Investment summary

Nearly 50% Decrease in Earnings Last Year

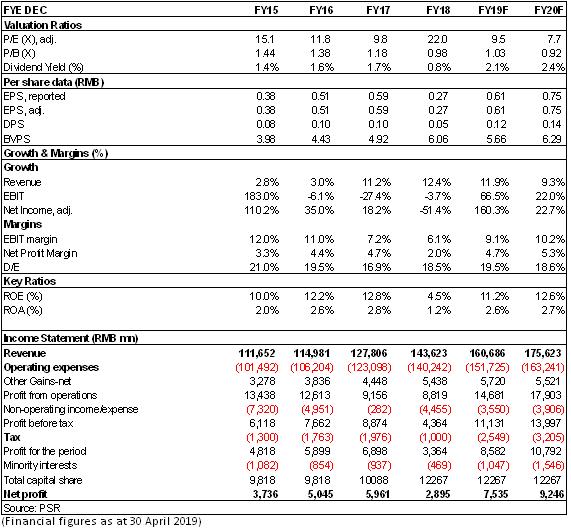

In 2018, the Company recorded a revenue of RMB143,623million, up by 12.66% Y-o-Y. The net profit attributable to the parent company was RMB2,983 million, down by 49.56% Y-o-Y; the net profit attributable to parent company excluding non-recurring items was RMB2,342 million, down by 55.07% Y-o-Y; EPS was RMB0.28, down by 53% Y-o-Y. The decline in performance was mainly due to fluctuations in oil prices and exchange rates in 2018. The dividend per share was RMB0.05, with a payout ratio of 18%.

Increase in Overall Yield

Benefiting from the fares reform and tight industry supply, the revenue per RPK was RMB0.54, up by 1.89% over the same period last year, of which the domestic routes was RMB0.49, up by 1% Y-o-Y. In the whole year, CSA transported nearly 140 million passengers, up by 10.8% Y-o-Y; the P L /F was 82.44%, up by 0.23 ppts Y-o-Y. The cost per ATK (excluding aviation fuel costs) decreased by 3.80%.

Decline Due to Fuels and Foreign Exchange loss hampered 2018FY Result significantly

In 2018, the fuel cost of CSA jumped by 34.57% or RMB11.03 billion Y-o-Y to RMB42.9 billion, contributing 64% to the increase in the operating cost. In addition, due to the expansion of the fleet size and the increase in the transport volume, the maintenance costs, depreciation expenses and operational services expenditure increased by RMB830 million, RMB1.15 billion and RMB1,444 million, respectively. The final operating cost increased by RMB17,144 million Y-o-Y, offsetting the revenue growth of RMB15.82 billion. Therefore, the operating profit decreased by 3.7% Y-o-Y to RMB8.82 billion.

In 2018, the Company recorded an exchange loss of RMB1,853 million, while in 2017, it recorded an exchange gain of RMB1.8 billion. The exchange affected the pre-tax profit by RMB3.65 billion.

Good performance for 2019Q1 result even under a High Base

In 2019Q1, the Company recorded a revenue of RMB37,633 million, up by 10.36% Y-o-Y. The net profit attributable to the parent company was RMB2,649 million, slightly up by 4.13% Y-o-Y; EPS was RMB0.22, down by 12% Y-o-Y, mainly due to the dilution of the private placement. The performance was better than expected, mainly due to the fall in oil prices, the stabilization of the exchange rates and the higher fares in 2019.

In 2019Q1, CSA's transport capacity /traffic volume increased by 11.3%/11.9% Y-o-Y, and the P L /F was up by 0.5 ppts Y-o-Y, of which the domestic routes saw an increase by 10.4%/10.2% in terms of transport capacity /transport volume with the same P L /F while the international routes saw an increase by 13.4%/15.2% and the P L /F was up by 1.3 ppts.

With the drop of oil prices, the cost pressure of CSA in the first quarter was greatly reduced, and the fuel cost was up by 9.5% Y-o-Y. At the same time, the RMB exchange rate has stabilized and appreciated slightly, thereby generating exchange gains, which will also help ease financial pressure.

Exchange Leverage was enlarged, with Cost Reduction and Efficiency Increase

As a result of the implementation of the new accounting standards, the aircrafts under operating lease were credited in the balance sheet, the asset-liability ratio increased by 5.6 ppts to 73.9% from the beginning of the year, and the increase in the proportion of USD-denominated debts increased the flexibility of performance to the exchange rate.

On the cost control, the Company plans to add 1704 seats through wide-body cabin renovation this year so as to continue to dilute the cost of ASK; in terms of aviation fuel cost management, it has set up a special team for aviation fuel cost control; Preference is given to more efficient domestic routes in terms of transport capacity. We expect that the unit non-oil costs will still have a room to fall in the future.

At the end of 2018, the Company had a fleet of 840 aircraft, a net increase of 86 aircraft in the year. From 2019 to 2021, the Company plans to increase the number of aircraft by 69, 63 and 26, respectively.

Investment thesis

As the overall external factors such as fuel price and RMB exchange ratio tend to stabilizing, we expressed cautious optimism for the promotion of the industry next year.

In accordance with the latest data, we adjust the estimate of the Company's EPS to RMB0.61/0.75 in 2019/2020. The target price is HK$7.5, equivalent to 10.4/8.5x and 1.13/1.01x estimated P/E ratio and P/B ratio, respectively, in 2019/2020. The "accumulate" rating is maintaining. (Closing price as at 30 April 2019)

Risk

Traffic demand languished for the deterioration of macro-economy;

The depreciation of the RMB against USD would bring exchange loss;

Oil prices rose exceeded forecast.

War, terrorist attacks, SARS and other emergencies;

Irrational inter-industrial price war;

Financials

Click Here for PDF format...