Investment Summary

China Maple Leaf Education Systems Limited is a leading international school operator, from preschool to grade 12 education (K-12) in China. Although the valuation lifted recently thanks to the rumor of a looser regulation on “Education Promotion Law”, we believe that even if there are any difference in regulations compared with "Draft for deliberation ", the main content will not change much. Therefore, the business risk on compulsory education and kindergarten are still very high. As a result, we downgrade the rating from “Neutral” to “Reduce”, with a TP of HK$ 3.78, 10.8% potential downside. (Closing price at 25 April 2019)

Business Update

The group announced that as of March 31, 2019, the number of students enrollment was 41,380, an increase of 38.0% over the same period last year and an increase of 13.2% from October 15, 2018. During the period, the Group acquired a 66% equity interest in a primary and secondary school in Luzhou, Sichuan Province on December 10, 2018 at a consideration of RMB 185 million. The consideration will be paid in cash and allotment and issuance of new shares of the Group to the Vendor. Subsequently, on December 27, 2018, the Group increased its shareholding of 9% by RMB 25.2 million, which lifted the total equity interest held by the company to 75%. The school enrollment was about 3,200 and the school can accommodate a total of 3,500 students. The annual tuition fee ranges from RMB 20,000 to RMB 25,000. In 2018, 4 out of 5 highest scoring students of Luzhou municipal middle school exam were from this school, implying the quality of school education.

Policy risks

It is reported that “Education Promotion Law” will be legislated this year. We believe that even if there are any difference in regulations compared with "Draft for deliberation ", the main content will not change much. For example, there will a non-profit and For-profit classification for private schools, non-profit schools will receive the same benefits as public schools, compulsory education does not allow to choose for-profit and private education should be a supplement to public education.

From a practical point of view, if the non-profit and for-profit classification needs to be implemented literally, the first thing the government needs to resolve is the problem that the compulsory education school will be profitable in the name of non-profit. If the compulsory education school still allows to make use of the legal loopholes to distribute dividends to shareholders, and at the same time continue to enjoy the benefits as a non-profit school, higher education schools may adopt the same method to its maintain non-profit status and will have lower incentives to shift to for-profit status, making the classification failed to perform.

In addition, if there are still legal loopholes in the industry that allow schools to make profits in the name of non-profits, it will certainly lead to a unfair competition to higher education schools that have been shifted into for-profits, and they may therefore protest.

Therefore, we see that the probability of the policy to be implemented literally is very high, business risks on the compulsory education and kindergarten of the Group shall be very large, and even need to spin off to the corporate structure.

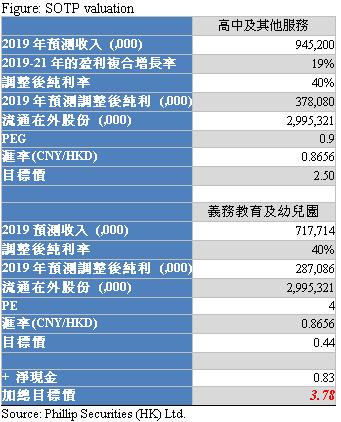

Valuation

Although the valuation lifted recently thanks to the rumor of a looser regulation on “Education Promotion Law”, we believe that even if there are any difference in regulations compared with "Draft for deliberation ", the main content will not change much. Therefore, the business risk on compulsory education and kindergarten are still very high. It is very likely that the business will not be able to pay dividends to shareholders in the future. However, since it is generally believed that there will be five-year grace period, we assume that compulsory education and kindergarten business spin off five year later. We maintain 4x P/E ratio for the business to reflect its value before divestiture.

Owing to the satisfactory growth in school enrollment, we increased the CAGR on adjusted net profit in 2019-21F to 19%, with 0.9x PEG, reflecting the increase in the effective tax rate and the payment of land transfer fees after the high school segment turning into for-profit.

We derive a TP of HK$3.78, 11.8% higher than the previous TP to reflect the satisfactory growth in school enrollment. However, as the stock price goes up recently, we downgraded the rating from “Neutral” to “Reduce”, with a potential downside of 10.8%. (CNY/HKD = 0.8656)

.Risk

1. VIE structure prohibited in China

2. The grace period of policies is shorter than expected

3. New acquired schools were not able to add value

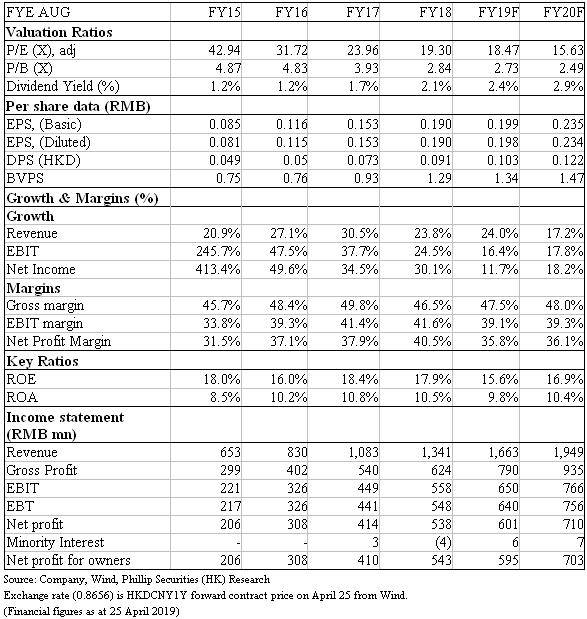

Financials

.Click Here for PDF format...