Investment Summary

SUNeVision is one of the leading carrier-neutral data center operators in Hong Kong, owned 74.04% by Sun Hung Kai Properties (16.HK). Robust growth of Cloud services lead to new demand to the high tier data centers, and the Group has a clear plan on supply for short, medium and long term. Therefore, we believe it will benefit from the rising popularity in cloud services. We derive a TP of HK$6.12. Due to the recent rally on stock price, we downgraded the rating to “Hold”. (Closing price at 27 May 2019)

Robust growth of Cloud services lead to new demand to the high tier data centers

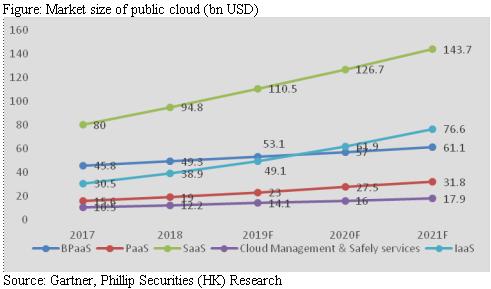

As the cloud services became mature in US, it is gaining popularity in Asia. Not only individual users, but also corporate users are open to this kind of services. According to Gartner, the market size of IaaS, PaaS and SaaS will reach 76.6, 31.8 and 143.7 bn USD in 2021F, representing a CGAR of 25%, 19% and 15%. Besides, the IT infrastructure has to be set up well before the cloud services became popular. As a result, the massive demand on data centers actually arrives before the popularity in cloud services. Moreover, in order to provide services in a high quality, cloud service providers will require a high tier data center which could provides high power density, high uptime and long power provision. Although there a number of data centers in the market, those high tier data centers are the one which could attract the cloud service providers moving in.

Mega Plus is a tier 4 data center, and the attractiveness of Mega Two and Mega-i to cloud services providers could be enhanced after the expansion and optimization work. The power density can lift by 40% after the optimization work. Besides, the new data center for the new project in Tseung Kwan O is believed to be a high tier data center, implying the group will be able to enjoy the robust growth of cloud services.

Clear plan on supply for short, medium and long term

In light of the data center industry characteristics of heavy assets, the supply takes time to build up, meaning the Group needs to prepare in advance to ensure the growth in the future even if there is a massive demand on data center coming later on. We see the Group has a clear plan on supply for short, medium and long term.

Regarding the short-term supply, the occupancy rate of Mega Plus is about 50% since the opening on Oct 2017. Based on the current progress, Mega Plus will be full in around 2021. Besides, the expansion and optimization work at Mega Two and Mega-i is expected to enhance the capacity of the Group.

In relation to medium and long term, the Group expects the project in Tsuen Wan will be finished in 2021-2022, while that in Tseung Kwan O in 2022-2023, but in several phrases.

Based on the projects on hand, we believe the supply from the Group will be able to meet the future demand, so it ensures the growth in the future.

The drop in GPM due to the pre-move-in expenses

The GPM of the Group dropped since 2016. Although we believe the drop was partly attributed to the more intensified competitive landscape, part of the drop was caused by the pre-move-in expenses. Before the clients move into the data center, the Group has to set up the equipment, such as UPS or air-conditioners. The equipment starts depreciating once they are ready, but the Group will receive no income until the client moving in. Therefore, the GPM will reduce during this period, but will resume to the normal once the clients move in. Currently, the occupancy rate of Mega Plus was around 50%, meaning the aforementioned situation will be very likely to continue in the future, so we expected the GPM will suffer a downward pressure.

Earnings forecast

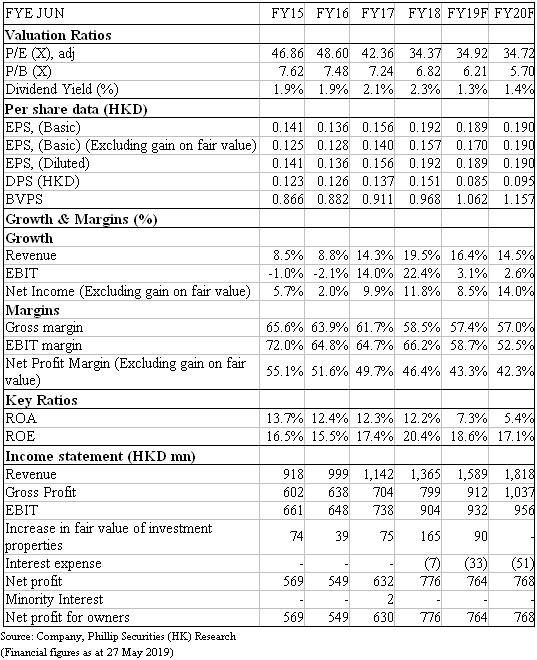

In view of the new capacity of the data center being sold well, we have lift the revenue growth forecast of 2019/2020FY to 16.4%/14.5%.

Valuation

Assuming 36x P/E in 2019F, we derive a target price of HK$6.12, up 5.2% than previous TP, due to the new capacity of the data center being sold well, implying 32.2x P/E in 2020F. As the stock price has rallied recently, we downgrade to the rating to “Hold”.

Risk

1. Slower than expected demand on data center

2. Significant increase in land supply for data centers within a short period

3. The entry of cloud service giant players to data center industry in Hong Kong

4. Loss on judicial review

Financials

Click Here for PDF format...