender. The previous gearing ratio target the Group provided was 40%-50%. We expect the gearing ratio will reach 35%-40% after this issuance of bonds, implying that there will still be room for further financing. In addition, as it is the convertible bonds to be issued, the gearing ratio may reduce once the conversion is done, enabling the Group for another financing. Assuming the acquisition price of an new school takes RMB 600-700 million, the capital financed will be enough for acquiring 3 new schools. ValuationUnder the management of the Group which are experienced in operating schools, we believe the potential improvement will be huge for the new acquired schools. Besides, the low cost financing has ensured the acquisition in the future, so the growth from acquisition should remain strong. Based on the net profit attributable to owners in 2020, we assume a P/E ratio of 28x (the average of the past), deriving a TP of HK$15.50 and maintain an “Accumulate” rating, with a potential upside of 18.68%.(HKD/CNY=0.8628)

Risk1. A plunge in birth rate in China 2. A sharp change in policies to education sector 3. The Group fails to improve the operation of the acquired schools Financials

Click Here for PDF format...

| Recommendation on 24-4-2019 | | Recommendation | Accumulate | | Price on Recommendation Date | $ 13.060 | | Suggested purchase price | N/A | | Target Price | $ 15.500 |

| |

|

|

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the “Group”) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products’ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

版權所有, 翻印必究。

Copyright(C) 2019 Phillip Securities (HK) Ltd. All Rights Reserved.

|