Investment Summary

NetDragon mainly engaged in gaming and education. The group announced its annual results, where revenue increased by nearly 30%, and net profit turned into a profit from a loss. In the future, the Group will try to monetize its education business in order to become profit-making. Besides, the new game “Vow of Heroes” will be launched in 2019. We adopted sum of the parts valuation, deriving a TP of HKD 30.22, and reiterate a “Buy” rating with a potential return of approximately 51.1%. (Closing price at 6 May 2019)

Annual result update

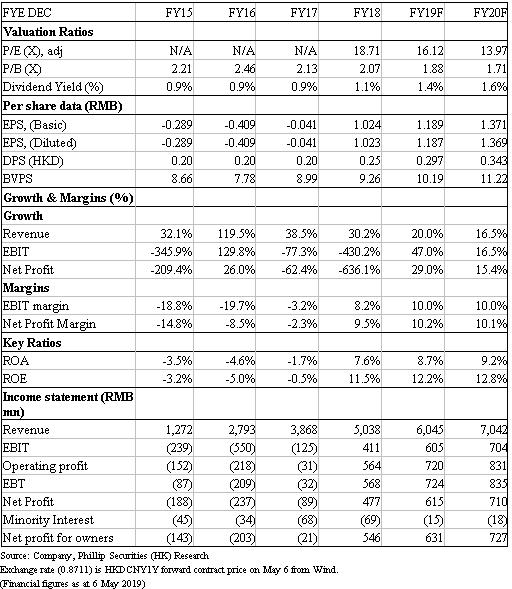

The group announced its annual results. During the period, revenue increased by nearly 30% to RMB 5.04 billion; net profit turned into a profit from a loss, recording RMB 480 million.

Gaming revenue jumped by 41.5% to RMB 2.37 billion, and gross profit margin increased by 2% YoY. Among them, the revenue of PC gaming rose by 39.8% to RMB 1.92 billion, mainly benefiting from the new expansion packs and new functions launched by the classic game “Eudemons Online”, where the highest monthly gross billing reached RMB 150 million. Mobile gaming revenue reached RMB 450 million, up 49.3%. In the second half of 2018, the pocket version of “Eudemons Online” and “Eudemons Online Mobile” recorded an average monthly gross billings RMB 100 million in total. The average monthly revenue per user of the group also increased to RMB 665, a significant increase of 64.8% YoY.

Education revenue increased by 21.9% to RMB 2.57 billion, and gross profit margin increased by 1.9% YoY. Among them, the progress of Prometheus was doing well, with revenue growth of 25.9% to RMB 2.2 billion; net profit also increased significantly to RMB 150 million, mainly due to the increase in ASP of products and stronger growth than the overall K12 interactive display market. In addition, the group acquired a learning community platform Edmodo in 2018. Currently, the total number of users of the platform reaches 100 million.

Education

In relation to oversea, Prometheus continued to innovate, launching a new generation of interactive whiteboard V7, and won the Red Dot Design Award. As the product's functionality becomes more mature, it helps to improve the product ASP and competitiveness. In addition, Prometheus will further enhance its monetization capabilities by providing an application platform for its own products. Edmodo will also launch more monetization plans this year. The Group expects to launch a homework helping service in the second half of 2019 and will charge monthly. In the future, the platform will also monetize by providing high-quality tutorial contents. Currently, the platform has nearly 700 million tutorial resources. Regarding domestic, although 101PPT is still loss-making, the primary goal of the product is to increase the number of user and their stickiness. As of 2018, the number of 101PPT users reached 5 million, a significant increase from last year (1.2 million). In the future, we believe that the Group can monetize by providing high-quality tutorial contents.

Gaming

Since the grant of licence approval was resumed in the end of 2018, three games were granted the approvals, including “Eudemons (PC-Moblie Cross Platform Version)”, “Eudemons Legends” and “無境戰地”. Besides, there are 8 games in the pipeline which are about to be launched or under development, such as “Vow of Heroes”, “Eudemons II”, “Heroes Evolved Thrones”, “Battle of Giants” and etc. “Vow of Heroes” is a JRPG mobile game, where the characters and card paintings are drawn by Japanese “Painting Hall”, with gorgeous battle screens as a selling point. The first round of testing of the game has been launched, and was rated 7.8 in the platform TapTap, representing a good response from the users. We expect the game to be officially launched this year and will add momentum to mobile gaming revenue growth. In addition, the group will continue to monetize its classic IP "Eudemons" and "Heroes Evolved", by launching "Eudemons Century", "Eudemons Legends", "Heroes Evolved", "Heroes of Ages" and other adaptation games. At the same time, the group said it will launch a new Season pass payment model, with new heroes and new gameplay in "Heroes Evolved", in an attempt to improve the ARPU and keep the game fresh.

Valuation

We adopted sum of the parts valuation and forecast the earnings per share of the gaming business in 2019F to be RMB 3.02, with target PE ratio 8x. As the education business is still loss-making, PS ratio will be used for valuation. We predict the revenue per share of the education business in 2019F to be RMB 5.71, with target PS ratio 2x. With RMB 2.64 net cash per share in 2018, we derive our TP to be HKD 30.22, maintaining a “Buy” rating, implying 35% potential upside. (CNY/HKD=0.8711)

Risk

1. Edmodo integration progresses slowly

2. Overseas acquisition fails

3. Gaming revenue growth slows down

4. Policy risk on gaming industry

Financials

Click Here for PDF format...