First-quarter Net Income Rose 37%

SIA recently released its 2019Q1 resul: revenue reached RMB2.77 billion, increasing by 21.6% yoy; net profit attributable to the parent company reached RMB1.39 billion, up by 36.7% yoy, with a growth rate achieving the new peak over the past 8 years; and its non-attributable net profit deducted reached RMB1,343 million, increasing by 32% yoy. The basic EPS was RMB0.72. Cash flow from operating activities nearly doubled, reaching RMB978 million and increasing by 96% yoy, and the yield of weighted net assets increased by 0.84ppts.

Aeronautical Business Maintained Small Growth

The latest operation data showed that, in2019Q1, SIA completed 126,900 aircraft movements, increasing by 2.4% yoy, and recorded a passenger throughput of 18,826,100 capitals, increasing by 4.9% yoy, among which, domestic passengers reached 9.22 million, increasing by 5.5% yoy, international passengers reached 7.9 million, increasing by 4.9%, and regional passengers reached 1.71 million, increasing by 2.3%. The cargo throughput was 804,900 tons, decreasing by 9.1% yoy. With the scaling-up proportion of wide-body aircraft, we expect the yoy growth of aeronautical business revenue to maintain a small-moderate single-digit growth rate.

Rapid Growth of Non-aeronautical Business Sustained

As of the first quarter of 2019, duty-free stores in Pudong T2 Terminal started to adopt the new royalty rate of 42.5%, increasing sharply by 17.5ppts from that of 25% of 2018. In the first quarter, this section contributed RMB1.01 billion to the revenue, equivalent to a turnover of RMB2.38 billion, which was estimated to drive an overall tax-free sales growth of 33% yoy approx. We believe that the improved deduction rate and substantial sales growth have boosted the profitability of the non-aeronautical business of SIA and were the main driving force for its strong performance in the first quarter. The Company's overall gross margin reached 55.24% in the first quarter, increasing by 4.5ppts from that of 50.7% a year earlier.

Expense Ratio Dropped and Investment Income Increased by RMB85 Million

In Q1, the Company's expense ratio dropped significantly, with the sum of sales, administration and financial expenses totaling RMB11.62 million, decreasing by 53% from that of RMB24.77 million a year earlier. Cause for such drop mainly lies in the decrease of current operating costs of one subsidiary, the expiration of the depreciation period of fixed assets, and one-time expenses in the same period of the last year. In addition, due to the change of accounting method, the investment gains increased by 39% or RMB85 million yoy.

Non-aeronautical Business will be Improved After the Satellite Terminal Puts into Service

Satellite Terminal S1 and S2, the Phase III Expansion Project of Pudong Airport, is expected to put into service in September, 2019, which will increase a duty-free area of 9,062m2, and T1 and T2 Terminal will offer a new duty-free area of 1,000m2, which is expected to enhance the shopping experience of passengers while expanding the area of its duty-free business, so as to fully release the premium valuation of the Company as a leading hub airport.

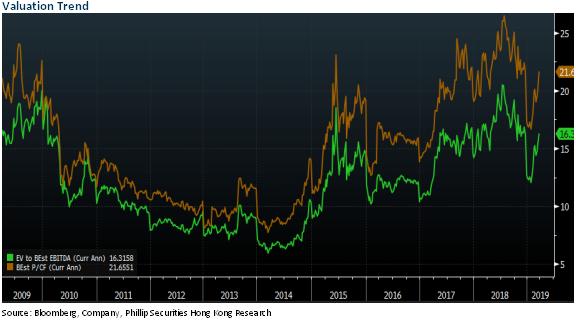

Investment Thesis

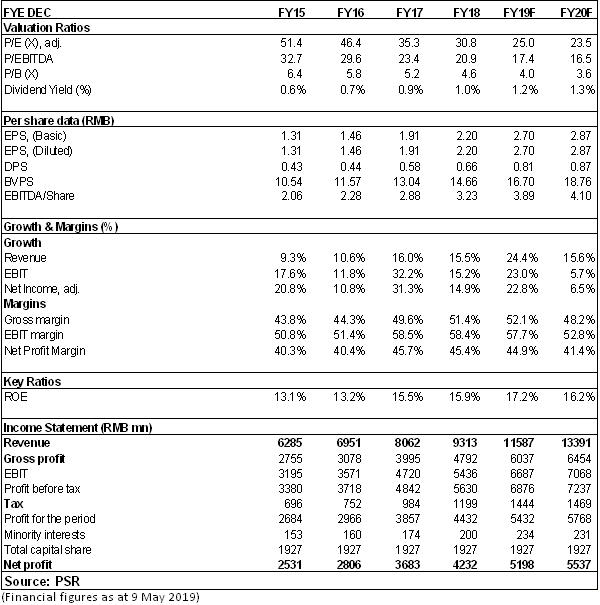

Considering the Company riding on the new round of stable growth period, we revise the Company's EBITDA per share in 2019/2020 E EBITDA per share. The target price is increased to RMB 74, with the estimation of a 19/18x multiple respectively, and the "Accumulate" rating is maintained. (Closing price as at 9 May 2019)

Financials

Click Here for PDF format...