|

|

CHINAGRANDPHARM(512)

Analysis:

China Grand Pharm announced that on March 11, 2019, the Committee on Foreign Investment in the United States (CFIUS) has issued a license for the company and CDH Genetech`s acquisition of Sirtex in accordance with relevant laws. Sirtex`s SIR-Sphere Y-90 resin microspheres have been inoculated with more than 86,000 doses in more than 1,160 treatment centers worldwide, and China currently accounts for more than 50% of global liver cancer patients, which will be a major market opportunity for Sirtex. At the same time, through this acquisition, the company can expand its business to the field of liver cancer treatment. The company has now assisted Sirtex in its commercialization in China, preparing to bring its leading treatment technology to patients in China. In recent years, China`s pharmaceutical regulatory agencies have successively issued a number of preferential policies to support, promote and accelerate the introduction and registration of therapeutic products with critically identifiable diseases in the international market. The company believes that this will benefit Sirtex products in the Chinese market, especially for the registration and approval, which will accelerate the launching and commercialization of products in China. In recent years, through the international development strategy, the company has continuously introduced international innovative treatment programs with development potential. It is expected that the company`s core competitiveness and operational efficiency can be further improved, and shareholders can also be beneficial from this.

Strategy:

Buy-in Price: $4.00, Target Price: $6.25, Cut Loss Price: $3.84

Tayca (4027.JT)

Founded in 1919 as an imperial artificial fertiliser which had sulphuric acid and superphosphate fertilizers as their main products. Carries out the manufacture and retail of chemical industry chemicals such as titanium oxide, surfactants, sulphuric acid, particulates of titanium oxide, surface treatment products and pollution-free anticorrosive pigments, etc. In recent years, they have been focusing their efforts on new fields, such as particulate titanium oxide for cosmetics and piezoelectric ceramics for ultrasonic echos, etc.・For FY2019/3 results announced on 9/5, net sales increased by 11.4% to 47.385 billion yen compared to the previous period, operating income decreased by 4.0% to 5.803 billion yen, and net income increased by 10.6% to 4.007 billion yen. Although sales of functional-use titanium oxide particulates and surface treatment products have performed strongly, rising manufacturing costs have been a burden. Extraordinary loss due to impairment has been recovered. For FY2020/3 plan, net sales is expected to increase by 9.7% to 52 billion yen compared to the previous year, operating income to increase by 17.2% to 6.8 billion yen, and net income to increase by 12.3% to 4.5 billion yen. Due to the increase in interest towards UV protection, we can expect the demand for titanium oxide particulates and zinc particulates to increase for UV cut agents. Also, the company has plans to carry out development of the South East Asian market. Recommend to buy at ¥2,050, target price ¥2,600, cut loss if drop below ¥1900.

