Investment Summary

CNHEG announced its 2018 results. During the period, organic growth was strong, and tuition and accommodation fees increased steadily, but the debt ratio jumped significantly, which may affect the progress of acquisition in the future. In addition, Chinese Premier Li Keqiang mentioned in the government report that there will be a one million enrollment expansion for higher vocational colleges in 2019. At the same time, the State Council also announced the “National Vocational Education Reform Implementation Plan”, hoping to improve the quality of higher vocational education. Based on the DCF model, we derive a TP of HKD4.26, and giving a “Buy” rating, with 35.7% potential upside. (Closing price as at 14 May)

Company Update

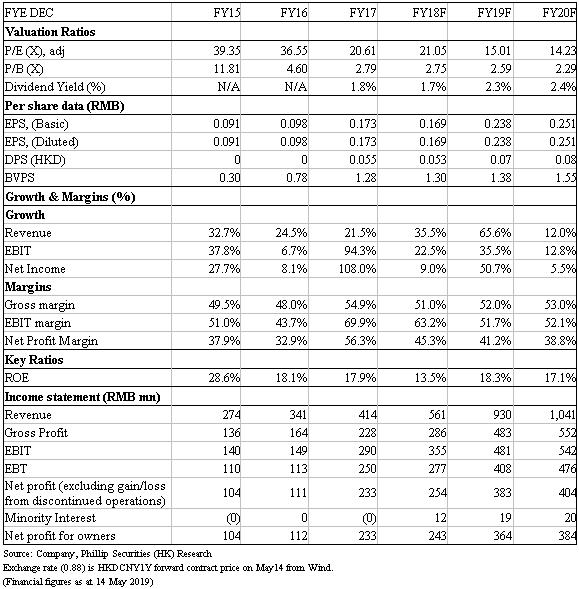

The Group's revenue in 2018 was RMB 561 million, a YoY increase of 35.5%, mainly due to the excellent organic growth of students in Yunnan and Guizhou, the higher average Accommodation fee per student and the consolidation of Henan and Northeastern schools. The net profit attributed to the owner was RMB 243 million, up 3.9% YoY, mainly due to the provision for the termination of the acquisition of Xinjiang schools. If this provision, listing fees and exchange gains are deducted, the adjusted net profit is RMB 285 million, a YoY increase of 20.3%.

During the period, the number of students in Yunnan and Guizhou schools increased by 13.7% to 44,583; the number of students in Northeast, Central China and Henan schools increased by 17.1% to 39,012. Among them, the number of students in Central China and Henan schools increased by nearly 50% and 16% respectively, but the number of students in Northeastern schools dropped slightly by 1%. It can be seen that the organic growth for those schools is strong. The number of students in Gansu and Guangxi schools is 8,218 and 9,953 respectively.

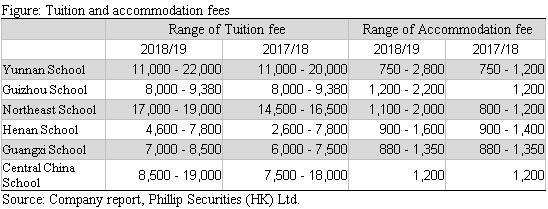

In terms of tuition and accommodation fees, due to the improved dormitory environment in Yunnan and Guizhou, the average accommodation fee per student has increased by 9.9% this year. Except for Guizhou schools, the tuition fee range of each school has also increased in the 2018/19 academic year. The average tuition fee is expected to be RMB 9,947, an increase of about 5% from the previous year's RMB 9,492.

Termination of the acquisition of Xinjiang schools

In October 2018, the group announced the termination of the acquisition of the Xinjiang University of Finance and Economics Business School because of local policy restrictions. As the group hopes to obtain the management fee of the school, it has paid RMB 148 million in investment prepayments for this acquisition. After the termination of the acquisition, the Group stated that the prepayment could become a bad debt, so an impairment provision of RMB 30 million was prepared for this year. However, the group expressed its confidence to recover the money.

Debt ratio driven up significantly

The Group's interest-bearing debts rose sharply in 2018, and the net interest-bearing debt-to-equity ratio rose sharply from 14% in 2017 to 41% in 2018. As a the growth of the current education sector mainly comes from acquisitions, the high debt to equity ratio indicates that the future group will not have much funds for the acquisition, implying a reduction in growth of the group. The Group also raised approximately HK$390 million in the form of a placing on April 10 this year, which is believed to help ease the Group's debt burden..

Industry Update

One million enrollment expansion for higher vocational education

Chinese Premier Li Keqiang mentioned in the government report that in 2019, the enrollment expansion for higher vocational education will be one million. The enrollment targets of higher vocational colleges are mainly ordinary high school graduates, secondary vocational graduates, social candidates (farmers, laid-off workers, retired military personnel, new professional farmers, etc.). In addition to enrollment expansion, the Ministry of Education has also introduced a number of policies to encourage the development of higher vocational education, such as: eliminating the higher vocational school enrollment ratio of secondary vocational graduates, higher vocational education graduates and ordinary college graduates enjoying the same treatment and the central government allocated RMB 23.7 billion for the modern vocational education quality improvement plan.

In addition, earlier this year, the State Council also announced the "National Vocational Education Reform Implementation Plan", hoping to improve the quality of higher vocational education, and by 2022 to build 50 high-level higher vocational schools and 150 professional groups.

Valuation

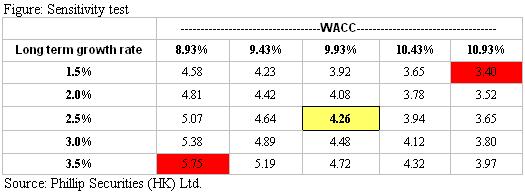

We adopted a three-stage discounted cash flow model, assuming the short and long term growth rate are 10% and 2.5% respectively, with 10 declining years and 9.93% WACC. According to the range for WACC [8.93%,10.93%] and long term growth rate [1.5%,3.5%], the highest and lowest target price are HKD5.75 and 3.40 respectively. Due to the dilute effect from new placing and the depreciation of RMB, we lower our TP to $4.26, implying a PE ratio of 15.8x and 15.0x in 2019/20. Owing to the slump in stock price recently, we update the rating to “Buy”, with 35.7% potential upside.

Risk

1. VIE structure prohibited in China

2. The faster than expected decrease in birth rate

3. New acquired schools were not able to add value

4. The Revised Draft of Law for Promotion of Private Education passed successfully

Financials

Click Here for PDF format...