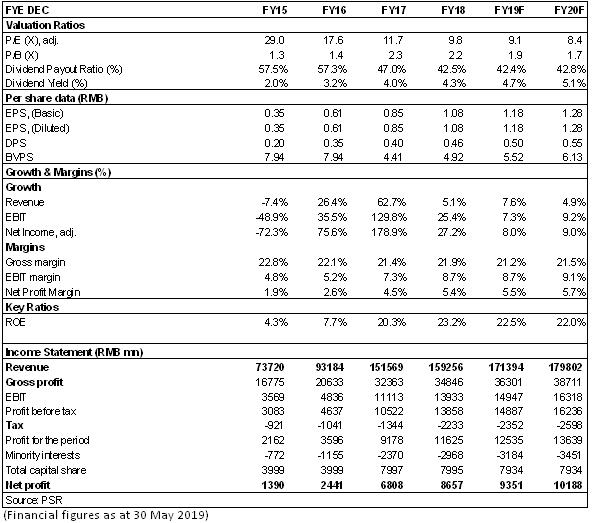

Net Profit Reached A New High in 2018, Increasing by Nearly Thirty Percent

In 2018, Weichai recorded an annual revenue of RMB159.3 billion, increasing by 5% yoy, and a net profit attributable to the parent company of RMB8.66 billion, increasing by 27% yoy. The basic EPS was RMB1.08, the dividend was RMB0.46 totaling the final dividend of RMB0.28 and the medium-term dividend of RMB0.18, and the dividend payout ratio was 42.6%. In addition, the Company spent nearly RMB500 million to re-purchase and cancel over 63 million A-shares, which accounted for 0.8% of the total share capital.

In 2018, Weichai sold 363,000 heavy truck engines in total, basically flat with the same yoy, and accounted for 31.6% of the market share, which remained stable (when compared to 27% in 2016 and 33.1% in 2017); its subsidiary, Shaanxi heavy-duty truck, sold 153,000 heavy trucks in total, increasing by 2.7% yoy and accounting for 13.3% of the market share; its another subsidiary, Fast, sold 909,000 transmissions, increasing by 8.9% yoy; and its overseas subsidiary, Kion, recorded an annual revenue of EUR8 billion, increasing by 5.2% yoy. The Company expects a sales revenue of RMB175 billion approx. in 2019, an increase of 10% approx. over 2018.

In the reporting period, three expenses and R&D expenses accounted for 13.36%, decreasing by 0.19 ppts yoy Vs 2017, among which, the sales expenses accounted for 6.67%, decreasing by 0.15 ppts, the administration expenses (including R&D expenses) was controlled at 6.64%, slightly increasing by 0.28 ppts yoy, and the R&D expenses accounted for 2.71%, increasing by 0.25 ppts. The Company continued to build its moat with high R&D investment. The Company repaid part of long-term debts, and the gearing ratio decreased by 2.6 ppts to 32.9%. Meanwhile, the ratio of financial expenses dropped by 0.34 ppts, benefiting from the increase of interest income from bank deposits.

In 2018, the Company's gross sales margin was 22.33%, increasing by 0.50 ppts when compared to that of 2017. The net profit margin increased from 6.1% to 7.3%, with further improved profitability. The Company's heavy-duty engine enjoyed a stable dominant position in the heavy truck market, 5-ton loader market and above-11m bus market.

Performance Continued to Grow at a High Rate in Q1 2019, Increasing by 35% yoy

In Q1 2019 Quarterly Report, Weichai recorded a revenue of RMB45.21 billion, increasing by 15.3% yoy, and a net profit attributable to the parent company of RMB2.59 billion, increasing by 35.0% yoy. When excluding non-recurring gains and losses, the net profit attributable to the parent company still increased by 23%.

In Q1, the development of the heavy truck industry in China was better than market expectation, with an increase of 0.6% yoy in industry sales to 326,000 heavy trucks, and the heavy truck sales of Q1 of the Company's subsidiary, Shaanxi heavy-duty truck, was far ahead of the industry average, with an increase of 20% yoy and an expected annual increase of 20% yoy. In Q1, the domestic construction machinery industry also witnessed a relatively rapid growth (with an increase of 24.5% yoy in excavator sales and 7.4% yoy in loader sales), which drove the Company's high-power engine sales to an ideal level.

In Q1, the Company invested RMB987 million in R&D, increasing by 20.31% yoy. The gross margin was 21.66%, decreasing by 1.43 ppts yoy. However, the ratio of financial expenses/sales expenses/administration expenses decreased, the fair value increased, and the impairment reduction increased by RMB487 million, with a final net profit rate up to 7.5%, increasing by 1.0 ppts yoy.

Continued to Benefit from the Increased Market Share

We expect that the future heavy truck engine business of the Company will continue to benefit from the upward trend in the sales structure resulting from upgrading consumption in heavy truck industry. And on the other hand, after the Company's chairman also served as the chairman of Sinotruk, Sinotruk will increase its engine procurement from Weichai. After entering into the supporting system of Sinotruk, the market share of Weichai's heavy truck engine will further increase in the future. It is estimated that, as supported by the implementation of the national VI standards and the demand of infrastructure construction, the heavy truck sales will remain at high position in 2019. Furthermore, the Company's clear strategic framework, "Power + Hydraulic + New Energy", will help to smooth the existing business affected by the cycle fluctuations in heavy truck industry and make the business structure more balanced.

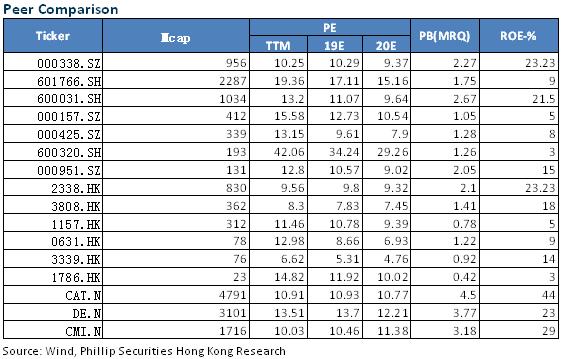

Investment Thesis

We revise the profit forecast of the company in 2019/2020 to EPS of RMB 1.18/1.28. We will also revise target price to 15.2 HKD (911.5/10.5x for 2019/2020 P/E) and buy rating. (Closing price as at 30 May 2019)

Financials

Click Here for PDF format...