|

|

|

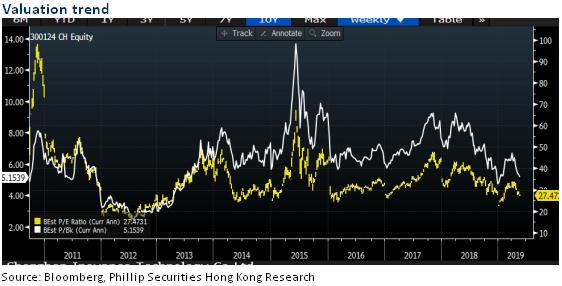

Inovance Technology (300124.CH) - 2019 Q1 is Likely to Be a Low Point for Result

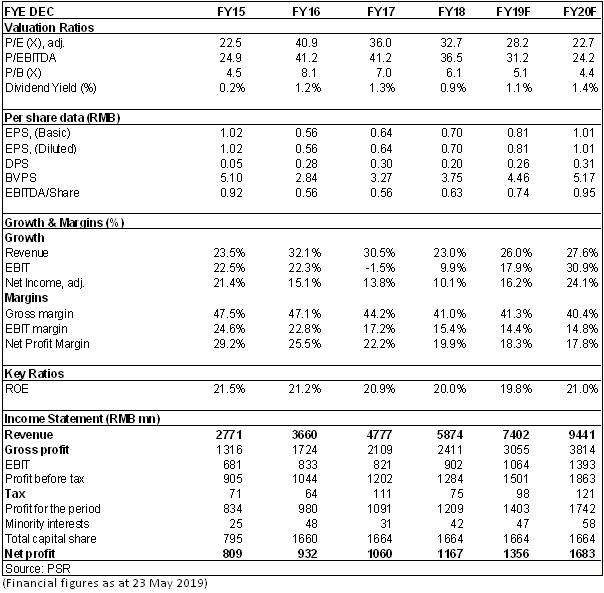

Investment SummaryRevenue Grows Rapidly and Net Profits Increase Steadily in 2018 In 2018, Inovance Technology reported net profits of RMB1.167 billion attributable to shareholders of the parent company, up 10.1% yoy, with EPS of RMB0.70 and dividends per share of RMB0.2. The result is lower than our expectations, mainly because 1) domestic macroeconomic downturn in the fourth quarter of last year affected downstream demand, 2) new energy bus market in the reporting period is still affected by the policy adjustment. The duration is longer than expected. However, by virtue of the Company's competitive advantages in many segments and the delivery of rail transit orders in the early stage, the Company's overall revenue still achieved rapid growth, with the annual revenue of RMB5.874 billion, up by 23% yoy. In terms of business, the revenue of the general segment reached RMB2.587 billion, up by 32% yoy. The elevator business reported revenue of RMB1.37 billion, up 22.34% yoy. Electro-hydraulic servo business reported revenue of RMB495 million, up 3% yoy. The new energy vehicle business reported revenue of RMB841 million, down 8% yoy. Rail transit revenue reached RMB212 million, up 112% yoy. In 2018, the Company's overall gross margin was 41.81%, down by 3.31 ppts yoy, mainly due to changes in the Company's product revenue structure and intensified industrial competition in 2018: (1) the price reduction of Yutong bus, the main customer, led to a decrease of 10.56 ppts in the gross margin of the new energy sector; (2) the sales structure of elevator business has declined, the market competition of automation business has intensified, and the gross margin has declined slightly. The Company has a good cost control, and its period cost rate is 25.46% (saving 0.96 ppts yoy), among which the proportion of research and development expenses is 12.12% (reducing 0.28 ppts yoy), still maintaining a high level of research and development expenditure. By the end of 2018, the Company has completed eight designated projects of domestic auto companies. In 2019, with the gradual increase of designated models, the electric motor control business of the Company's passenger cars will start to enter a period of high growth. Q1 of 2019 is Likely to Be a Low Point for Result In Q1 of 2019, the Company reported revenue of RMB1.10 billion, up 12.8% yoy, and net profit of RMB129 million, down 34.3% yoy. 2019 Q1 results fell, mainly because: 1. The decline in the revenue structure and increased competition in the industry reduced gross margin by 4.13 ppts yoy. 2. The amount of VAT software rebate received was reduced, resulting in a yoy decline of 46.77% in other income. 3. During the reporting period, the increase of personnel and the implementation of equity incentive led to the increase of expenses. 4. Exchange rate fluctuations led to increased investment losses in Qianhai Jingrui Hehui Financial Services Co., LTD. However, operating cash flow improved in Q1, from the outflow of RMB94 million to the inflow of RMB21 million in the same period of last year. In terms of business, sales revenue of automation business reported RMB503 million, up by 5.2% yoy. The integrated elevator business reported sales revenue of RMB241 million, up 12.35% yoy. Electro-hydraulic servo business and Yishitong business reported revenue of RMB106 million, down 14.59% yoy. Revenue from new energy vehicles reported RMB75 million, down 8.8% yoy. Rail transit business reported revenue of RMB83 million, up 655% yoy. Industrial robot business reported revenue of RMB21 million, up 38.5% yoy. Acquisition of BST Opens up Overseas Markets Recently, the Company announced that it planned to acquire 100% of BST by means of cash and equity, with a total transaction amount of RMB2.487 billion, corresponding to PS\PE\PB of 1.03, 10.57, 4.57 times. BST is a quality elevator parts supplier mainly serving foreign customers. BST's man-machine interface interaction system, wire and cable system, and other products are in a leading position among international brands of elevator manufacturers. It has stable cooperative relations with most of the world famous elevator manufacturers, including Otis, Kone, thyssenkrupp, Schindler and Fujitec, and has entered the global supplier system of some of them. Inovance Technology and BST are complementary to each other in terms of customers and products, with obvious synergies. By opening up the overseas market through BST, we will further expand the scale of overseas business and expand business development space. Investment ThesisT By the end of 2018, the Company had accumulated RMB1.38 billion of orders in hand, and the electric motor control business of passenger cars will gradually improve in 2019. The industrial control industry is expected to gradually bottom out and recover as PMI returns to above the 50-point line delineating growth from contraction. By opening up overseas elevator market, and the Company's result in 2019 is expected to grow steadily. As for valuation, we expected diluted EPS of the Company to RMB 0.81 and 1.01 of 2019/2020. And we accordingly gave the target price to RMB28.41, respectively 35/28x P/E for 2019/2020. "Buy" rating. (Closing price as at 23 May 2019)

Financials

Click Here for PDF format...

| Recommendation on 27-5-2019 | | Recommendation | Buy | | Price on Recommendation Date | $ 22.940 | | Suggested purchase price | N/A | | Target Price | $ 28.410 |

| |

|

|

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the “Group”) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products’ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

版權所有, 翻印必究。

Copyright(C) 2019 Phillip Securities (HK) Ltd. All Rights Reserved.

|