|

|

NEW HIGHER EDU(2001)

Analysis:

The Group`s revenue in 2018 was RMB 561 million, a YoY increase of 35.5%, mainly due to the excellent organic growth of students in Yunnan and Guizhou, the higher average Accommodation fee per student and the consolidation of Henan and Northeastern schools. The adjusted net profit is RMB 285 million, a YoY increase of 20.3%. During the period, the organic growth for the schools was strong. The number of students in Yunnan and Guizhou schools increased by 13.7% to 44,583; the number of students in Northeast, Central China and Henan schools increased by 17.1% to 39,012. Among them, the number of students in Central China and Henan schools increased by nearly 50% and 16% respectively, but the number of students in Northeastern schools dropped slightly by 1%. It can be seen that the organic growth for those schools is strong. The number of students in Gansu and Guangxi schools is 8,218 and 9,953 respectively. In terms of tuition and accommodation fees, due to the improved dormitory environment in Yunnan and Guizhou, the average accommodation fee per student has increased by 9.9% this year. Except for Guizhou schools, the tuition fee range of each school has also increased in the 2018/19 academic year. The average tuition fee is expected to be RMB 9,947, an increase of about 5% from the previous year`s RMB 9,492. In addition, Chinese Premier Li Keqiang mentioned in the government report that in 2019, the enrollment expansion for higher vocational education will be one million. The enrollment targets of higher vocational colleges are mainly ordinary high school graduates, secondary vocational graduates, social candidates (farmers, laid-off workers, retired military personnel, new professional farmers, etc.). We believe the Group will be benefited from this enrollment expansion.

Strategy:

Buy-in Price: $2.80, Target Price: $4.00, Cut Loss Price: $2.00

ETFMG Alternative Harvest ETF (MJ)

ETFMG Alternative Harvest ETF is a passively-managed ETF with market cap of approximately USD 1.01 billion and expense ratio of 0.75%. MJ is the first US-listed ETF to offer exposure to legal cultivation, production, marketing or distribution of cannabis products for either medical or nonmedical purposes. In October of 2018, Canada legalized cannabis for adult recreational use. In addition to Canada, about 10 U.S. states have legalized cannabis for recreational use while almost half the states approved cannabis for medicinal but not recreational uses. According to the BDS Analytics, global spending on global cannabis products may surge 40% in 2019 with estimated 18.1 billion. Estimated global sales should reach $32 billion by 2022 from $12.9 billion in 2018, which is a 25.5% compound annual growth rate. Due to the loosened rules and regulations, the US will become the major driving force for the growth of legal cannabis industry, followed by Canada. Increasing adoption of legalized cannabis in various products particularly medical and recreational use would further expand the cannabis industry. Therefore, investors can access the growth opportunity through MJ ETF. Suggested to buy at $32.49, target price $38.35, cut loss if drop below $30.68.

|

|

|

Report Review of May. 2019

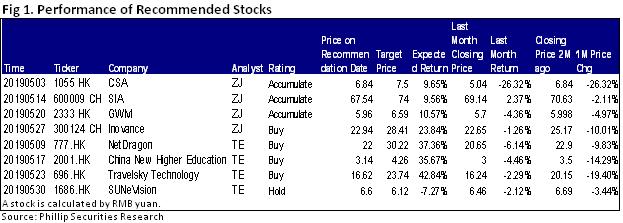

Sectors: Air, Automobiles (Zhang Jing), TMT& Education (Terry Li) Retail & Property (Tracy Ku) Automobile & Air (ZhangJing)This month I released 4 updated reports of CSA (1055.HK),SIA(600009.HK),GWM (2333.HK),and Inovance (300124.CH), which got success by their unique Competitive edge. Among them, we recommend Inovance firstRecently, Inovance announced that it planned to acquire 100% of BST by means of cash and equity, with a total transaction amount of RMB2.487 billion, corresponding to PS\PE\PB of 1.03, 10.57, 4.57 times. BST is a quality elevator parts supplier mainly serving foreign customers. BST's man-machine interface interaction system, wire and cable system, and other products are in a leading position among international brands of elevator manufacturers. It has stable cooperative relations with most of the world famous elevator manufacturers, including Otis, Kone, thyssenkrupp, Schindler and Fujitec, and has entered the global supplier system of some of them. Inovance Technology and BST are complementary to each other in terms of customers and products, with obvious synergies. By opening up the overseas market through BST, we will further expand the scale of overseas business and expand business development space. TMT& Education (Terry Li)I released four reports on NetDragon (777.HK), China New Higher Education Group (2001.HK), Travelsky Technology (696.HK) and SUNeVision (1686.HK). We highly recommend NetDragon. Since the grant of licence approval was resumed in the end of 2018, three games were granted the approvals, including “Eudemons (PC-Moblie Cross Platform Version)”, “Eudemons Legends” and “無境戰地”. Besides, there are 8 games in the pipeline which are about to be launched or under development, such as “Vow of Heroes”, “Eudemons II”, “Heroes Evolved Thrones”, “Battle of Giants” and etc. In relation to the education business, Prometheus launched a new generation of interactive whiteboard V7, and won the Red Dot Design Award. As the product's functionality becomes more mature, it helps to improve the product ASP and competitiveness. In addition, Prometheus will further enhance its monetization capabilities by providing an application platform for its own products. Edmodo will also launch more monetization plans this year. The Group expects to launch a homework helping service in the second half of 2019 and will charge monthly. In the future, the platform will also monetize by providing high-quality tutorial contents. Currently, the platform has nearly 700 million tutorial resources. Besides, 101PPT is still loss-making, the primary goal of the product is to increase the number of user and their stickiness. As of 2018, the number of 101PPT users reached 5 million, a significant increase from last year (1.2 million).

Click Here for PDF format...

|

|

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the “Group”) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products’ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

版權所有, 翻印必究。

Copyright(C) 2019 Phillip Securities (HK) Ltd. All Rights Reserved.

|